April 16, 2012 | about: REGN, includes: AMGN, DNDN, FBT, GSK, HGSI, JNJ, MDVN, MRK, NVS, PFE, SNY, VRTX

Biotechnology is a sector that offers much in the way of both risk and reward. And for investors willing to research the sector, large profits are possible. We believe that Regeneron Pharmaceuticals (REGN) has the potential to offer investors profits, even after its outsized gains so far this year.

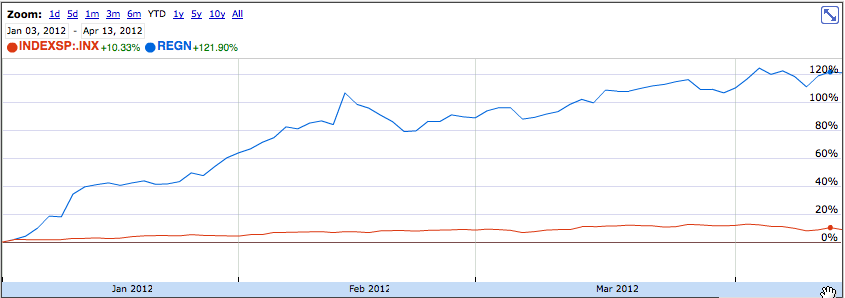

Regeneron has 2 drugs on the market, Eylea and Arcalyst, which treat age-related macular degeneration and cryopyrin-associated periodic syndromes, respectively. The company has a deep partnership in place with Sanofi (SNY), which we will discuss in detail below. Year-to-date, the stock has more than doubled, advancing over 121% as optimism grows over future sales and its pipeline. Of further interest is the fact that unlike many other biotechnology companies, such as Human Genome Sciences (HGSI) and Vertex Pharmaceuticals (VRTX), Regeneron has not succumbed to post-launch selling pressure.

As a matter of disclosure, we are long Regenron via the First Trust NYSE Arca Biotechnology Index Fund (FBT) and a mutual fund that gives Regeneron a weighting of 2.11%. We have no direct position in the stock.

(Click charts to enlarge)

The question now is can Regeneron continue to climb? After all, investments in stocks are investments in the future, not the past. Before we delve into Regeneron's drugs, we will first provide a brief financial overview of the company.

Regeneron Financial Overview

| 2009A | 2010A | 2011A | 2012E | 2013E | |

| Sanofi Collaborative Revenue | $314.357 Million | $311.332 Million | $326.609 Million | N/A | N/A |

| Net Product Revenue | $18.364 Million | $25.254 Million | $44.686 Million | N/A | N/A |

| Total Revenue | $379.268 Million | $459.704 Million | $445.824 Million | $800 Million | $1.1 Billion |

| R&D Expense | $398.762 Million | $489.252 Million | $529.506 Million | N/A | N/A |

| Total Operating Expenses | $453.371 Million | $556.546 Million | $650.983 Million | N/A | N/A |

| GAAP EPS | -$0.85 | -$1.26 | -$2.45 | -$0.30 | $1.30 |

| Net Cash | $390.010 Million | $626.939 Million | $535.531 Million | N/A | N/A |

| Average Shares Outstanding, Year-End | 79.782 Million | 82.926 Million | 90.61 Million | N/A | N/A |

Regeneron is set to reach profitability in 2013, on the back of continued growth in Eyelea and Arcalyst sales, as well as its pipeline. However, some analysts believe profitability could be reached in 2012 on the back of stronger-than-expected sales. We believe that further upside in Regenron is possible, and we now delve into Regeneron's approved products to see what is currently driving the company.

