Summary

- Shopify IPO allows investors to gain a return from the strong growth of e-commerce.

- Shopify has many untapped markets left.

- Shopify shares offer high potential returns if management can continue strong growth and eventually turn a profit.

After reviewing Shopify (Pending:SHOP) FORM F-1 extensively, I have summarized all the main points and reviewed the company, risks, competitors, share price and the current state of the e-commerce industry in this article. As a previous user myself of Shopify when launching my e-commerce business I can speak to its solid platform, ease of use and outstanding customer support.

Overview

Shopify is Canada's first internet startup since the dot com crash to reach a billion dollar valuation and one of only 39 firms created in the US and Canada since 2003 to reach a billion dollar valuation. Shopify is a cloud based commerce platform that allows brands to run their business across all sales channels from their websites to brick and mortar stores. Shopify's platform allows brands to manage their products and inventory and process payments and orders. Shopify allows brands to handle spikes and dips in sales from their websites with ease and is used by over 160,000 stores in 150 countries, by brands from Tesla, Google, Wikipedia, WWF to mom and pop stores.

Business

(click to enlarge)

(click to enlarge)

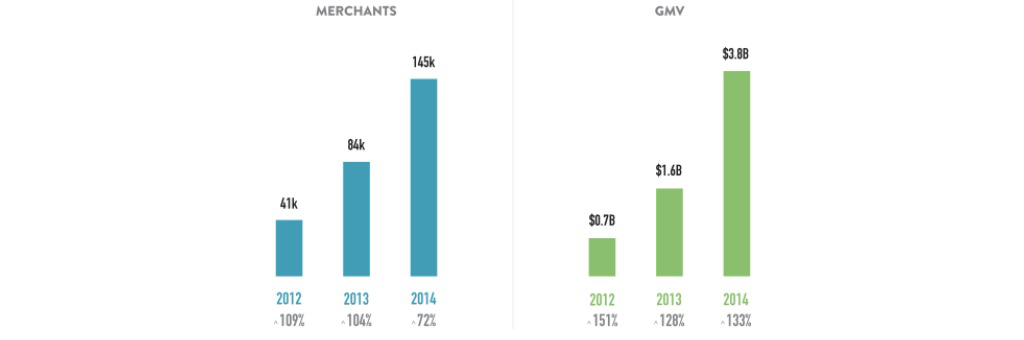

Fig 2: Shopify growth in merchants and merchant sales

Shopify has on average almost doubled its merchant base every year for the past 3 years and more than doubled merchant revenue every single year for the past 3 years. Shopify has stated that it has identified over 46 million merchants worldwide with less than 500 employees which it sees as its target market. This leaves significant growth potential ahead for Shopify from its current 160,000 customers, even if it were to only capture a small percentage of this overall market.

