june. 10, 2014 4:29 PM ET | 7 comments | About: Sandstorm Gold Ltd. (SAND), Includes: FNV, GDX, PPP, RGLD,

Summary

- Sandstorm Gold has one of the most solid balance sheets in the gold sector, with over $110 million in cash, zero debt and $100 million line of credit available.

- The company is a gold streamer - not a miner. Streaming has several advantages over traditional mining, including fixed cash costs forever and no ongoing CAPEX requirements.

- Sandstorm provides exceptional leverage to the price of gold and lower risk; the company appears to have learned from its mistakes and is poised to outperform.

Sandstorm Gold (SAND) is a small-cap gold company with a pretty unique business model: the company gives capital to miners who are looking to build a mine and in return, Sandstorm receives a gold stream that gives the company the right to buy gold at a fixed price per ounce, for the life of the mine.

This business model has a number of key benefits:

- Gold mining tends to be a very capital intensive business because of the many ongoing capital requirements of operating a mine. For example, exploration to replace lost reserves is just one part of operating a mine, costing millions of dollars each year.

However, Sandstorm only has to make one original upfront payment to a miner to purchase a gold stream, and in most cases does not have to contribute funds for exploration or ongoing CAPEX - yet the company gets all of the exploration and production upside in the projects it invests in.

- Solid exploration results can lead to big production growth, which is where Sandstorm can really add value for shareholders.

- A gold streaming contract works like this: the company buys gold from the miner at a fixed price per ounce, often in the range of $250 - $500 per ounce, but sells the gold at spot price. For example, if a contract calls for ongoing payments of $500 per ounce, Sandstorm will sell gold at spot ($1,250) and pay the company $500, resulting in margins of $750 per ounce. This results in solid free cash flow generation.

- Today, Sandstorm Gold has an impressive portfolio of 37 gold streams and royalties, with 14 of them cash-flowing and the rest in the development or exploration stage. The company has a rock-solid balance sheet, with over $110 million cash in the bank and zero debt.

- Sandstorm Gold estimates gold production of 40,000 - 50,000 in 2014, growing to 60,000 in 2016, all from its current assets with no further capital required to fund this growth.

Here, I will try to make the case that Sandstorm Gold is currently one of the best ways to gain exposure to the gold market - I believe the company is in a great position to outperform going forward.

Gold Streamers Outperform Miners

To prove my point about the gold streaming sector, here is a chart that shows the performance of the three major precious metals streaming companies over the past five years - Royal Gold (RGLD), Franco Nevada (FNV) and Silver Wheaton (SLW) - compared to gold miners (GDX).

You'll see a 100%+ performance from SLW, a 70% rise in FNV and a 50% rise in shares of RGLD, but a negative return in the miners:

(click to enlarge)

Meanwhile, Sandstorm Gold has also crushed gold and silver miners - the company is up 82.81% since February of 2010, compared to negative returns in the GDX and SIL:

(click to enlarge)

I fully believe that this outperformance has to do with the numerous advantages of the gold streaming business model. I only expect this outperformance to continue going forward - as miners have difficulty turning profits, developing properties and reducing ongoing capital costs, streamers will still be profitable and looking to invest.

Why Sandstorm Gold?

There are a few reasons why I consider Sandstorm to have the biggest upside out of the streamers:

Growth upside: With a market cap of just under $600 million, Sandstorm is tiny compared to its peers Silver Wheaton ($7.46 billion), Royal Gold ($4.23 billion), and Franco Nevada ($6.95 billion).

I believe the company has a ton of room for growth. The advantage of being smaller than its peers means that just a $20-$30 million gold stream can result in significant value creation. This is not the case for the larger streamers, where a $30 million deal would barely move the needle.

