45 comments | About: Stratasys, Inc. (SSYS), DDD

Summary

- The 3D printing market is real, and is now trading at an attractive entry point.

- 3D Systems has a strong focus on growth through acquisitions, which have not proven accretive for the stock price other than garnering attention through headlines.

- Stratasys offers a superior product at a discount based on forward multiples.

- SSYS leads DDD in the industrial and consumer sectors, which seem to have the strongest long-term potential.

I first initiated large positions in Stratasys (SSYS) and 3D Systems (DDD), and a small position ExOne (XONE) last fall prior to the huge run up in price. At that time, my knowledge of the 3D printing market was minimal at best, and I was entering based solely off the momentum I believed would carry the prices higher. I ultimately sold DDD and XONE in early February once the 3D market started being sold off. I maintained my position in SSYS and lowered my cost-basis at the dip when I got in around $95. In the long term, I believe SSYS is poised to significantly outpace the broader 3D market, specifically DDD as these are currently the two major players.

Is the 3D printing market real or just hype?

This question has had drastic implications for the greater 3D printing market, and I am here to tell you it is 100% real. I prefer to invest in companies that offer products and services to a variety of industries, and 3D printing is a market that does just that. 3D printing has the ability to revolutionize the manufacturing industry by increasing efficiency and margins for manufacturers, and has strong demand from a multitude of industries such as the automotive market, defense industry, education, etc. While this hype resulted in a mini-bubble in January and February, the sell-off resulted in stock prices that demanded high multiples not due to hype, but due to growth expectations. The market as a whole is expected to grow at a stellar rate as high as 45.7% annually through FY2018. This growth rate would result in a market of over $16 billion.

Companies like Wal-Mart (WMT) recognize the potential of this technology and how it can transform their business to cater to the everyday consumer. In-store manufacturing of goods would drastically reduce costs for Wal-Mart, while also providing the consumer means to acquire products such as replacement parts which usually take 2-3 days to deliver. General Electric (GE) will begin using 3D printing to manufacture fuel nozzles for jet engines which will be both lighter and more durable then nozzles manufactured by traditional techniques. These fuel nozzles represent the greater potential of 3D printing for on-the-spot manufacturing of any type of product from jewelry to children's toys to electronics.

The business model of 3D printing companies is similar to traditional printers in which the actual machine is sold at fairly low margins and the materials (ink in traditional printers) are sold at extremely high margins. As the industry transitions from the sale of printers to the sale of materials, margins will undoubtedly rise in conjunction with earnings. In summary, the fact that some of the largest companies are forging business partnerships with (or possibly trying to acquire) various 3D printing companies shows the potential growth for this market as a whole.

So who stands to benefit?

As this market continues its rise, SSYS is in the best position to outperform its peers due to a far more proven management and more sustainable business plan. Stratasys outperforms 3D Systems in a few key areas including, but not limited to: the consumer market, industrial market, and acquisition quality.

Stratasys acquired MakerBot last Fall in an effort to boost its consumer presence and branch out from its roots where it has dominated in the industrial sector. This set up a battle of sorts between SSYS and DDD to see who could roll out the best consumer-friendly printer. So far, it seems that the MakerBot has significantly outperformed the Cube 3, giving SSYS the early lead in a race that will surely take years to play out. Even by looking through Amazon reviews for the two printers, it is clear that consumers prefer the MakerBot. Wall Street analysts tend to agree and consensus estimates show revenue derived from MakerBot sales growing at a clip over 50% through FY2016. While the consumer market may seem like the smallest market because of practical reasons, as the technology for the MakerBot improves and expands into new areas, it will inevitably lead to higher sales.

In terms of acquisitions, DDD's strategy seems to be to make as many headlines as possible, while SSYS kept a fairly low profile up until its MakerBot acquisition. The sheer amount of M&A at DDD may make it seem like the superior company, but management has not proven an ability to derive significant revenue from many of these acquisitions. In addition, many of them simply do not gel and make the overall business strategy seem haphazard, evident in the fact that it has made over 50 deals in the past three years. In contrast, SSYS has been very strategic about acquisitions and all have been significantly accretive to the stock price. SSYS also boasts over $600 million of cash on hand and no debt, giving it the ability to continue focusing on M&A activity that builds upon the strong, pre-existing segments of the company.

The industrial sector could very well end up having the largest market considering how 3D printing could redefine the traditional design-to-manufacture method. It is this market that I predict SSYS can truly dominate as well. With a 54% market share versus DDD's 20%, SSYS is already beginning to differentiate itself from competitors. The barriers to entry into the industrial sector are significantly higher than the consumer market, and demand a lot of R&D. SSYS continues investing heavily to better its already superior product. There is no reason to think SSYS will lose the competitive advantage in its technology and should continue raking in a larger market share in the coming years.

Valuation

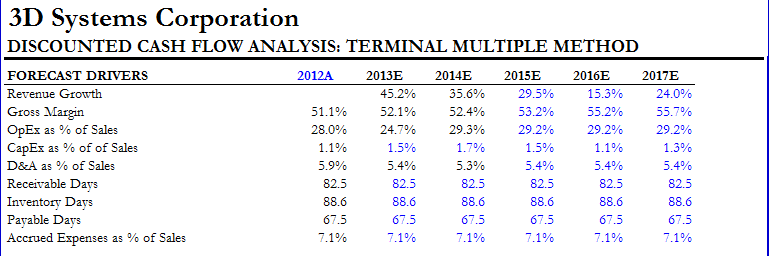

SSYS could very well be the superior company, but valuing its growth prospects is important to gauge the upside for both companies. It is hard to define a peer group for 3D printing companies since there are limited amounts that are actually involved in the printer distribution segment. Because of this, comparable companies' analysis is nearly impossible. Instead, I ran a DCF for each company. I ran the same exact model for each company, just switching out the assumptions. Below are the forecast drivers and sensitivity analysis for DDD.

(click to enlarge)

I applied the same WACC (discount rate) and EV/EBITDA multiple to both DDD and SSYS. News since I made this model would infer that the price target for DDD should be towards the upper right portion of the sensitivity analysis (around $68/share). Assumptions for SSYS include revenue growth of 47% in FY2014 with 7% decreases each subsequent year before bottoming out at 26%. I expect net margins to stay constant in the 18-20% range over the next 5 years as well. All other assumptions were made in line with historical averages unless significant activity demanded otherwise. The DCF resulted in a $135 price target with the sensitivity analysis looking the exact same.

The chart below shows the Trailing PEG ratios for both companies over the last 5 years. It is clear that SSYS looks to be much cheaper based on the current price and future earnings potential of the company. While the current P/E ratio of over 110 may scare some investors, the forward P/E of 65 shows just how much earnings for SSYS are expected to grow.

Risks

Risks to my analysis include a technology breakthrough for either DDD or another competitor that eats up a large share of SSYS's market. Also, the high multiples the 3D printing market leaves a lot of room for a decrease in stock price if negative news were to hit the industry.

Conclusion

Even after the recent run up in price, I believe SSYS is a solid buy primed for growth that will outpace the broader 3D printing market. I would suggest purchasing at current price levels and adding on major dips over the next few years, as this is a long-term hold in my mind. I maintain a positive outlook on the industry as a whole, and while I believe SSYS is the strongest company right now, I am not suggesting to short DDD by any means.

No comments:

Post a Comment