About: SPDR S&P 500 Trust ETF (SPY), QQQ, DIA, SH, IWM, TZA, SSO, TNA, V

Summary

Economic news was solid and the market responded.

Few fireworks from Chair Yellen and no major conflict with Pres. Trump.

Rising inflation raises the question of more aggressive Fed policy.

Confidence is higher, but the jury is still out on specific Trump policies.

Analyzing the Trump effect on stocks is much more difficult than most realize.

We have another holiday-shortened week with little fresh data. While there are some Fed speakers on tap, it is not enough to feed the avaricious punditry. There are two competing themes: the spike in inflation and the continuing assessment of Trump Administration policies. Once again, I expect the two to be joined in most commentaries. Pundits will be asking:

Will Trump policies extend the business cycle?

Last Week

Last week the economic news was mostly positive, and stocks responded.

Theme Recap

In my last WTWA I predicted a conjunction of two themes as Fed Chair Yellen testified to Congress and President Trump considered candidates for several Fed vacancies. I was only half right. Yellen got plenty of attention from Congressional questioners and revealed that she plans to finish her term as Chair. She also gave some non-specific agreement with some of Trump's principles about regulation. GOP questioners wanted to talk about the Fed balance sheet. President Trump did not comment about this. This topic will have continuing interest. Presidents are rarely fans of rising interest rates.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes the record high and the overall gain of 1.51% for the week.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective.

The News

Each week I break down events into good and bad. Often there is an "ugly" and on rare occasion something very positive. My working definition of "good" has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news - and you should, too!

This week's news was mostly positive.

The Good

- LA Port traffic surges. Calculated Risk analyzes the factors, concluding that imports and exports both helped, and explaining the dip in 2015.

- Rail traffic improves, but mostly due to coal and grain Steven Hansen (GEI) reports.

- Building permits rose 4.6%. This is one of my favorite leading indicators, since permits cost money and represent a serious commitment. Bob Dieli has a nice chart in his regular data review (subscribers only).

- Retail sales increased 0.4% beating expectations of a flat report. December's data was revised to a 1% gain from the prior 0.6%.

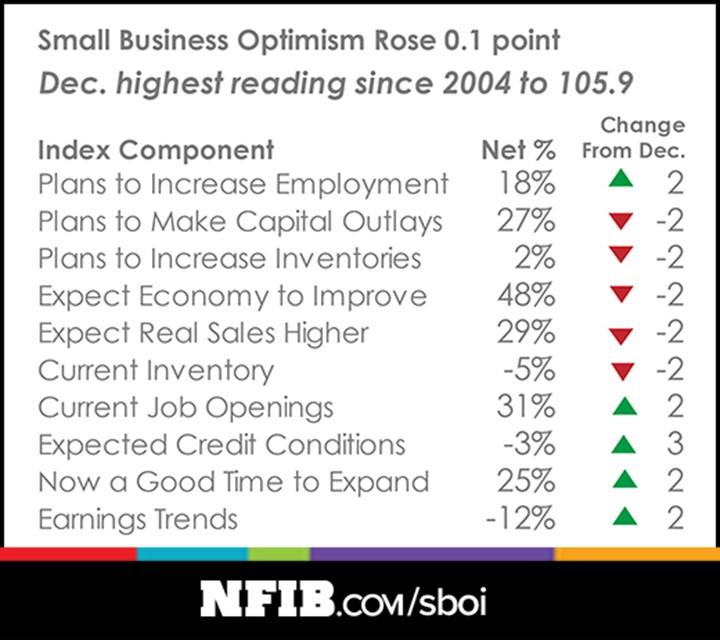

- NFIB small business optimism shows that "economic growth is coming." Dr. Ed opines that this must be a Trump effect.