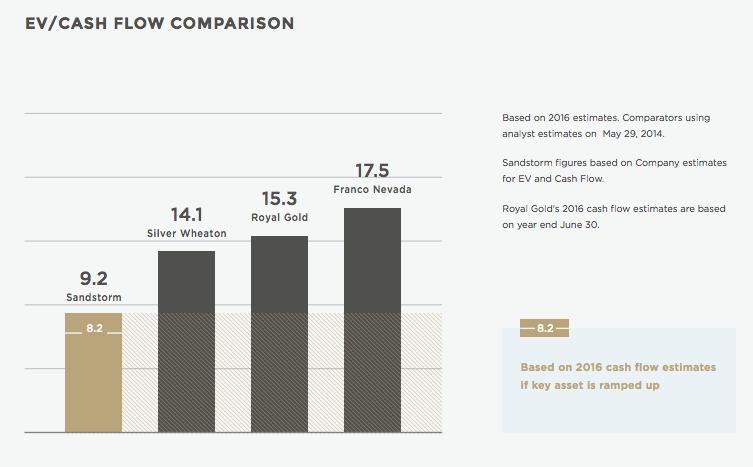

You will also see from this chart below that Sandstorm currently trades at a discount to its peers, trading at 8.2x its 2016 cash flow estimates.

(click to enlarge)

Balance Sheet Strength: With $110 million in cash plus a $100 million line of credit available, Sandstorm is well capitalized to grow its business by buying additional accretive gold streams.

Cash Flow Machine: Sandstorm Gold is profitable, even at $1,200 gold and below. This is due to the nature of gold streams, which allows the company to buy gold at a fixed price per ounce, in addition to the strength of its partners.

For example, for the first quarter of 2014, the company reported operating cash flow of $9.2 million and net income of $3.8 million, even with gold prices under $1,300 for most of the quarter. Most mining companies either did not turn a profit, or turned a small profit.

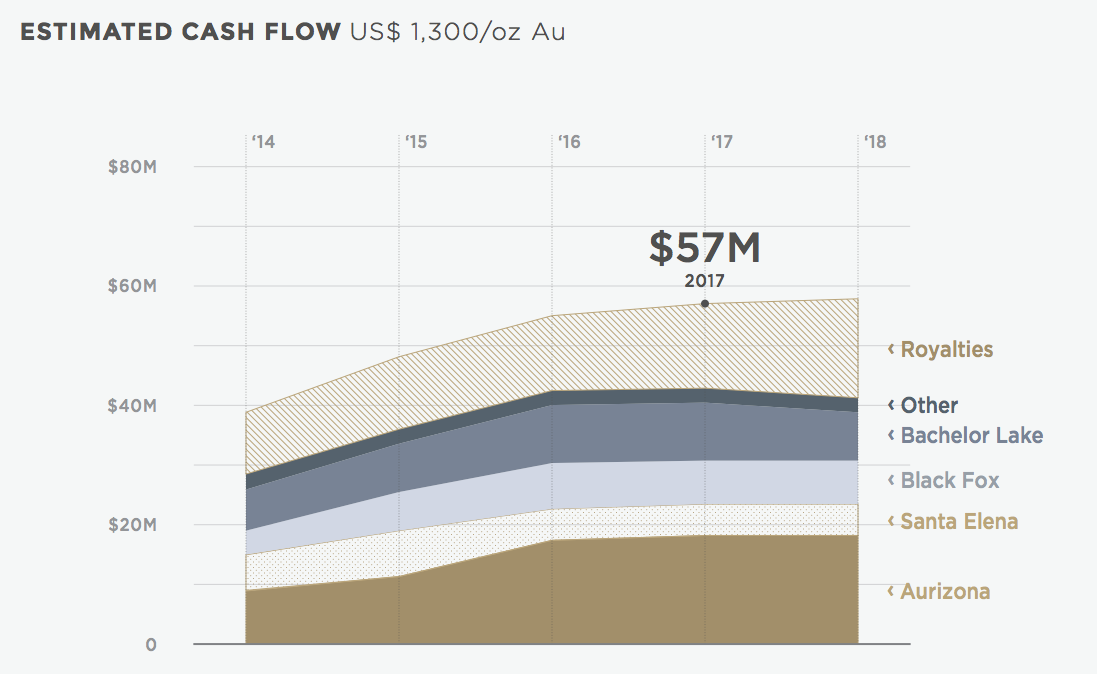

For the full year 2014, the company estimates cash flow of $47 million, increasing to $57 million by the end of 2016 (based on a $1,300 gold price). This is based on Sandstorm's current assets only, and does not include any potential future gold streams or royalties.