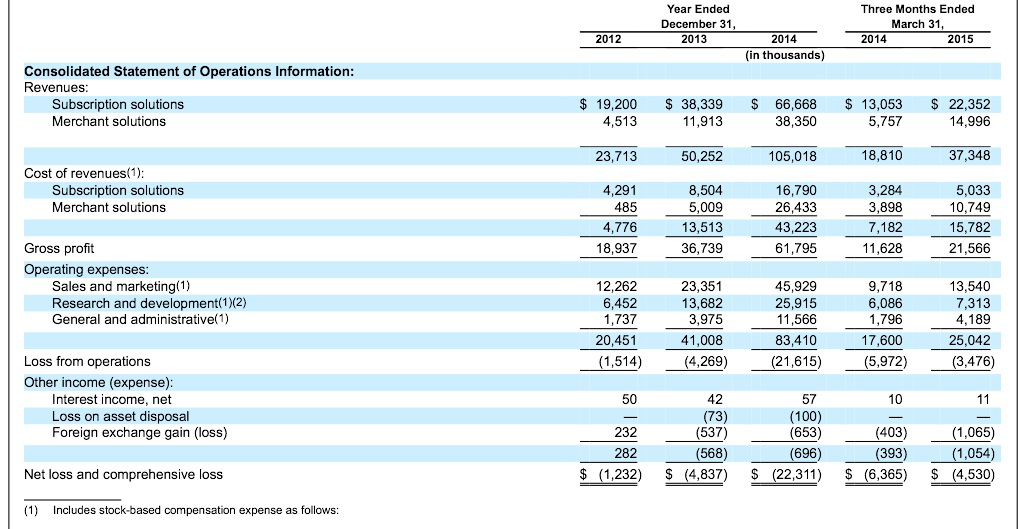

(click to enlarge) Fig 3: Shopify financial statement

Fig 3: Shopify financial statement

Fig 3: Shopify financial statement

Fig 3: Shopify financial statement

Shopify breaks down its revenue into Subscription services and Merchant solutions which I describe in more detail below. Total revenues from Subscription services and merchant solutions have grown by over 100% every year for the past 3 years. That trend looks set to continue for 2015 when looking at the 3 months ended March 31 revenue for 2014 and 2015 which show slightly under 100% growth.

- Subscription Services: Includes subscription fees, payments from sales of website themes, apps, and domain names.

- Merchant Solutions: Includes fees from Shopify Payments (currently only available in Canada, USA, and UK), referral fees, and POS hardware sales. Shopify notes in its filing that Shopify payments has been decreasing its margin however it expects to see little downside in margin going forward, with most of the decrease having already happened.

Merchant solutions revenue growth has been outpacing overall revenue growth at Shopify and it looks like that is set to continue when looking at the 3 months ended March 31, 2015 compared to a year ago. It is also promising to see that during the same timeframe Shopify has significantly reduced losses compared to a year ago.

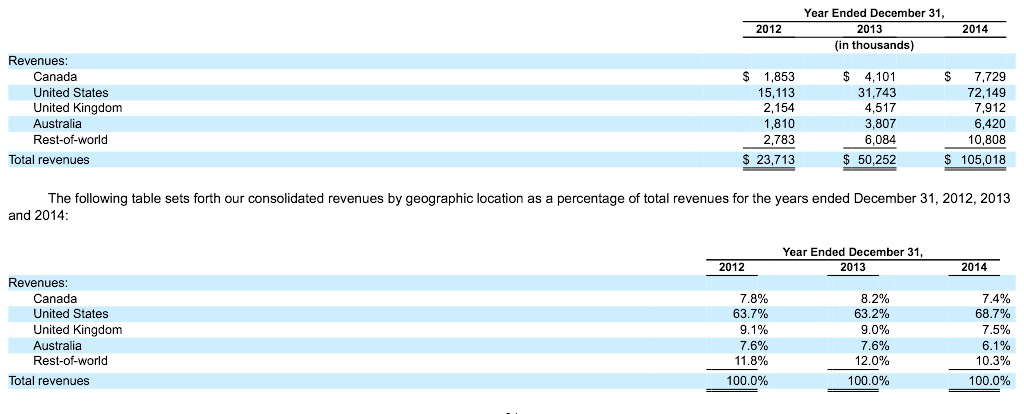

(click to enlarge) Fig 4: Shopify revenue by region

Fig 4: Shopify revenue by region

Fig 4: Shopify revenue by region

Fig 4: Shopify revenue by region

Shopify derives 84% of its revenues from Canada, USA and UK. This is a weakness but also an opportunity for the company. Canada, USA and UK make up only 36% percent of e-commerce sales in the top 10 e-commerce markets and there lies significant opportunity ahead for Shopify if they can tap into the size and growth of other markets.

Shopify is in a unique position in that it can monetize and capture all e-commerce growth without being focused on any particular segment and the risks that would bring. Shopify has stated no customer represented 1% or more of its revenues in 2012, 2013 and 2014. Shopify has strong customer loyalty and works with its 160,000+ stores to build their brands through free tools, guides, video content, books, and a blog. By ensuring the success of its customers it also ensures its own success by creating customers who will upgrade to more expensive plans and process many more payments and orders. Shopify's employees own 20% of the company and are encouraged to act like owners and help build long term value for the company.