Eylea and Arcalyst: Catalysts Ahead

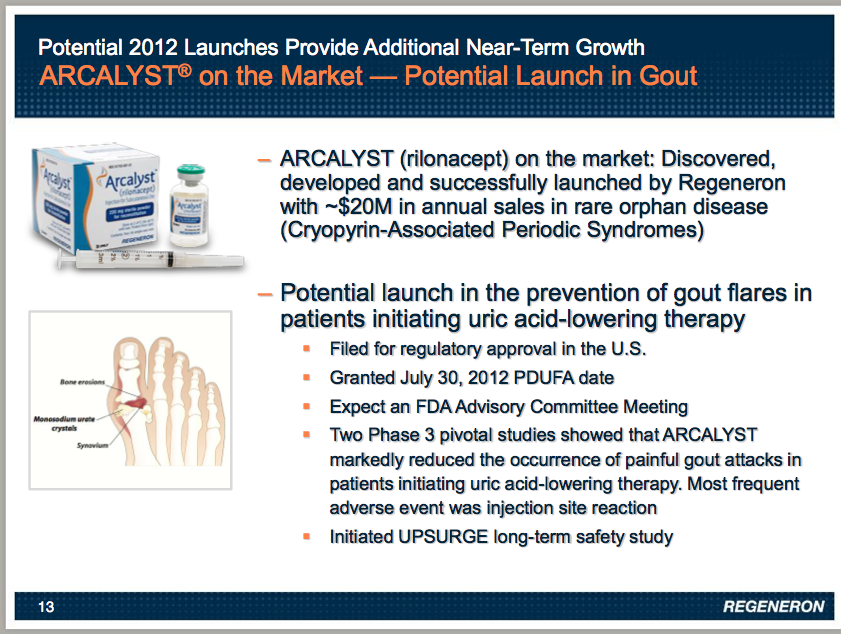

Arcalyst was approved in 2008 for the treatment of cryopyrin-associated periodic syndromes, but has made little contribution to Regeneron in terms of profitability. Annual sales are currently at around $20 million, for Arcalyst targets a rare disease. Yet, there is further potential in this compound, as the drug is currently under FDA review for the treatment of gout. A PDUFA date of July 30, 2012 has been set.

Regeneron will own 100% of worldwide profits from the sale of Arcalyst. However, Arcalyst has not, nor will it be Regeneron's focus for the foreseeable future. That role happens to go to Eyelea.

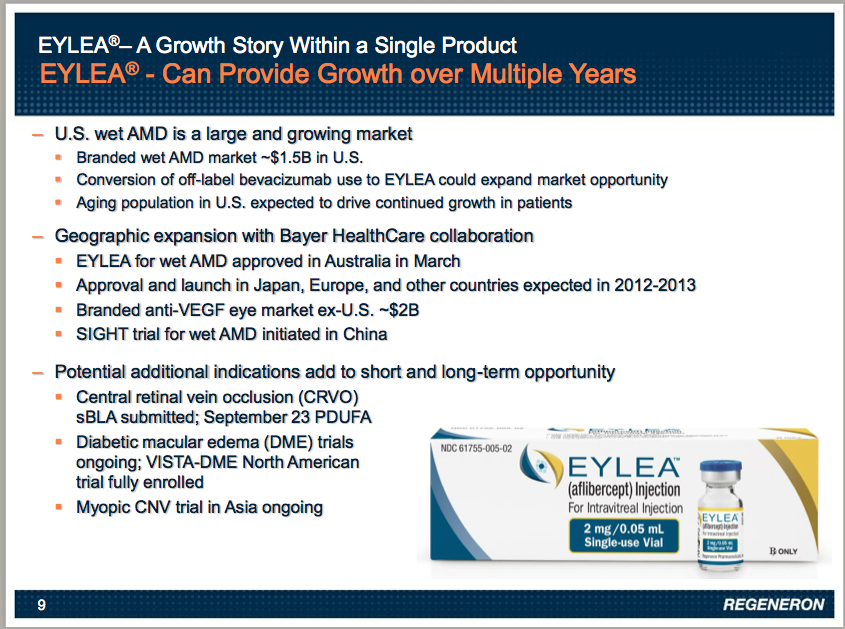

On November 18, 2011, Regeneron annoucned that the FDA approved Eylea for the treatment of age-related macular degeneration (AMD) in the United States (Regeneron and its partners are in the process of launching Eylea in several other countries). Eylea will be competing against several existing treatments for AMD, most notably Roche's Lucentis. Eylea is expected to reach blockbuster status in 2012, and a variety of factors back up this claim. In assigning a $142 price target and outperform rating to Regeneron, BMO noted that Lucentis is already losing market share, citing statistics from Roche's 1st- quarter earnings conference call. Roche executives reported that Lucentis' market share has declined to 36%. This data shows that patients are switching to Eyelea, presenting a significant opportunity for Regeneron in the months and years to come.

The branded AMD market is believed to be currently worth around $1.5 billion in the United States alone, and Eylea should be able to capture a significant portion of that market. Goldman Sachs, in assigning a $144 price target to Regeneron, notes that peak sales should reach around $2.3 billion in the United States and $4 billion worldwide, driven by continued aging of populations in the United States and across the world.

Eylea does face several challenges. Permanent J-codes for reimbursement will not be granted until January 2013, although physicians and payers have not indicated any meaningful reimbursement issues. Another issue facing Eylea is cost. While Eylea, at $1,850 per injection is cheaper than Lucentis, its main competitor (which costs $1,950), off-label use of Avastin (from Genentech, a Roche unit) for the treatment of AMD is common, and in such scenarios it costs just $50 per dose. Avastin currently accounts for over half of the AMD market, and Regeneron will have to convince physicians and patients that the efficacy profile of Eylea, as well as its less frequent dosing is worth the increase in cost. So far, Regeneron's efforts appear to be successful. According to the company, the Eylea launch is tracking above expectations, and the company is now forecasting 2012 sales of between $250 and $300 million, up from previous estimates of $160 million. Sales were $24.8 million in the fourth quarter of 2011 (from approval through December 31). Readers should be made aware that Regeneron and Bayer lost a patent case relating to Eylea in Britain, where a judge ruled that the drug infringes on a patent held by Genentech. However, the ruling has no impact on sales in the United States, and the patent in question expiresin October,

