Summary

WESCO is cheap, both objectively and compared to its long-term valuation history.

WESCO is safe - it has a valid business model, a diverse customer base, and it is diversified geographically.

Uncertainty regarding short-term headwinds scares away short-term oriented growth investors, and creates an opportunity for long-term oriented value ones.

What happens when growth investors' darling stock takes a recess from growing, and fails to notify investors the exact time for it to resume its growth?

You've probably guessed correctly, the stock declines in price.

What happens when the underlying company is exposed to Gas and Oil as well as the Canadian dollar?

Well, I'll tell you what happens. Growth investors run for the hills, not looking left or right. The stock price cuts in half. Price decouples from fundamentals. From a darling growth play, it becomes a hated stock, one that institutional investors wouldn't want their clients to see in their portfolios. One that individual investors wouldn't tell their friends about.

But, where others see junk, value investors see opportunity. The company I am about to portray is first and foremost cheap, secondly safe, and thirdly has a fair chance of returning to growth sooner or later. Should an investor adopt a longer term time horizon and a stomach for volatility, I believe it is more likely than not that a small investment in this name, as part of a well diversified portfolio, should turn out well.

The Business

WESCO International (NYSE:WCC) is a distributor of industrial, electrical and communication supplies such as fuses, connectors, wires, light bulbs, tools and testers, safety products, consumables, janitorial products, and almost anything you can imagine - 215,000 product SKUs in total.

The business model is rather simple. This $2 billion market cap company utilizes economies of scale to buy products from manufacturers in wholesale prices, and sell them to businesses and organizations at market prices.WESCO simplifies procurement for industrial, commercial and government organizations by alleviating the need to manage procurement from tens or hundreds of suppliers, as well as providing a level of service which include next day deliveries and technical support. WESCO also provides value added services such as staffing for procurement and inventory management; manufacturing process improvements; consulting; training and participating in cost savings teams. There are quite a few similarities between the business model of WESCO and another holding of mine, Houston Wire and Cable Company (NASDAQ:HWCC), which I have profiled in my personal blog.

According to management estimates, electrical distribution industry sales have grown at an approximately 4% compound annual rate over the past 20 years.WESCO's revenue distribution from the various customer segments have stayed rather stable during the last few years, as can be seen from the following table:

(click to enlarge)

(source: 2014 10-K)

WESCO aims to grow both organically and through acquisitions. Making small acquisitions of distributors within this fragmented industry is the norm forWESCO. In this business, economies of scale play a crucial role due to its commoditized nature. WESCO is one of the largest players in this space, having 485 full service branches and nine distribution centers across all north America. It serves 75K active customers and employs approximately 9,400 employees worldwide. It swallows up much smaller local or regional electrical and industrial distributors and creates value as it integrates them into its larger and thus more efficient infrastructure. The supplies distribution industry is so fragmented that, according to this analyst, the four largest players (WESCO, Sonepar, Graybar and Rexel) account for only 25% of the market. Such a fragmented industry structure provides ample opportunities for WESCO to create a pipeline of small acquisitions and add value by expanding its economies of scale and its market position.

Side Note: I have found the analysis linked above using the customized value investing search engine that I developed, and can be accessed here.

In 2014 alone, WESCO made three acquisitions, LaPrairie, Inc. ("LaPrairie"), Hazmasters, Inc. ("Hazmasters"), and Hi-Line Utility Supply ("Hi-Line"). Despite the fact that WESCO does not disclose the price it paid for each acquisition, management did disclose annual sales figures. In total, the three companies generated approximately $140M in annual sales at the year of acquisition. According to WESCO's cash flow statement, cash paid for acquisitions in 2014 totaled $138M. With the industry median P/Sales being 0.62x, WESCO might have been too generous, yet one should bear in mind the value creating opportunities and synergies described briefly above.

2015's acquisition of Hill Country Electric Supply seems to have come at a much cheaper price, costing WESCO only $68M for approximately $140M in annual sales.

The largest acquisition to date was that of EECOL in 2012, a full-line distributor of electrical equipment, products and services with 57 locations across Canada and 20 in South America. WESCO paid $1.1 billion for that acquisition, having to raise debt through a term loan in order to fund it. During 2012, EECOL had revenues of about $900M and net income of $62M. As it turns out, the timing of the acquisition, which occurred at the peak of the gas and oil cycle, was not perfect. Revenue stagnated during 2013 and started declining in 2014 to date, mostly due to softness in the Gas and Oil and mining sectors, as well as currency headwinds. It shows that even industry pundits cannot predict macro cycles.