E-Commerce Industry

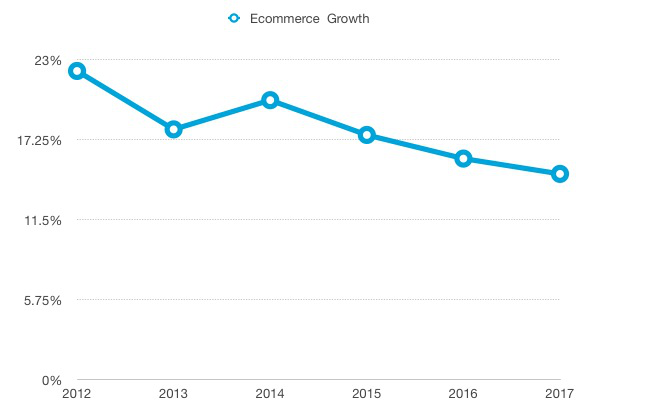

(click to enlarge) Fig 5: E-Commerce growth by year worldwide

Fig 5: E-Commerce growth by year worldwide

Fig 5: E-Commerce growth by year worldwide

Fig 5: E-Commerce growth by year worldwide

The e-commerce industry has seen spectacular growth worldwide in the past few years and it looks like that trend is set to continue which buoys well for Shopify.

(click to enlarge)

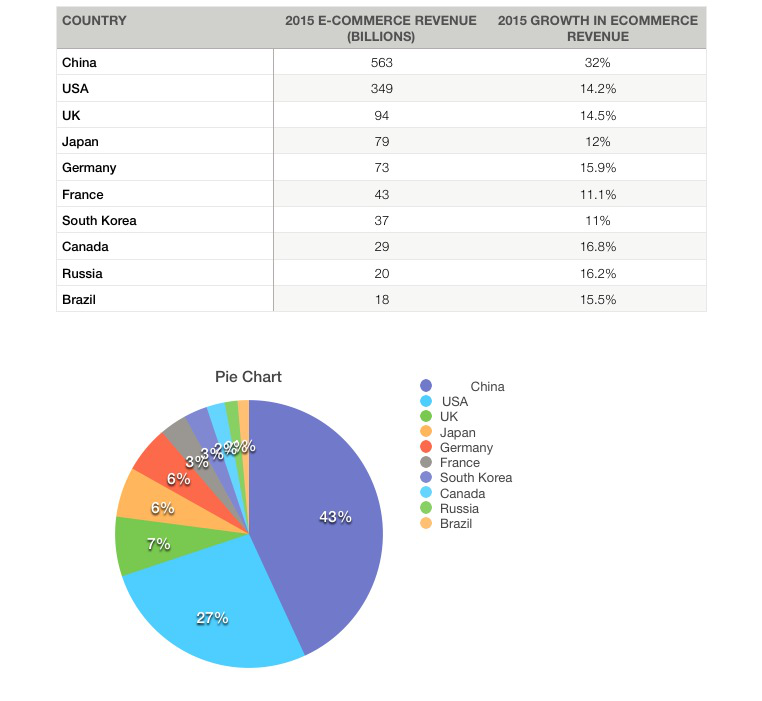

Fig 6: E-Commerce sales as percent of total sales of top 10 e-commerce markets

Analyzing the above data shows the potential for Shopify to grow. 84% of Shopify revenue comes from just 36% of the top 10 e-commerce markets (Canada, USA & UK).

On top of that the markets with the most e-commerce potential are the following, all countries Shopify currently has little presence in.

Country

|

E-Commerce as % of sales

|

Population

|

2015 GDP Growth

|

UK

|

14.4%

|

64.1 million

|

2.5%

|

India

|

0.9%

|

1.252 billion

|

7.5%

|

Indonesia

|

0.8%

|

249 million

|

5.2%

|

Mexico

|

1.5%

|

122.3 million

|

3%

|

Risks

Shopify outlined many potential risks in its F-1 filing and I go over the ones that I believe are the most likely to occur out of all of them.

