- Following Ares' unsuccessful takeover bid in 2010, Stallergenes has lagged the market rally.

- Presently the stock trades 10% below the takeover price offered back then, which was deemed to be far too low.

- In the meantime, sales and earnings have increased 30%, indicating substantial undervaluation.

- While Stallergenes trades at 18 times expected earnings for 2014, Danish competitor ALK trades at 24 times 2016 forward earnings.

- Another buyout offer is in the cards as well as a substantial re-rating of the stock.

(Editors' Note: Stallergenes trades on the Paris Stock Exchange under the ticker symbol GENP.PA, with €300K average daily volume).

The company

The company was founded in 1962 as part of Institut Mérieux, back then world leader in vaccines, and became a leader in allergen immunotherapy through the merger with Institut Pasteur's allergen division. After the acquisition of Bayer Pharma's allergy division, Stallergenes became the worldwide no. 2 in its field.

Allergy immunotherapy

It is estimated that 20 to 30% of the developed world's population suffers from allergies. Generally, allergies are treated symptomatically with antihistamines, antileukotrienes or corticosteroids. These different treatments temporarily reduce and soothe symptoms but do not prevent their reappearance when treatment stops. The market is considered to be mature with few new products in development.

Unlike symptomatic treatments, allergen immunotherapy (abbreviated to AIT) seeks to re-educate the immune system to normalize its response to the presence of the allergen. It has been used for more than 100 years as a desensitizing therapy for allergic diseases and represents the only potentially curative way of treatment.

Stallergenes offers a complete range of products for AIT: injectable (subcutaneous injections), liquid sublingual (drops placed under the tongue) and solid sublingual (rapidly dissolving tablets placed under the tongue). Sublingual liquids and tablets make up 86% of Stallergenes' sales, injectable liquids represent 11% of sales. The remaining sales are made with a range of in vivo tests and preventive products such as dust covers.

As far as patent protection is concerned, Stallergenes states that the company

benefits from limited patent protection but the complexity of the biological process of allergen extraction nevertheless constitutes a significant barrier to entry for potential competitors. Stallergenes manages the concentration process which, on the whole, cannot be patented. All in all, in the allergen field, process management is just as important as patent protection and constitutes a significant barrier to entry that limits the risk of generic copies through similar biological processes. It is therefore most likely that a competitor seeking to develop a similar biological process would have to commit to clinical development lasting several years before being able to market a competing product. (Source:2013 annual report)

As such, a process requires large investments and the market is still small, while regulations have recently become more restrictive, the future will likely see industry consolidation - to the benefit of the larger players. Some of this has already happened, as Stallergenes and ALK have a combined market share of 56%, with the Danish company holding a slightly larger share compared to the French one.

Product development and clinical test series have shown little development risks when compared to other biotech products. This is probably due to the simple fact that Stallergenes' products are based on naturally occurring substances which are unlikely to cause serious side effects.

Financials

Currently, the company's stock trades (rather thinly) on the Paris and Frankfurt stock exchanges at about €54 per share, resulting in a total market capitalization of €740 million.

Stallergenes is superbly managed and has grown sales and earnings steadily over the past decade. Earnings have grown at a CAGR of 15% and I expect 2014 EPS to come in at about €3 per share. Having about €10 net cash per share on its balance sheet, on a cash adjusted basis the stock trades at only 15 times forward earnings. Note that over the past decade the stock has never traded below 14.5 times forward earnings, not even during the worst market panic in 2008/9.

