Summary

- Xplore Technologies is an overlooked pure play on enterprise tablet computing at the beginning of its growth trajectory.

- The low valuation is primarily due to the implied disbelief that XPLR will be unable to capture market share from iPad or other rugged tablets.

- However, customers continue to switch to XPLR as its tablets are more durable and provide superior functionality/performance.

- The recent introduction of a cheaper and lighter weight tablet expands the potential target market by >10x and should drive a >3x increase in revenue over the next several years.

- The lack of debt and $86 million of NOLs mean operating income drops straight to net income while outsourced manufacturing results in minimal inventory and no production related investment.

Company overview

Xplore Technologies (XPLR) sells a line of rugged mobile tablet PC systems and accessories able to withstand hazardous conditions such as extreme temperatures, rain, vibrations, dirt, dust and shocks.

The primary end markets and customers are shown in the chart below.

(click to enlarge)

Source: Company presentation

Never bring a knife into a gunfight - or an iPad into the field

The third place ranking behind Samsung and Apple in a tablet test is more positive than it appears due to a gradually changing paradigm shift among customers. XPLR was the only rugged tablet manufacturer selected out of 19 total vendors so the rank effectively improves to first. The threat from iPad (or a Galaxy) in the enterprise market is more perceived than actual. An iPad may be more than capable of meeting the needs of a mobile white collar workforce (e.g. mutual fund wholesaler), however, it is wholly unsuitable for more demanding environments (e.g. special forces operator, oil rig worker).

XPLR has been a market leader in rugged tablets for more than 15 years due to several competitive advantages. First, its tablets are the most rugged on the market with the ability to withstand a seven foot drop onto concrete, operate underwater and withstand temperatures from −49° Fahrenheit to 160°. Second, its tablets have superior screen technology such as the ability to be viewed in direct sunlight (unlike other tablets) and dual mode input (stylus or finger). Third, its tablets offer the best performance with the Intel Core i7 processor, solid state drive, longest battery life and 4G LTE connectivity, which should not be taken for granted considering that rugged products typically do not have the latest technology. Fourth, it manufactures the only field repairable and upgradeable tablet on the market, which allows a customer to quickly swap out a component whereas the entire tablet from a competitor would have to be sent back for repairs resulting in lost productivity. This feature alone helped XPLR win a large contract from a major telecom company (telco), which has subsequently increased to >$20 million.

Its tablets are even superior when compared to other rugged tablets. A major telco chose to replace the Panasonic Toughbook (the largest competitor) with a more rugged solution. In a series of tests (extreme heat, water submersion, thrown into a washing machine), the XPLR tablet was ranked number one. In a January 2014 presentation, XPLR CEO Philip Sassower said that the tablet from General Dynamics Itronix ranked so low that GD decided to exit the business. This not only created a more favorable competitive environment for XPLR going forward but also allowed it to hire half a dozen of the top people from GD Itronix. Another competitor (DRS Tactical Systems) came in second place although it subsequently exited the consumer side of the business in order to focus on the military side after seeing the performance of the XPLR tablet.

RangerX - the next phase of growth

In July 2013, XPLR introduced the RangerX tablet, a rugged Android tablet with the fastest processor, most storage capacity, 10 hour battery life (enough for a full working shift on one charge), best drop rating, waterproof/dustproof (though not as high as its ultra-rugged tablet) and sunlight readable display. It is also the only tablet with integrated gigabit ethernet and HDMI-In ports (as an option), which allows field technicians to only carry one device and run diagnostic tests on site (e.g. testing video signal or internet connectivity). This feature (which cannot be added to an iPad like a credit card reader) is projected to save one of its telco customers $10 million by avoiding repeated service calls.

RangerX expands the target market from only $500 million (ultra-rugged tablets) to $6.9 billion (enterprise grade rugged tablets). To put the potential growth in perspective, revenue increased 72% from FY11 to FY13 before RangerX was even introduced. Moreover, RangerX should not cannibalize sales of its ultra-rugged tablet line given the different price points ($1,300 vs. $4,000) and intended uses.