Nevertheless, WESCO did a nice job of reducing its leverage since the EECOL acquisition to below 3x, its stated target in recent conference calls, but the leverage has picked up again during the last three quarters. The recent hike results from the disappointing operating results in the last three quarters. Longer term, I believe that management will be able to return to a reasonable 3x EBITDA/debt levels. The following figure, taken from Q3 '15 earnings presentation shows how debt has nicely declined since EECOL's acquisition in Q4 '12, but picked up again during the last three quarters.

Usually I shy away from companies with excessive debt load. While WESCO's debt, totaling 85% of equity, is not insignificant, it is not excessive nonetheless. In such a business, having thin profit margins and a relatively stable revenue base, funding operations with cheap debt is, in my mind, very acceptable. Moreover, with the recent successful refinancing of a $440M revolving credit facility due in 2016, WESCO does not have any significant maturities through 2019. I shall continue monitoring debt levels, yet I'm not overly concerned, for now.

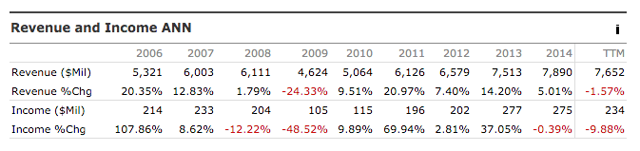

Let's examine next the history of revenue and profitability. The consistent growth trend in revenues and net income, which had prevailed over at least ten years (except an obvious decline during the crisis years 2009-2010), came to an abrupt stop in 2014. Those investors who were accustomed to high single-digit or even double-digit annual growth rate are waking up to find that their darling going nowhere but sideways for almost two years now, while some of them may have expected the growth trend to prolong well into the future, maybe to infinity. The table below tells this story.

(click to enlarge)

Who's to blame for the cessation of growth?

Well, who's not to blame?

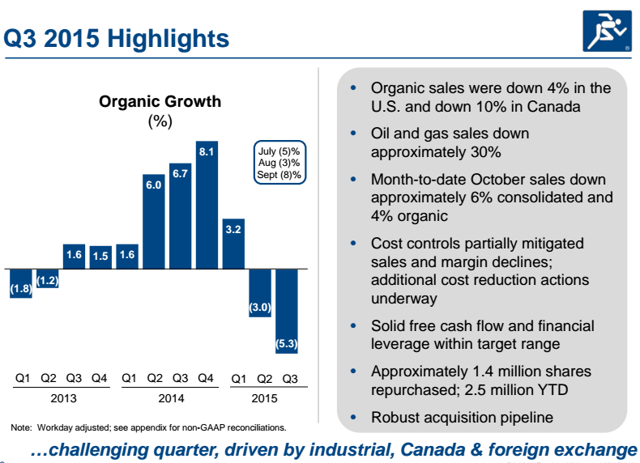

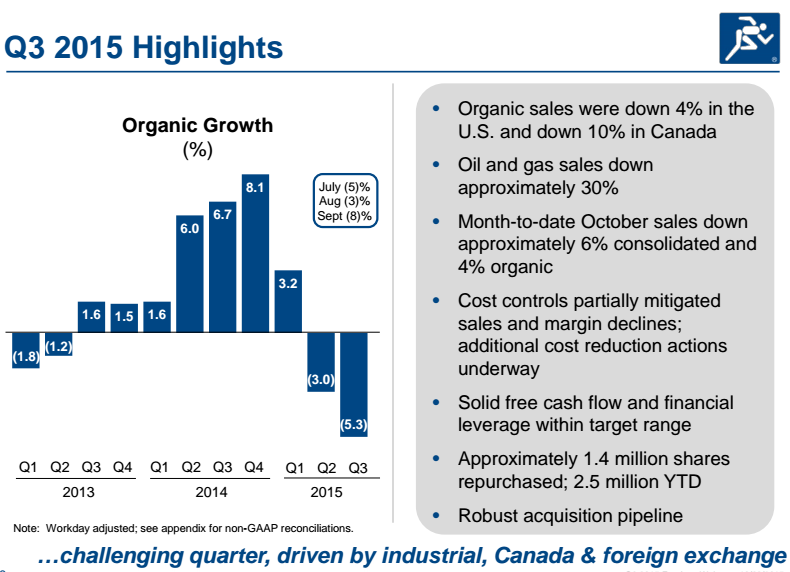

Oil and Gas customers are lowering their expansion and maintenance, hence purchasing less supplies. The Canadian dollar (WESCO derives 24% or its revenues from Canada) has depreciated over 20% over the last two years. As if that is not enough, the industrial sector is experiencing some softness as of late. The slide below, taken from a recent company presentation, reflects how management views the company's current affairs.

