Undiscovered Gem: Sandstorm Metals & Energy

I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years.- Warren Buffett

Few investors would be willing to hold a stock for five years without the ability to sell. Why? Because few investors understand the businesses behind their stocks. And a side effect of ignorance is over-diversification, reliance on analyst commentary, and overpaying for liquidity.

Those last two are particularly important for understanding why Sandstorm Metals & Energy (STTYF.PK) has been overlooked - it has no mainstream analyst coverage and a $132M market cap. But the cash flow outlook suggests that an inflection point is at hand.

Company Overview

Sandstorm's business is straightforward. They provide capital to mining and energy exploration and production companies (E&Ps) in return for the right to purchase a set percentage of future production at a specified price. So, for example, Sandstorm may provide a junior copper miner $20M of capital to bring a mine into production a year or two from now. In return, Sandstorm receives the right to purchase up to 20% of company's copper production at $0.80/lb for the life of the mine. Sandstorm then purchases the copper at $0.80 and then immediately sells the copper at market prices, which are currently around $3.60. In mining terms, this agreement is called a "stream."

Reducing Risk

The advantage of this business model is tremendous. The company is asset-light and has the ability to produce significant revenue with relatively little overhead. This results in high free cash flow and operating leverage.

All of the risks typically associated with mining - capital overruns, production delays, regulatory compliance, shareholder dilution - are avoided or mitigated through diversification by Sandstorm. Sandstorm is not responsible for ongoing capital needs at the mines, nor can its stream be diluted by future financing.

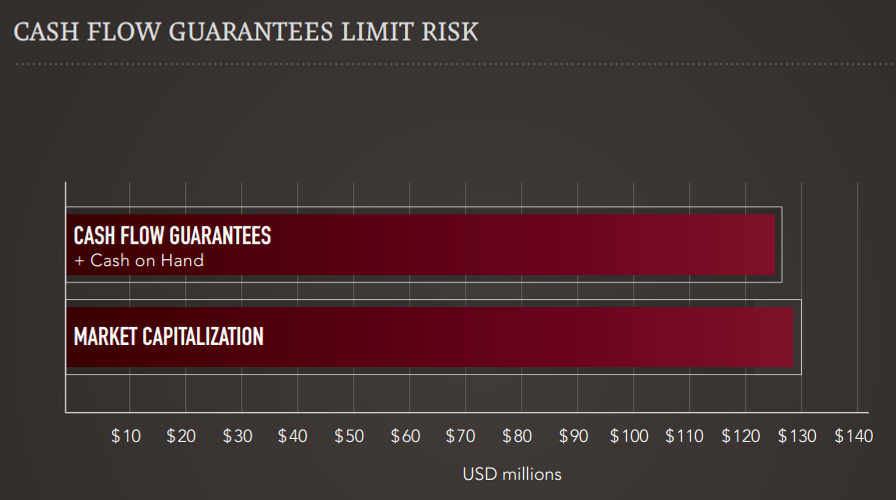

Sandstorm further reduces its risks by requiring minimum cash flow guarantees to ensure that Sandstorm earns a minimum return on its investment. To enforce its rights in the event of default, Sandstorm typically has a senior secured lien against the mine's assets.

click to enlarge

(Source: Investor Presentation)

Further, Sandstorm is able to diversify across commodities and E&Ps, reducing its exposure. As Sandstorm continues to add streaming agreements, risk will be further reduced.

Lastly, Sandstorm focuses on streams in North America, reducing the political risk associated with other locations.

Keep in mind that though Sandstorm mitigates its risk, the company benefits fully from exploration upside. If the E&P continues to develop the resource and finds that the mine has much larger production potential that originally anticipated, Sandstorm still holds the right to purchase a fixed percentage of production. The higher the production, the greater Sandstorm's return on investment.

Current Streams

The vision for Sandstorm Metals & Energy was to create the world's first base metal, bulk commodity and energy streaming company. We launched the company in December 2010 with a $100 million financing and two coal streaming deals and have since added an oil and gas deal.* We have a strong cash position and an aggressive growth plan and we are actively pursuing base metal opportunities in copper, lead, zinc, nickel etc. as well as more energy deals.* Since the interview, the company also acquired a copper stream

Sandstorm is a relatively young company, but has already executed streaming agreements for copper, thermal and met coal, natural gas, and oil. The company seeks to do deals in the energy and base metals space. The sister company, Sandstorm Gold (SNDXF.PK), focuses exclusively on gold streams.