Even outside of the ultra-rugged market, the iPad is proving less of a threat. Less than six months after introduction, XPLR received its first major purchase order for RangerX of ~$4 million from a major U.S. telco. This customer had been using iPad and Galaxy tablets that cost half as much but found that they were only lasting six months to a year before breaking compared to RangerX, which has a standard three year warranty. The financial savings alone as measured by the total cost of ownership (e.g. spend $600 on three iPads or $1,300 on one RangerX) should help RangerX continue to steal market share from iPad.

However, the Android version of RangerX only represents a fraction of the expected growth as a majority of XPLR customers rely on the Windows OS. The Windows version of RangerX is currently undergoing beta testing and should be introduced by mid 2014.

Superior technology + new products + new markets = Long growth runway

This growing product suite and two year head start on the competition should allow XPLR to gain significant market share in the larger rugged tablet market. Below are several of the largest opportunities (in addition to the telco market) with specific examples of recent customer wins.

Warehouses/distribution centers are using tablets to increase productivity in core areas such as supply chain management and order fulfillment. An ultra-rugged tablet from XPLR is now installed on all Daimler forklift trucks after it replaced a heavy and bulky computer that had to be installed on a fixed mount (a consumer grade tablet would not be able to withstand the constant vibration). The smaller size and portability provide a significant advantage. At any given time ~20-25% of forklifts are being repaired so a company must have 50 forklifts if it needs 40 in operation. With the older and more expensive solution, Daimler would have needed one computer for each forklift or 50 computers total. However, with the solution from XPLR, Daimler only needs 40 tablets because it can remove a tablet from a forklift being repaired and place it in a working forklift.

Utilities are increasingly using tablets to more efficiently respond to customer requests and power outages. The largest utility in Canada (Hydro One) switched from using the Panasonic Toughbook after finding that it would not work in extreme conditions such as snow and rain.

Energy companies are using tablets for more efficient data entry. Previously, workers would not use a computer on a drilling platform as it could cause an explosion (from sparks) and would not be able to withstand the extreme conditions. If a worker had to record data, they would go to the wellhead with a pad and pencil, write down the data then go back to an office and enter it into a computer. Now, a worker (at PennWest Energy for example) only has to enter data once using a XPLR tablet that can be brought directly to the wellhead.

XPLR tablets have been sold to >300 public safety organizations in the U.S. as well as multiple international organizations. The Abu Dhabi police department became a customer after finding that other rugged tablets could not operate in extremely hot temperatures.

The military is now one of the largest markets, even if the original entry was by chance. Singapore Technology previously sold their own rugged notebook to the military, however they saw the trend towards tablets and asked XPLR if they could be a reseller of its ultra-rugged tablet after seeing it perform. XPLR has customized tablets specifically for the military with features such as a common access card (CAC) reader (which prevents unauthorized use) and the ability to shield the signal normally given off so that it cannot be traced by the enemy. As a result of superior performance in the field compared to its primary competitors Panasonic and DRS, XPLR is beginning to receive reorders. However, these multi-million orders pale in comparison to the potential market opportunity as XPLR estimates that the market for CAC-equipped rugged tablets is 50,000-100,000 units.

The pharmaceutical industry is a source of overlooked growth. Merck chose XPLR to supply tablets for its clean rooms and drug facilities because other devices would short out when washed down with chemical disinfectants.

The OEM market represents a potential source of recurring revenue. In July 2013, XPLR received an additional order of >$3 million for its ultra-rugged tablet from a medical device manufacturer (in this case the tablet is the control unit for a heart pump). Doble Engineering now installs their software on an XPLR tablet as part of its testing solution for hydroelectric power plants. As a result, every time a heart pump or testing solution is sold, a XPLR tablet is sold.