- The business may be harmed if growth is not managed effectively

- They may fail to keep up with innovation and lose customers due to this

- Competition may intensify

- A security issue may occur such as a breach of the servers that store personal data of the millions of customers that have used shopify, or a software bug/hack that causes significant lost sales and brand damage

- Company may be unable to make a profit

Competition

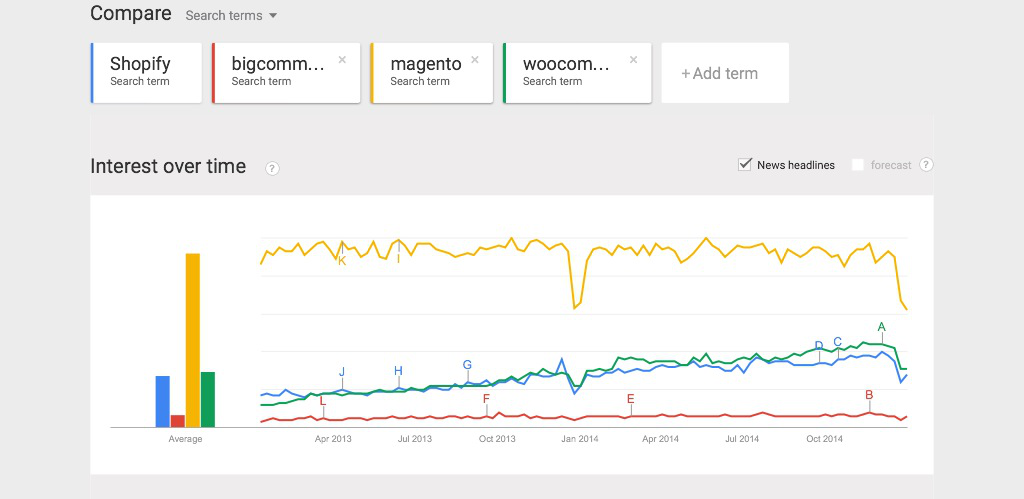

Shopify's main competitors are BigCommerce, Magento, and WooCommerce. I did a quick search using Google Trends to get a rough idea of how they stack up.

(click to enlarge) Fig 7: Google Trends data for Shopify's biggest competitors

Fig 7: Google Trends data for Shopify's biggest competitors

Fig 7: Google Trends data for Shopify's biggest competitors

Fig 7: Google Trends data for Shopify's biggest competitorsBigcommerce:

Bigcommerce boasts that it has 90,000+ stores compared to 160,000+ at Shopify. Google trends however shows fairly consistent use of BigCommerce worldwide for the past 2 years while Shopify has seen a steady increase. I did a Google search "BigCommerce VS Shopify" and read the top 5 articles that did a comparison of both platforms. 3 of the 5 articles swayed towards Shopify as their preferred platform while 2 articles maintained a neutral view.

Magento:

Magento has 240,000+ stores compared to 160,000+ at Shopify. Magento boasts that Vizio, Olympus, Rosetta Stone and Nespresso are some of its customers. Google trends shows it as the clear winner for the past 2 years however it looks like recently that is beginning to change. I did a Google search "Magento VS Shopify" and read the top 5 articles (excluding the one written by Shopify) that compared both platforms. 1 article picked Magento as the winner while 4 preferred Shopify.

WooCommerce:

WooCommerce has 663,153 websites using its platform compared to 160,000+ at Shopify. Google trends shows it steadily increasing at an almost identical rate to Shopify. I did a Google search "Woocommerce VS Shopify" and read the top 5 articles (again excluding the one written by Shopify) that compared both platforms. 1 article picked Shopify as the winner, 1 picked Woocommerce and the other 3 remained fairly neutral overall. Woocommerce appears to be widely used by small brands and does not boast of any large names using its platform.