Like many biotechnology companies, Regeneron is focused on not only launching drugs, but expanding their usage. And that is exactly what Regeneron is doing with Eylea. The FDA is currently reviewing Eylea for the treatment of central retinal vein occlusion, and a PDUFA date of September 23, 2012 has been set. Eylea is currently in Phase III trials for diabetic macular edema, and the drug is also in Phase III trials for choroidal neovascularisation in Asia. We now turn to Regeneron's pipeline.

The Pipeline: A Myriad of Opportunities

Unlike other "non-Big 4" biotechnology companies we have covered, such as Human Genome Sciences and Vertex Pharmaceuticals, who have just a few drugs in development, Regeneron has 12 compounds in various stages of development, including new indications for Arcalyst and Eylea, which we discussed above. Therefore, we will focus on the 3 other compounds that are the furthest in the development and approval process. Much like Human Genome Sciences is intertwined with GlaxoSmithKline (GSK), Regenron has a deep partnership with Sanofi, which is providing Regeneron with $160 million in research funding through 2017. Regeneron has partnered with Bayer for the global commercialization of Eylea, and the two companies split profits and costs equally.

The first drug we will discuss is Zaltrap, developed with Sanofi for the treatment of metastatic colorectal cancer and prostate cancer. Based on Phase III data from the companies' VELOUR study, Sanofi and Regeneron filed for approval in both Europe and the United States.

On April 5, Sanofi and Regeneron provided an update on Zaltrap. They announced that the FDA has granted priority review status for Zaltrap, citing the unmet medical need for the drug. A decision date of August 5, 2012 has been set. In addition, the companies announced Phase III data from the VENICE trial of Zaltrap. While the results showed a consistent safety profile with previous studies, the study failed to meet its goals in terms of extended survival benefits. While the companies have not yet abandoned the development of Zaltrap for prostate cancer, at this time we do not believe that other companies with prostate cancer treatments on the market, such as Dendreon (DNDN), Medivation (MDVN), and Johnson & Johnson (JNJ) need to worry about Zaltrap. Assuming that Zaltrap is approved as a second-line treatment for colorectal cancer, itcould see peak sales of up to $250 million, but that number could rise sharply if it is approved as a first-line treatment.

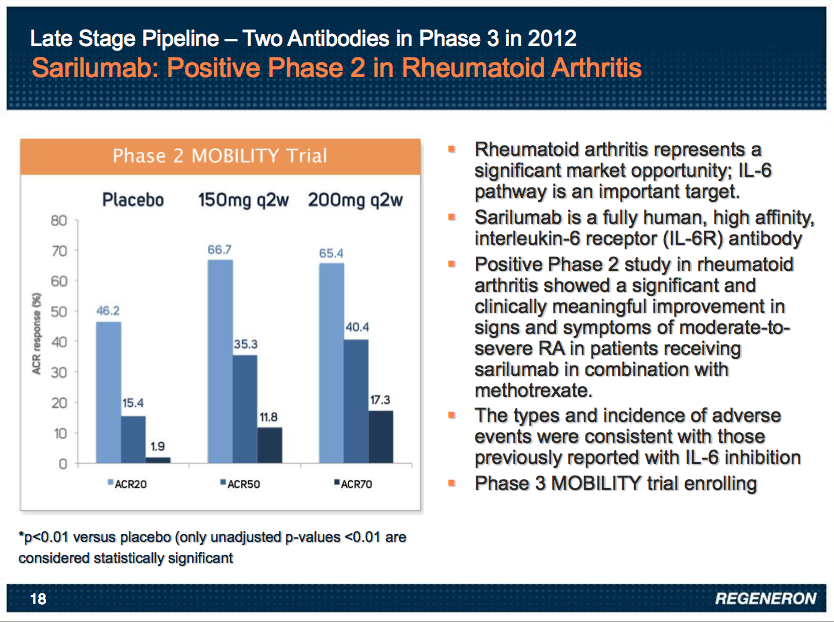

The second compound we would like to cover is Sarilumab, which is currently in Phase III trials for the treatment of rheumatoid arthritis. This antibody was developed in collaboration with Sanofi as well, further highlighting the deep ties the two companies have. Phase II data for Sarilumab was positive, and further data is expected in either the second half of 2012 or 2013.