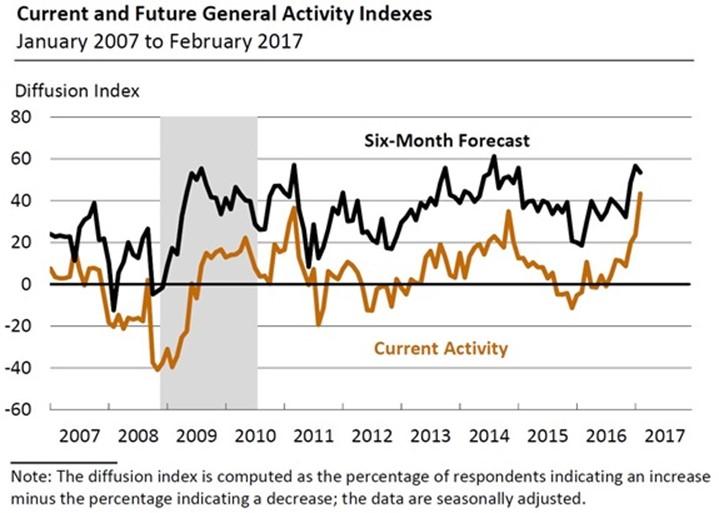

- Philly Fed survey rose 43.3, crushing expectations of 17.5 and the prior month's 23.6. The six-month outlook also remains very strong. From the report:

- Leading indicators remained strong increasing 0.6% and slightly beating expectations.

The Bad

- Industrial production dropped 0.3%, missing expectations for a flat report.

- Fewer developed market stocks are outperforming - 44% versus the 57% average. Eric Bush of GaveKal explains that this has a negative correlation with the overall market.

- Kim Jong-un took two provocative actions, two days apart. Jonathan D. Pollack at Brookings wrote "…North Korea's impetuous young leader, yet again reminded the outside world of his determination to defy international norms by all available means". The ballistic missile test was a flagrant violation of agreements, and the assassination of his half-brother continues a policy of killing potential rivals. So far, the market has taken little notice of such events or other possible challenges to the new president.

- Inflation data showed price increases greater than expected (Briefing.com consensus in parentheses). PPI was up 0.6% (0.3%). CPI up 0.6% (0.3%). Core CPI up 0.3% (0.2%).

- Housing starts declined in January, so I am scoring this as a negative. The prior months were revised higher, and the result was a slight beat of expectations. Calculated Risk, one of the top sources on housing matters, ascribes the shifts to the volatile, multi-family sector. Bill expects starts to increase 3% - 7% in 2017. The range may seem wide, but he is careful to explain the expected error around his forecasts, which have been quite good. See the full post for charts splitting out multi- and single-family.

The Ugly

Malware is winning the race against antivirus software. Users are not taking the most important precautions. Hint: Strong passwords and a password manager. (Slate).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. This week's award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, the types of debt, and the threats to the system are easily made. It takes only a chart, and most readers are pre-convinced.

Explaining the data requires a deeper, second-order analysis. In his well-sourced article, Josh takes a comprehensive look at employment and lending. You need to read the entire post (twice) but the no-nonsense conclusion captures the key point for investors:

When bankers complain, the rhetoric is almost always a caricature of the reality. Today is no different. There's probably room to streamline or clean up the crisis era regs, but to make the claim that "the banks can't lend" flies in the face of the actual facts.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a very light week for economic data, with all reports in a three-day period.

The "A" List

- New home sales (F). Gains expected in this important sector.

- Michigan sentiment. Important indicator for employment and spending.

- Initial jobless claims (Th). How long can the amazing strength continue?

The "B" List

- Existing home sales (W). Not as important as new sales, but is a read on the overall strength of the housing market.

- FOMC minutes. No surprises expected.

- Crude inventories (Th). Recently showing even more impact on oil prices. Rightly or wrongly, that spills over to stocks.

Fed Presidents will be on the speaking trail. Earnings reports continue. Early actions from the Trump Administration have captured the spotlight and will continue to do so.

Next Week's Theme

If the market did not have the extreme Trump focus, the question would be whether incipient inflation suggests the need for more aggressive Fed policy and the probably end of the growth portion of the business cycle.