Financials

In the mrq, revenue increased 136% to $14 million (the highest quarterly level in company history) with the new RangerX accounting for ~50% of the increase while the gross margin remained stable at 35%. This topline growth resulted in net income increasing to $890,000 compared to a loss of $626,000 despite a ~47% increase in operating expenses for new product development and increased sales/marketing headcount. This performance is a continuation of the strong top and bottom line growth over the past several years as shown in the chart below.

XPLR is stronger from a balance sheet and cash flow standpoint than ever as evident by the lack of debt, $5.3 million of cash, positive cash flow and ability to fund growth internally.

The sharp reversal in cash flow in the LTM is due primarily to an increase in accounts receivable. However, this is not a concern in light of the successful history of collecting receivables. Specifically, subsequently to the end of the quarter, 57% of the receivable balance was collected.

On the subject of cash flow, the outsourcing of production to Wistron (a Tier 1 manufacturer) allows XPLR to rapidly scale up production in order to meet the expected exponential demand growth. This also results in minimal inventory (only units ordered are produced), eliminates the need for a large upfront investment in production capacity and significantly reduces working capital requirements as XPLR is able to pay for the production with sales proceeds.

Valuation

Although its primary competitors are either private or owned by larger corporate parents (Panasonic, DRS is owned by Italian defense contractor Finmeccanica) a relevant peer comp is possible using a past deal multiple and recent IPO filing.

In August 2005, General Dynamics acquired Itronix for "a few hundred million" according to Mr. Sassower (terms of the deal were not disclosed). Assuming GD paid $200 million, this would have resulted in a P/S multiple of 1.3x assuming $150 million of revenue for Itronix.

A much more recent example is action-camera company GoPro, which is expected to be valued at more than $2.3 billion (the valuation for the company when Foxconn Technology invested in December 2012) when iteventually goes public.

Even assuming the valuation remains unchanged, this results in a P/S multiple of ~2.3x on 2013 revenue of ~$1 billion. Compared to these two higher multiples, XPLR is undervalued at an EV/Revenue multiple of only 1.2x.

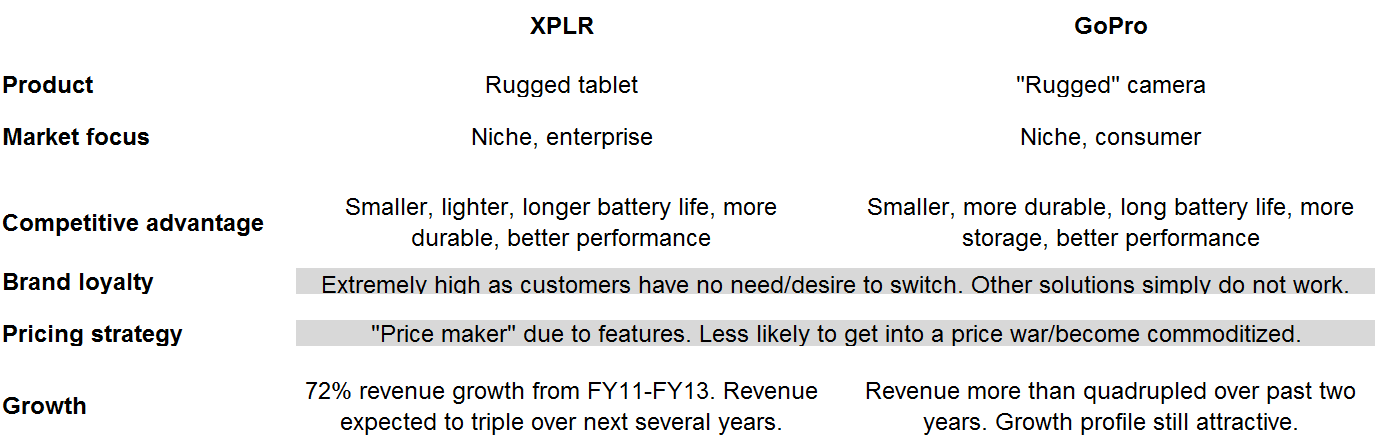

Despite being in a different market, GoPro and XPLR share many similar qualities as shown in the chart below.