(click to enlarge)

(source: Company earnings presentation, Q3'15)

Q3 '15 was horrible with a 5.3% organic decline and a 7.4% consolidated revenue decline y-o-y. Operating profit was down 20%, and net earnings is down for the third consecutive quarter.

The company is fighting the trend by applying cost control measures. It has already eliminated hundreds of jobs, is closing under-performing branches and is reducing discretionary spending, aiming to achieve savings of $0.4 a share in 2015.

The industry headwinds may turn out to be good for WESCO in the long term. With such a fragmented industry, and so many smaller players struggling,WESCO has the wherewithal not only to live through the difficult period, but also to scoop up and buy smaller local and regional distributors on the cheap. Management did indicate in its latest conference call that it sees a robust acquisition pipeline.

The Valuation

Were you a growth investor, being accustomed to a consistent 10%+ average earning growth rate over the last ten years (with a halt during 2009's recession), and expecting this growth to extend to maybe infinity; were you a growth investor, witnessing Gas and Oil's dire situation, seeing how the Canadian dollar continues its endless decline with no end in sight; seeing the softness in industrials; were you a growth investor having no clue when all this pain will come to an end - would you keep being long?

In one word - No.

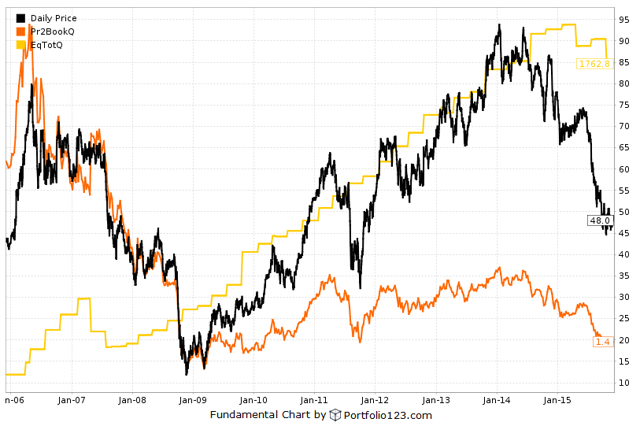

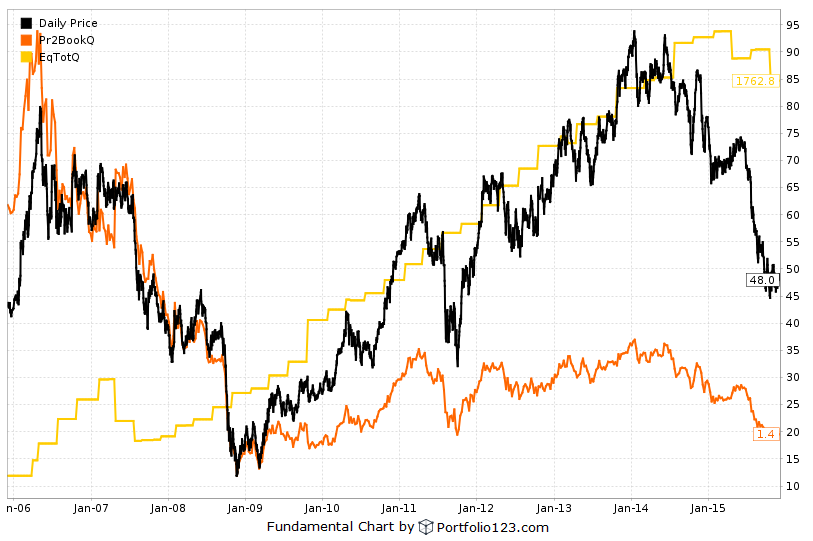

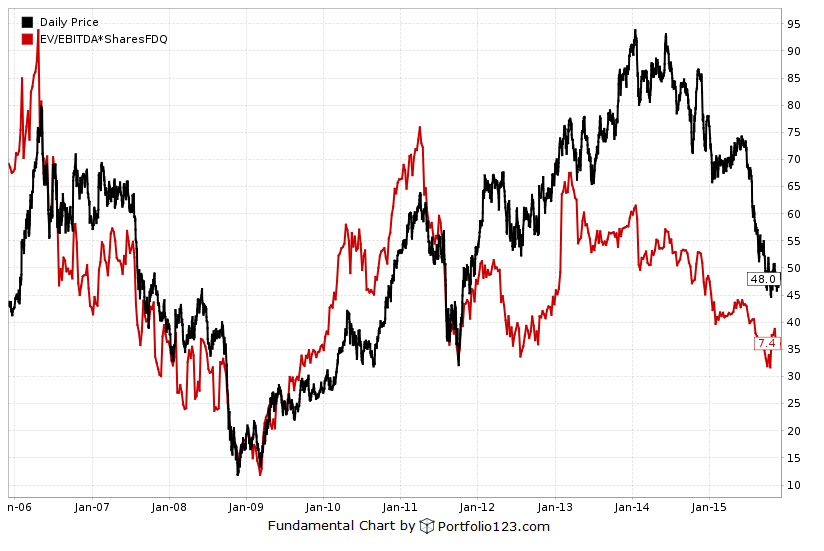

In one graph -