On the most recent conference call, management said that the company is seeking to acquire another stream this year using cash on hand of roughly $40M. Note that the company currently has 30% of its market cap in cash. Sandstorm is likely to go after a base metal such as nickel or zinc. Also, management has noted that they are not interested in acquiring "rare earth" or precious metal streams.

I will leave a detailed analysis of the streams until later (also see the links below), but the key point to note now is management's focus on exploration upside. In most cases, management only acquires a stream when there is a compelling geological case for greatly expanding production in the future.

Perhaps it is apparent by now that management is focused on risk-adjusted returns for shareholders. They mitigate downside risk and chose opportunities with compelling upside.

Management

The CEO of Sandstorm Metals & Energy also serves as the CEO of Sandstorm Gold. He thinks like Warren Buffett, flies coach to save money for shareholders, has a heart for humanitarian work, and was theyoungest CFO ever at a NYSE-listed company at the age of 26. Watson took his experience as CFO at silver streaming company Silver Wheaton (SLW) and applied the same business model to the gold and metals/energy spaces.

Watson heads up a team that is skilled at financial and geological analysis. Their ability to ferret out the best opportunities and negotiate deals is key to the success of Sandstorm.

Competitive Environment

One of the most interesting elements to the story is the lack of competition from streaming companies in the base metals and energy space.

And the current environemt is favorable for executing streaming agreements. Market conditions make it very difficult for junior E&Ps (small caps) to raise capital. Banks are hesitant to work with juniors because juniors lack cash flow to service loans. That is why most juniors finance capital costs through issuing equity. And there's the rub.

Because investors have generally avoided high-risk junior E&Ps during the uncertain economic environment of the past few years, junior E&P share prices have been depressed. Existing investors are diluted when additional shares are issued to raise money. And the level of dilution increases with lower share prices because more shares must be issued to raise an equal amount of capital.

Sandstorm offers an attractive alternative. A streaming agreement with Sandstorm is more flexible than a bank and less dilutive than issuing equity.

It is easy to see the size of the opportunity for Sandstorm - management is able cherry pick the best deals from juniors hungry for capital.