(click to enlarge)

However, XPLR is more attractive from an investment standpoint due to its smaller size, low investor/customer following and location in terms of its growth trajectory. Mr. Sassower said that revenue should more than triple over the next couple of years with growth primarily driven by the RangerX tablet.

Assume XPLR is able to reach a $100 million revenue run rate within three years. Assuming a gross margin of 30% and SG&A/R&D margin of 15%, this produces operating income of $15 million. There is no debt so the interest expense is zero, which means income before tax is also $15 million. XPLR has $86 million of NOLs so other than a minimal amount of AMT, cash taxes are effectively zero, which again means net income is $15 million. In October 2012, XPLR converted all outstanding preferred shares into commonfollowing an equity raise so there are no more preferred dividends. Dividing net income of $15 million by diluted shares outstanding of ~8.6 million produces EPS of ~$1.74 and a P/E of only 3.2x. Granted the above is subject to change given the multiple moving parts (revenue growth, margins), however it should illustrate the point.

The extremely conservative price target is based on only a P/S multiple of 1x on $60 million of revenue (about halfway to $100 million run rate). Although the 200 DMA right below the current price provides a perfect place for a stop loss, given the longer time horizon required for the thesis to play out (12-24 months; more back-end weighted) a larger stop should be used. Due to the volatility in quarterly results, low float and microcap size, longer-term investors (especially HF/MF building a larger position) should place greater weight on any change in the fundamentals rather than the technicals.

Risks

Below is a discussion of the primary risks to the investment thesis as well as mitigating factors that limit the downside.

Until sales of RangerX ramp up, XPLR is dependent on the ultra-rugged product line for a majority of revenue. However, not only are efforts to diversify the product line already underway (Android RangerX on the market followed by Windows version) but this reduced dependence on a single product in a relatively smaller niche market should result in a higher multiple.

In FY13 two customers in the U.S. (where XPLR generates a majority of its revenue) accounted for ~28% and 15% of overall revenue, respectively. However, both of these customers are resellers so XPLR should be able to replace them much easier than if it lost a direct end user customer, which only accounted for 4% of overall FY13 revenue.

Quarterly results have been volatile as the shipment of a large order in one quarter may result in a steep decline in sequential or y-y growth. For longer-term investors this is less of a concern (if at all). In addition, any seemingly disappointing quarterly results need to be placed in context (see below for an expanded discussion).

XPLR is subject to the same macro risk of lower spending during periods of weaker economic growth. However with the addition of the Android/Windows versions of RangerX, going forward XPLR should be less vulnerable to lower overall IT spending for two key reasons.

First, its target enterprise customers are at a critical inflection point in terms of future purchasing decisions. Over the past several years many companies, organizations and governments began to give their more mobile workers tablets in order to increase productivity. While the intention was obviously good, the execution was not as the tablets either quickly broke and/or lacked the necessary performance and functionality. As a result, there should be a coming "replacement wave" as these customers realize that more popular and/or cheaper tablets are not necessarily the right choice for them. Moreover, these expected orders are independent of any of the other significant demand drivers.

Second, as just discussed, XPLR tablets do increase productivity, the need for which actually increases in a recession in order to offset lower topline growth. For example, the $10 million its telco customer is expected to save by preventing repeated service calls does not have to be "made up" by firing workers and can be used for more productive purposes such as increasing capex (or making cable boxes more user friendly).

There are two additional risk-limiting factors. First, the previously mentioned collection of more than half of the accounts receivable balance resulted in net cash increasing to $11.4 million or 25% of the market cap, assuming all other cash flow items remain constant (or add to cash). Second, insiders (who own 37% of the stock) clearly believe in the company story and represent a stable long-term shareholder base. On a related note, insiders (including the Phoenix Venture Fund) could opportunistically increase ownership by acting as a "strong hand" in the event of any further short-term weakness not supported by the fundamentals.