Shopify will gain user growth by being the platform of choice when business owners perform the Google searches I did when looking for a platform to host their store on. While Shopify was the clear winner against Bigcommerce and Magento, it will need to up its game against Woocommerce if it wants to be the best hands down. However with e-commerce growth at 17.7% this year followed by 15.9% next year there will be opportunities abound for Shopify and Woocommerce to see significant growth in the years ahead without having to be at each other's throats.

Share Value

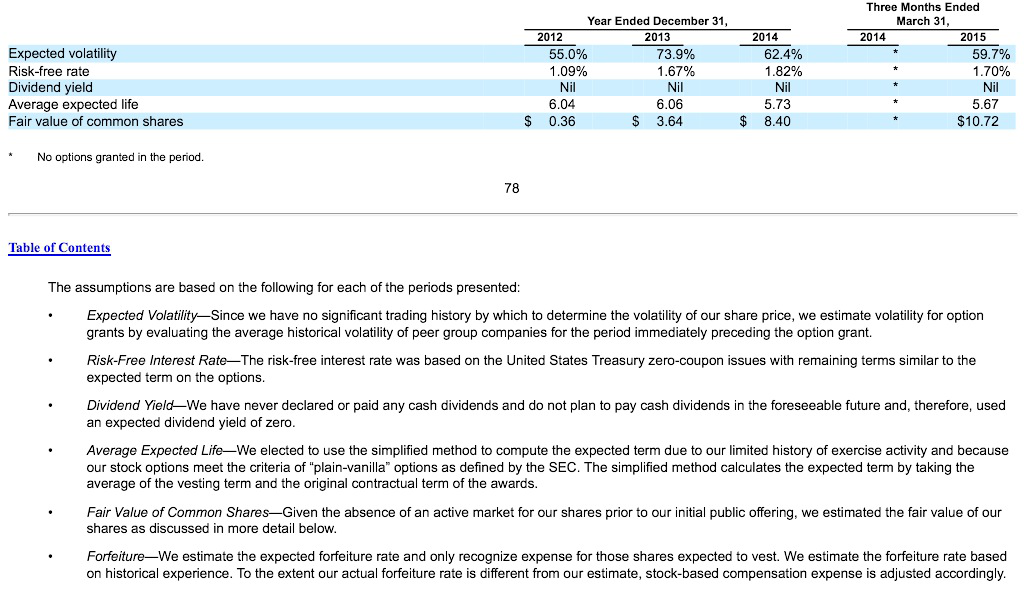

(click to enlarge)

Fig 8: Shopify change in share value

Shopify has went from a fair value of $0.36 per share in 2012 to $10.72 today. To get a very rough idea of what it should be worth on the market I looked for companies with similar revenues, and similar revenue growth while being slightly unprofitable. I opened up Finviz and did a screening with the requirements of the stocks having a market cap under 10 Billion, being in the technology sector, sales growth of over 30% and insider ownership over 10%. I got back a list of companies and found two that most resembled Shopify. The companies were Hubspot and Paycom which I go into a little more detail on below;

Hubspot

- Revenues for 2014 of $115.9 million

- Not profitable

- 49% revenue growth

- $1.6 Billion market cap

- Revenue multiple of 13.8

Paycom

- Revenues for 2014 of $150.9 million

- Profitable

- 40.3% revenue growth

- $2.06 Billion market cap

- Revenue multiple of 13.73

Shopify has over double the revenue growth of both Hubspot and Paycom but showed and slightly lower revenues for 2014, however in 2015 Shopify should see revenue exceed both these companies. By taking the median revenue multiple of Hubspot and Paycom and multiplying it by Shopify's 2014 revenue of $105 million we get a $1.445 billion market cap. Based on shares at $15 giving a $1 billion dollar market cap this would give a rough value of $21.67 for its shares currently and $43.20 this time next year if Shopify can double revenue once again this year and market conditions don't change. This may change however if Shopify management chooses to pursue a secondary offering down the road and original shareholders shares get diluted.

No comments:

Post a Comment