Valuation

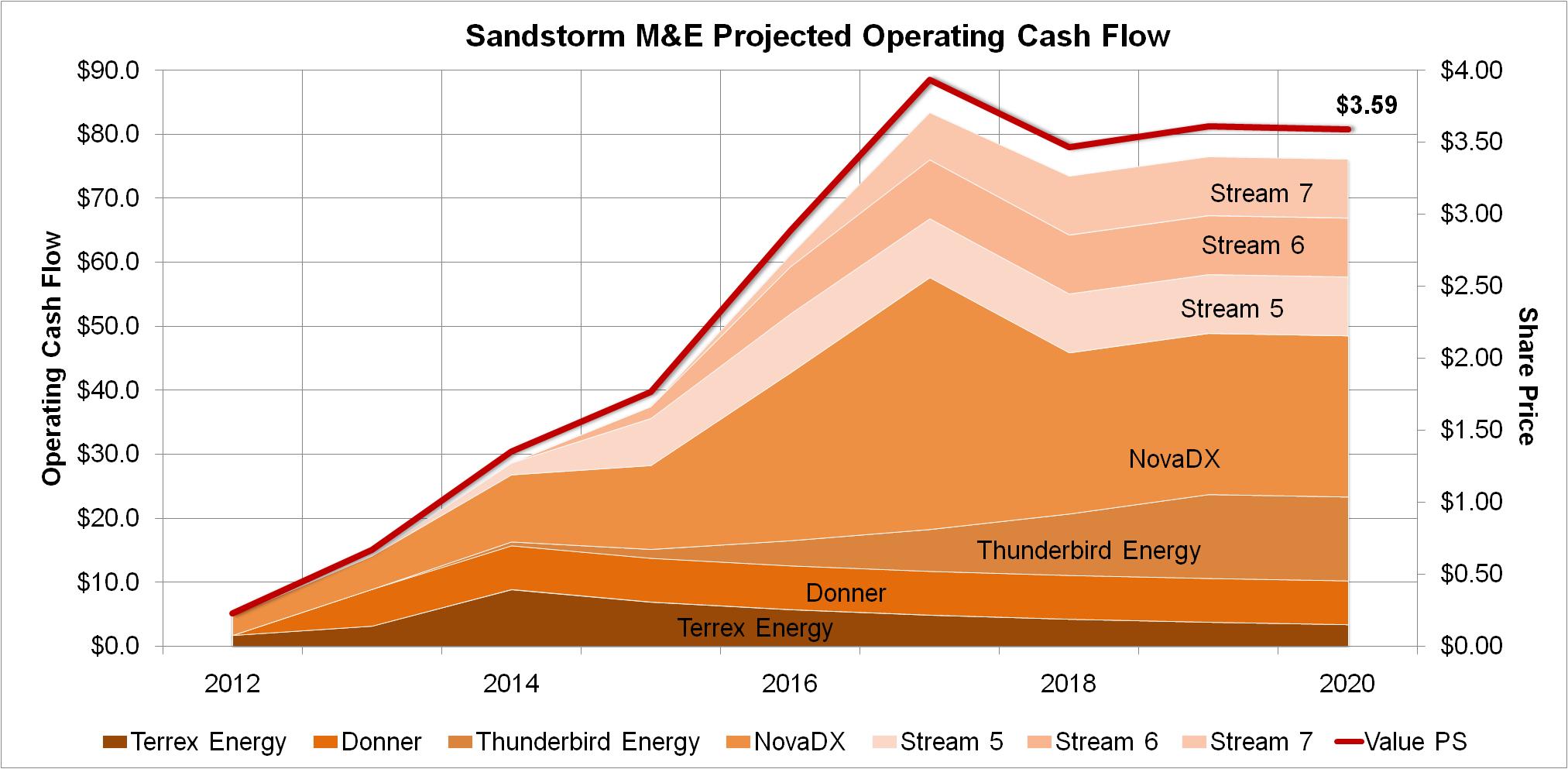

Sandstorm should be cash flow positive at least by early 2013. It is important to note that unlike a biotech or other speculative, cashless companies, Sandstorm has an incredibly high likelihood of producing significant cash in the near term. The agreements are already in place. It simply takes time to build a mine and ramp up production.

The graph below is my estimate of cash flow based on current streaming agreements. The graph also shows the potential future cash flow if Sandstorm executes an additional streaming agreement this year (as management guided) and another in 2013 and 2014. While the actual size and timing of cash flows from new streams is speculation, it serve to illustrate the snowball effect in play as Sandstorm invests the $40M on its balance sheet, reinvests cash produced, and eventually taps the credit markets as Sandstorm Gold did recently.

My estimates also assume Donner Metals (DONFF.PK) exercises its right to repurchase 50% of the copper stream (reducing Sandstorm's stream from 17.5% to 8.75%).

The value per share estimate uses a multiple of 15x current year operating cash flow. The closest public comparables, Sandstorm Gold, Royal Gold (RGLD), and Franco Nevada (FNV) - typically trade north of 14x-16x. See the investor presentation for more details. A premium valuation is reasonable for a company that has high free cash flow and many opportunities to reinvest the cash at a 25%+ IRR.

I estimate that over the next 4 years, the company will earn cumulative operating cash flow in excess of its current market cap. This makes Sandstorm Metals & Energy an extremely attractive investment.

Sandstorm Gold is in the process of uplisting from the OTCB to the American Stock Exchange (in addition to its current listing on the TSX Venture Exchange in Canada). I expect Sandstorm Metals & Energy to follow suit once cash flow ramps. Due to the production timing of its streaming agreements, Sandstorm Gold is a couple of years ahead of its sister company and is now a $600M company. Sandstorm Gold serves as a model of what management will seek to do with Sandstorm Metals & Energy over the next few years.

Conclusion

The market has a tendency to misprice securities that are at inflection points, especially when significant free cash flow and reinvestment opportunities exist.

Sandstorm is on the cusp of rapid growth in cash flow yet is almost completely ignored by the market due to its small size and illiquidity. Illiquidity does not make for a poor investment so long as the investor is compensated with a higher return (a "liquidity premium"). Such a liquidity premium is no doubt discounted into the stock.

The upside potential is clear. Investors willing to research the streaming agreements and understand the production timelines and risk will no doubt have an edge.

Links

Great work done by another investor (with other lists of links):

No comments:

Post a Comment