(click to enlarge)

The decline in the stock price is perfectly aligned with the halt in revenue growth.

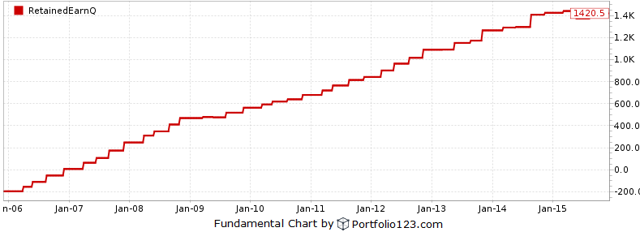

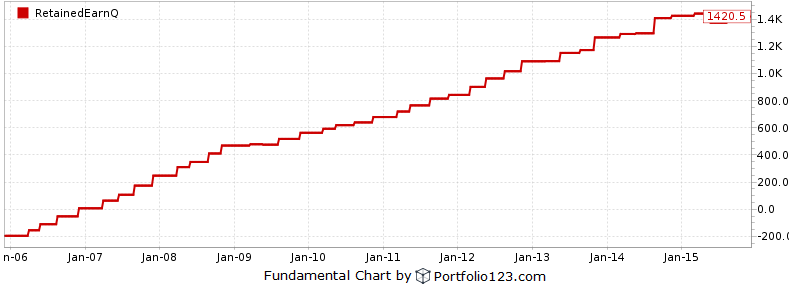

At $44 a share, the company sells at a price to book of 1.22x, which is near the low end of its 10-year valuation range, except for 2009, in the midst of the market scare. To provide some perspective, I find the following figure of quarterly retained earnings extremely telling on the company's cash generation ability. Retained earning is a balance sheet item which is part of shareholder's equity. Looking at retained earnings eliminates the effect of stock repurchases (WESCO bought $115M of its own stock in 2015 alone), stock issuance (e.g. through option exercise), and also non controlling interests (negligible in WESCO's case).

(click to enlarge)

While I have not measured it accurately, it seems obvious from the figure above that retained earnings have been growing in excess of 20% a year, in much a consistent way over the last ten years. With WESCO showing a positive net income in each one of the last ten years, even during '08-'09, I need no other proof for the company's ability to survive as a going concern in the foreseeable future. Return on equity peaked to above 30% in 2007 and 2008, just before the crisis years, while hovering between 10% and 17% following the crisis years. TTM return on equity stands today at levels of just under 13%, which are adequate in my opinion for this type of business, and have ample room to grow, once headwinds fade away.