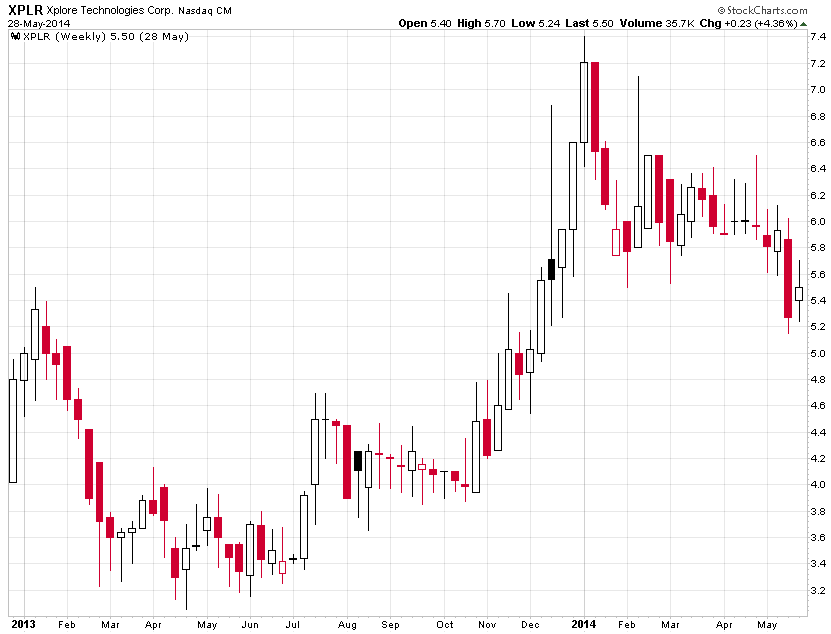

A less obvious though very real risk is that the stock is much more dependent on news flow than more visible tech growth stocks. Unfortunately the news vacuum during the "shoulder season" in between earnings releases and major product announcements is filled with negativity by investors. As shown in the weekly chart below (this time frame was chosen for the sake of clarity) the stock sold off in 1Q13 as the only significant news item was theearnings announcement. Apparently the market was disappointed with the top line growth as the stock fell ~25% over the next two weeks. However, the following point bears repeating as it is largely responsible for the inability of the market to properly react by placing earnings results in context. Revenue only decreased 34% due to the fulfillment of a large order in the prior period, which created an unfavorable comparison a year later.

A positive example is the ~25% gain over two weeks following the introduction of RangerX in July 2013. However, a more recent and relevant example that highlights the price appreciation potential is the ~80% gain in less than three months beginning in November 2013, which was driven largely by an earnings release that was better received and the announcement of the first RangerX order. A rhetorical question for investors to consider is this: If the stock rose 80% based on a $4 million RangerX order and flat y-y revenue growth in the quarter, how much will it rise as revenue more than triples to $100 million over the next three years?

(click to enlarge)

The reverse split and equity raise in 2012 should be considered one-off events that only highlight the progress XPLR has made. Regarding the split, this coincided with the uplisting from the OTC to the NASDAQ. Regarding the equity raise, this was done to provide funds for sales/marketing expansion, product development and working capital. However, there is no need for any financing going forward (much less an expensive equity raise) given the strong balance sheet, increasing cash flow and minimal working capital requirements.

Conclusion

The ~25% pullback from the high in January provides an attractive entry point into an overlooked stock with no analyst coverage on the verge of exponential growth due to a sustainable competitive advantage, a "game changing" new product and expansion into new markets. However, the low valuation will not continue indefinitely as the surprising inability of investors to associate XPLR with the secular trend towards increasing tablet use will be replaced by the realization that it is one of the few pure plays left at the beginning of its growth trajectory.

Editor's Note: This article covers a stock trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks

By John Leonard

No comments:

Post a Comment