With the daily parsing of tweets, executive orders, and (somewhat conflicting) policy statements, analysts are scrambling to define and re-define the "Trump Effect."

In a holiday-shortened, light week for data, I expect a combination of these two themes:

Will Trump Policies Extend the Business Cycle?

Discussion of this topic includes both the policies and the business cycle. Most are not rigorous in separating them.

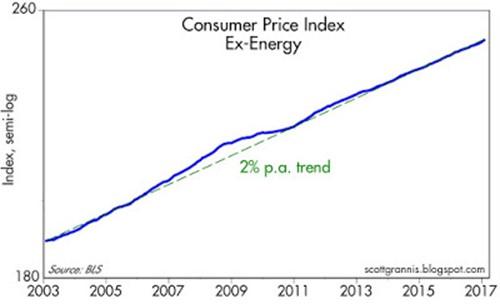

Scott Grannis does a good job by focusing on the inflation effect and the business cycle. He notes that core CPI inflation has been rather stable, and that it is "a stake through the heart of the deflation demon".

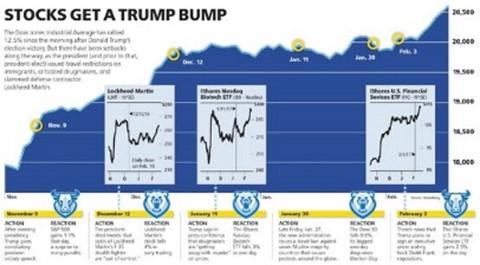

By contrast, Barron's focuses on the stock and market effects. In their cover story, they review each Administration move:

Will the week ahead provide any more clarity and focus? Maybe not, but investors should look for the following key points:

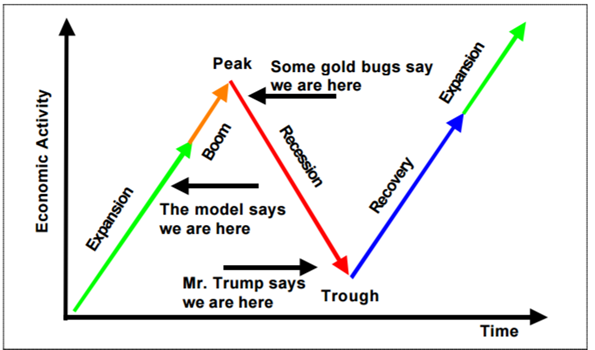

- Is there evidence of a business cycle peak? Here is Bob Dieli's take, vividly comparing the disparate opinions:

- Will Trump policies extend the cycle? Some are citing confidence from both businesses and consumers as evidence of a return of "animal spirits." The Trump administration is forecasting much stronger growth than does the CBO. (MarketWatch).

- Many Trump moves are generating opposition, sometimes with the Republican party.

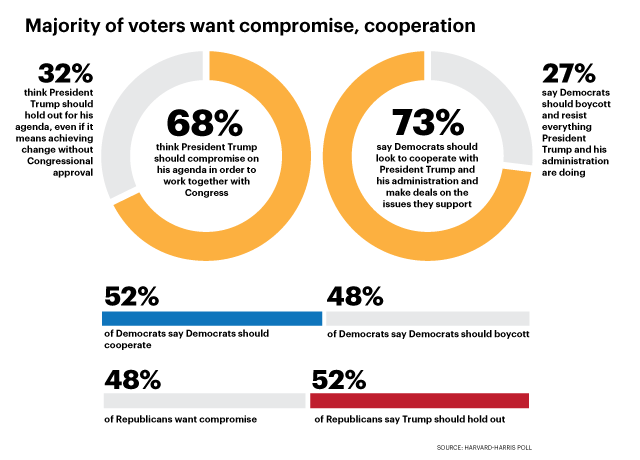

- Most voters are looking for compromises. This is true of both parties. "The Hill."

What does this mean for investors? As usual, I'll have a few ideas of my own in today's "Final Thought".

Quant Corner

We follow some regular great sources and the best insights from each week.

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.