Sarilumab, however is not an ideal drug. It disappointed in its Phase IIb ALIGN trial, which looked at the compound's efficacy in treating ankylosing spondylitis. Furthermore, should Sarilumab be approved, it will join a crowded rheumatoid arthritis market. Amgen (AMGN), Pfizer (PFE), Merck (MRK), and Johnson & Johnson all have drugs on the market that target this disease.

The third and final compound we would like to address is REGN-727, and it is perhaps the one with the most potential for Regeneron. REGN-727 is a anti-PCSK9 antibody currently transitioning into Phase III trials, which are set to start in the second quarter of 2012. It is designed to lower bad cholesterol. The gene that expresses this protein was discovered in 2003, and further research done in 2006 at the University of Texas Southwestern medical Center further demonstrated the potential of this class of drugs.

A Phase I study of REGN-727 showed that patients who took the drug lowered their LDL cholesterol by as much as 72% on top of Lipitor (Pfizer).

The safety profile of this drug is encouraging. In Phase II trials, the most common side effects were reactions at the injection site, such as rashes. Of the 183 patients in the Phase II trial, six stopped treatment due to unspecified adverse effects.

Regeneron is not the only company to have an anti-PCSK9 compound in development. Amgen and Merck are both developing their own treatments. AMG-145 is in Phase II trials. Earlier studies of AMG-145 showed that patients lowered their cholesterol levels by as much as 81% on top of Lipitor, and six Phase II trials with 1,900 patients will have results by the end of 2012. Merck, Pfizer, and Novartis (NVS) all have anti-PCSK9 drugs in various stages of development. AMG-145 presents the greatest threat to Regeneron. Though it may be about a year behind REGN-727, its efficacy profile is superior. In its Phase I results, AMG-145showed minimal declines in efficacy in the eighth week of trials (two doses were given four weeks apart). REGN-727, on the other hand, showed notable declines in efficacy in 4-week intervals. However, REGN-727, when given at 2-week intervals instead, showed "remarkable efficacy," according to Richard McKenney, CEO of National Clinical Research. REGN-727 will likely be built around 2-week dosing. REGN-727 is about a year ahead of AMG-145 in the clinical process, and as many drug companies will tell you, it is sometimes more important to be first to market, not best to market. This class of drugs is so new that no one knows the exact sales potential. Estimates range from $8 to $25 billion in annual anti-PCSK9 sales, and Regeneron should take in billions even if it does not capture a majority of the global market, should REGN-727 be approved. Merrill Lynch, in raising its price target for Regeneron from $130 to $135, cited REGN-727 as a leading factor in its decision to raise the target, and noted that the company's antibody platform provides a clear roadmap for long-term growth.

Regeneron has multiple other antibodies in various stages of development, and most of them are developed in collaboration with Sanofi. It is early to speculate on the future of the rest of Regeneron's pipeline at this time. And it should be noted that Phase II trials of REGN-475, the company's osteoarthritis of the knee and pain treatment, are on hold. This is due to an FDA directive ordering all American companies to halt all trials of anti-nerve growth factor drugs, such as REGN-475, due to reports of bone death. It is yet to be determined whether or not bone death was caused by these drugs, or due to the natural progression of the disease.

Regeneron has a strong pipeline, and Sanofi has committed itself to the company for the next several years. Therefore, it is only natural that we must address takeover speculation.

Sanofi and the Shareholder Base

With all the catalysts that Regeneron has, it may be surprising to learn that there has been little takeover chatter surrounding the company, even rumors involving Sanofi. We believe that part of this may be due to Regeneron's market capitalization, which currently stands at over $11.5 billion. When factoring in the premium needed to buy out the company, the price tag becomes prohibitive for all but the largest pharmaceutical companies, and such mega-deals do not occur frequently. If a deal for Regeneron were to occur, it would take a great deal of time to orchestrate, and at this time, we have not heard rumors that would suggest any pharmaceutical company is eying Regeneron.

Regeneron has the backing of several leading institutional shareholders, implying confidence in its long-term plans. Capital World Investors is the largest shareholder, holding 11.69% of the company. Fidelity and T-Rowe Price are not far behind, with stakes of 11.3% and 8.69% respectively.

Conclusions

We believe that even with the run that Regeneron has had, the stock can still rise from here. We agree with Jefferies that Regeneron is not being given enough credit for its pipeline, and think that 2012 and 2013 will be great years for the company as it expands its product portfolio, captures market share, advances compounds through the pipeline, and reaches profitability. Investors who wish to hedge their investments may buy put options on Regeneron if they desire to lower their risk. Regeneron is executing on all fronts, and in our opinion, the rally the stock has seen is not yet over.

By Helix Investment Management

Additional disclosure: We are long shares of REGN via the First Trust NYSE Arca Biotechnology Index Fund and a mutual fund that gives it a weighting of 2.11%. We are long shares of MRK and PFE via the SPDR Dow Jones Industrial Average ETF.

No comments:

Post a Comment