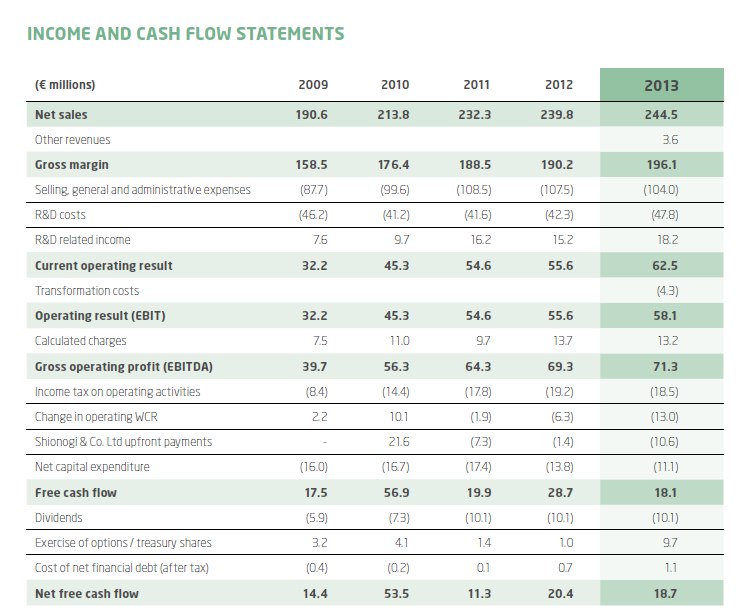

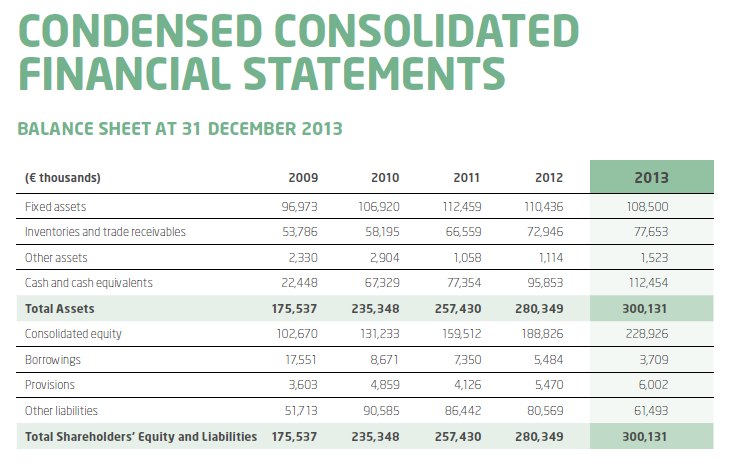

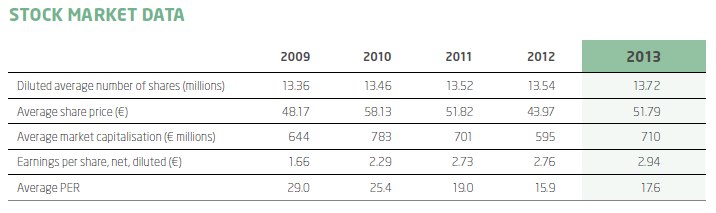

Here are some basic figures taken from the 2013 annual report that show an incredible stability of results and an ultra-clean balance sheet.

(click to enlarge)

(click to enlarge)

(click to enlarge)

The AIT business seems to very attractive, with solid net margins of more than 15% indicating good pricing power and a ROE of 20-28% (it has decreased in the past few years only because of the growing net cash position). According to the2012 annual report, maintenance capex is limited to only about 5% of sales, which explains the huge cash pile Stallergenes has accumulated over the past business cycle.

Ares Life Sciences' 2010 takeover bid

Ares Life Sciences is a privately held partnership that focuses on life science companies. In autumn 2010, Ares first bought a 46% stake from the Wendel Group and then offered to buy even the rest of shares outstanding at the same price of €59 per share. As Stallergenes could not avoid to clarify, the bid was very low. Shareholders expected a price of at least €70. Only half of the remaining shares were tendered and Ares, having reached only 73%, had to keep the stock listed.

Soon after the offer period had ended, European stock markets crashed (summer 2011). Due to heavily reduced liquidity, a free float worth only about €100 million and little institutional interest, the stock went down to €45 and has recovered only 20% since that time.

Ares is a long-term investor and is heavily involved in Stallergenes' day-to-day operations. It is also significantly involved in the international expansion plans. To support the US expansion, Ares has even acquired two US companies: Greer, a leading developer and provider of allergy immunotherapy products and services for treating humans and animals, as well as Antigen Laboratories which provides quality allergenic extracts and ancillary supplies to the allergy profession. So there can be little doubt about the fact that Ares is in for the long term, still believes in Stallergenes' future and would very much like to hold 100% of it.

Clear undervaluation

1. The stock trades 10% below the old takeover price, which was inadequate already back in 2010, but earnings and sales have grown 30% since then.

2. Danish competitor ALK (OTCPK:AKABY) (OTC:AKBLF) that has similar market share and a very similar product portfolio is trading at a far higher multiple: 24 times 2016 estimated earnings and 41 times 2014 estimated earnings. ALK has a history of lumpy growth and low profit margins which prompted management to start a deep portfolio restructuring program. Hence, at least in the near term, earnings at ALK are forecast to grow faster than at Stallergenes. However, even if ALK manages to improve profitability according to its restructuring program, margins would still be somewhat lower than Stallergenes' today. Furthermore, an acquisition is at least as unlikely as in Stallergenes' case, because both companies have large, long-term focused anchor investors.

3. Since 2010, Stallergenes has substantially expanded its international operations. Its flagship innovation Oralair has been granted marketing authorisation by the FDA for the treatment of grass pollen allergy.