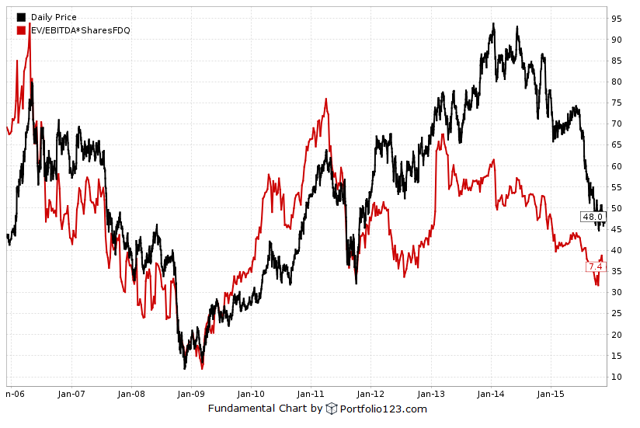

The price looks cheap also when inspecting the EV/EBITDA measure, compared to the company's own valuation history.

(click to enlarge)

To keep my valuation analysis simple, I'll use P/E to assess whether WESCO is cheap. The average net income over the ten years 2006-2015 is $205M. Current TTM earnings, depressed due to headwinds described above, is $234M. Let's assume a worst case assumption that the company never grows again, and to be extra conservative, let's assume that the average earnings going forward remain at $205M levels forever. The P/E over the last ten years ranged from 7x (in 2008, in the outbreak of the financial crisis) to 16x. With a market cap of just above $1850M, the market is valuing WESCO at 9x our conservative earning power estimate.

I believe that the consensus is overly concerned and misses out on two basic facts. The first, the company's headwinds might be of a temporary nature. At one time or another, Gas and Oil prices may rebound, the Canadian dollar may rebound, or industrials will continue growing again. The current depressed valuation does not even account for such optionality.

The second, the risk profile of the company's debt is much reduced today, compared to just three months ago, thanks to the successful refinancing of $440M revolving credit which was due in 2016. In addition, $177M of expensive convertible debentures (13.8% interest rate), which were issued at 2009 when the company did not have many other choices to raise funds, will be open for early redemption starting September 15, 2016. I do expect the company to redeem those bonds, and stop bleeding hefty interest rates.

Should the company return to normality, let's say in the next 2-3 years, I believe that there's a fair chance that it can trade above 12x earnings of $260M, which is only 10% above TTM earning, and still lower than earnings in 2013 and 2014. Such a valuation would result in a market cap of $3120M, 70% above today's level.

Management and Owners

John Engel leads the company as CEO since 2009, and as a director (and now a Chairman) since 2011. He also serves also on the board of US Steel (NYSE:X) as a director and chairman of the audit committee. Mr. Engel owns $4M worth of the company's stock. Former COO, Stephen Van Oss, who retired (or was dismissed) during 2015, owns even more stock, close to $5M worth. In total, insiders own 16% of the company's stock, so should be incentivized to see it appreciate in price.

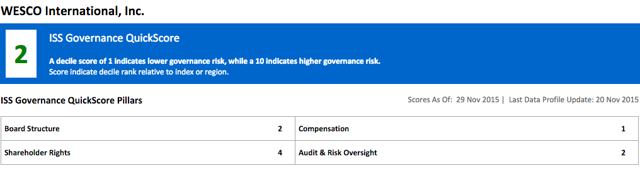

The ISS quickscore, which measures the risk involved in companies' corporate governance affairs, is surprisingly low. I have rarely seen such good scores for the companies which I analyzed. This fact is very encouraging.

(click to enlarge)

A notable shareholder of the company is Atlantic Investment Management, which has filed a SC 13D in April this year, disclosing a 5% stake, which indicates it has intentions to take an activist role. Atlantic has not yet disclosed what its activist plans are.

Summary

WESCO is cheap, both objectively and compared to its long-term valuation history. WESCO is safe - it has a valid business model, a diverse customer base, and it is diversified geographically. WESCO is led by competent managers who own a fair stake in the company's stock. Its corporate governance structure is clean. WESCO suffers from a cessation in its growth due to headwinds in the industries it serves. It is well financed and conservatively structured to weather those headwinds. It takes advantage of the industry's situation to systematically reduce costs and expand through acquisitions. Once the pendulum swings back - and the pendulum always swings back, as taught us by Howard Marks, WESCO will remain a stronger company, trading at much higher levels. Uncertainty regarding the timing of that scares away short-term oriented investors and creates an opportunity for long-term oriented once.

No comments:

Post a Comment