4. ALK has entered a partnership with Merck (MRK) to launch its own immunotherapy tablet, approved shortly after Stallergenes'. While this presumably strong competition is seen as a negative by analysts, it can actually be considered very positively. Let me explain this further:

Even though it is practiced by most allergy specialists in the US, allergen immunotherapy is primarily administered subcutaneously, requiring multiple injections of allergens under medical supervision. The new sublingual tablet therapy could be disruptive for their business, as allergists would have much less (paid) work to do. They would not need to mix the allergens and would not need anymore to give the shots. In fact, there have been reports that allergists are quite afraid of the new treatment. Now, if a huge pharma company like Merck puts its marketing muscle behind this treatment, there is a far better chance to increase public awareness of the genuine potential and step forward for patients offered by tablet therapies.

Here is a good NY Times article illustrating the current market situation. It also indicates why Stallergenes' Oralair (that offers a combination of five different allergens) could well be considered to be superior to ALK-Merck's tablet (that contains only one specific allergen):

"It's rare that somebody comes in and they are just allergic to one grass," said Dr. Rohit K. Katial, professor of medicine at National Jewish Health in Denver. "Generally, people who are allergic tend to be allergic to multiple things."

Another point to mention in this respect is that Stallergenes' partner Greer has 40% market share in the allergy therapy market, so it might well come out ahead of Merck.

Other risks are very unlikely to depress the stock price as the company has no ongoing legal disputes (it has had only three legal disputes over the past decade, two of which ended with no negative impact on the company) and is covered by adequate insurance policies against all major operational risks.

Outlook and potential catalysts

While the past two pollen seasons have been weak, R&D expenditures and spending for international product tests have been substantial and at the same time saving efforts among public healthcare systems in Europe have put some pressure on Stallergenes' results in recent years, at the very latest the next US pollen season should definitely show strongly increasing tablet sales and further innovations like the house dust mite immunotherapy tablet (currently in phase II/III in Japan) are likely to boost growth even more.

Decreasing earnings are very unlikely, as the immunotherapy market overall is growing at a CAGR of over 6% and recently emerged trends to stronger regulation of allergy therapies will certainly favor the larger players.

Considering that the stock has never traded below 14.5 times forward earnings, not much EPS growth is required to push investors above the €50-59 range, where they have been anchored ever since the failed takeover bid and in this event I expect shares to quickly approach the once usual average PER of 22-23. In this case I expect the stock to trade at €70-80 in about two years.

On the other hand, as Ares Life Sciences has clearly been building the road for successful long-term US operations by acquiring two US companies operating in the allergy therapy sector, the partnership is unlikely to be pleased by keeping only 75% of Stallergenes' profits. Another buyout offer could come at any time, as Ares' owner, Swiss billionaire Bertarelli, certainly has the cash required. Ares had no need to hurry. The partnership knew in advance that the international expansion project would have put a strain on Stallergenes' growth in the next few years to come and that through stock dividends alone its ownership would have increased anyway. Hence the required takeover price would not have increased a lot, while the risks connected to the expansion project would have been at least partly shared with minority shareholders. However, as soon as especially the US expansion will prove to have been successful, Ares will certainly want to own the whole business. And it might well manage to get there without spending a cent of its own money.

In fact, considering that available cash quickly increases on Stallergenes' balance sheet, I believe that within a few years Stallergenes could also try to buy back its own shares at a premium price, indirectly increasing Ares' stake above the 95% level required to delist the company. A rather unusual note to the share repurchase authorization hidden in the lengthy French reference document attached to the above linked 2013 annual report might point to this possibility:

The maximum price of shares to be bought back as part of the new share buyback programme will be € 100 per share, it being specified that this price may be restated in the event of transactions in the share capital of the Company to take account of the impact of these transactions on the share price. The overall maximum amount authorised in carrying out the new share buyback programme is set at € 137,045,700 at 31 December 2013. Stallergenes reserves the right to make full use of the authorised programme.

The stated amount represents 10% of shares outstanding times €100. Thanks to stock dividends received over the past few years, at the end of 2013 Ares already held almost 80% of shares outstanding:

I believe that, as soon as free float will be reduced to 15%, either through smaller buybacks or through dividends taken in cash by minority shareholders and in stock by Ares, Stallergenes will probably offer to buy back its own shares at a premium.

This might also be the reason why the two US companies have been bought directly by Ares itself, without consuming Stallergenes' cash.

As several international value funds have built large positions of Stallergenes' stock, I feel confident that Ares will not be able to squeeze out minority shareholders without offering a fair premium. In this case the stock could go even higher, probably close to €100.

Potential investors should consider that the stock trades very thinly and strictly limit their orders. US investors should also consider the significant foreign currency exposure, due to the fact that at least until now Stallergenes has very little US-$ denominated sales.

Editor's Note: This article discusses one or more securities that do not trade on a major exchange. Please be aware of the risks associated with these stocks.

Additional disclosure: I reserve the right to buy and sell shares at any time at my sole discretion.

No comments:

Post a Comment