(click to enlarge)

Asset diversity: Many junior gold mining companies only have one or two mines. Some only have assets located in one country. If something goes wrong at a mine, those companies could be in serious financial danger. Sandstorm, on the other hand, has a diverse asset base with 14 cash flowing assets located in different political jurisdictions. This is yet another advantage of being a gold streaming company over a miner.

Upside to gold price: Sandstorm's cash costs are fixed, so, if gold were to rise in price significantly to $2,000 or above, their costs would remain the same. This makes Sandstorm a very good hedge against inflation and against the potential of rising costs in gold mining.

Junior miner financing difficulty: I believe there are a ton of opportunities for the company currently, as equity and debt has become increasingly difficult for miners to obtain. The drop in the price of gold has put miners in a very precarious position, but puts Sandstorm is a position to get better terms on its deals. I believe it is only a matter of time before Sandstorm makes their next deal, and they will only focus on top-notch assets.

An In-Depth Look at Sandstorm's Assets

Most of Sandstorm's current assets are focused in very favorable mining jurisdictions: 68% are located in North America, 29% are located in South America and 2% are located in South Africa.

Here are Sandstorm's "core-four" gold streams, which have provided a platform for future growth.

The Aurizona Gold Stream: This stream is a great example of the benefits of gold streaming and the upside potential in Sandstorm. Located in Brazil and operated by Luna Gold, the company purchased the stream for just $22.8 million in 2009, and contributed an additional $10 million to the phase 1 expansion in 2012. Aurizona is targeted to produce 85,000 to 95,000 ounces of gold this year, increasing to 125,000 next year and potentially as much as 200,000 to 300,000 per year thereafter. A phase II preliminary feasibility study is expected in the second half of this year to consider this possibility.

Sandstorm buys 17% of the gold at Aurizona and pays $404 per ounce to Luna. To date, the company has recorded cash flow of $39.8 million from the stream, and the mine has at least 20 years remaining, according to the company.

The great thing about Aurizona is that when Sandstorm bought the stream in 2009, the mine only had a resource base of around 1.3 million ounces of gold - 904,000 ounces measured and indicated and 402,000 inferred. However, due to great exploration results, the company has significantly expanded the resource base today to 4.6 million ounces of gold - 3.63 million measured and indicated (2.35 million in proven and probable categories) and 1.03 million inferred.

The mine is also very profitable for Luna Gold, as the company produced gold at an all-in sustaining cost of just $787 in the first quarter of 2014. This is Sandstorm's best deal to date, and will continue to provide cash flow to the company for years to come.

The Santa Elena Gold Stream: Operated by SilverCrest Mines, this is a gold and silver mine located in Mexico. The mine is high-grade and has an estimated life of mine of 8 years. Sandstorm has an agreement to purchase 20% of the life of mine gold at Santa Elena, paying $350 per ounce. Sandstorm paid $12 million in cash plus 700,000 Sandstorm shares to buy the stream in May 2009.

In February of this year, Sandstorm exercised its underground mine option at Santa Elena, which allows the company to buy 20% of the gold from the underground operation.

Santa Elena produced 31,100 ounces of gold in 2013, netting Sandstorm more than 6,000 ounces. The company anticipates that a new 3,000 tonnes per day mill facility should recover an average annual rate of 32,800 ounces of gold, based on the current gold reserve base of 327,430 ounces.

However, exploration upside still remains at Santa Elena and I feel there is a good chance that the company can extend the life of the mine. Drilling results at the El Cholugo and El Cholugo Dos deposit were very positive, returning results of 13.4 m @ 1.8 grams per tonne gold, and 1.2 m @ 3.9 grams per tonne gold and a bonanza silver grade of 1,239.5 gpt silver.

The Black Fox Gold Stream: The Black Fox mine was originally owned and operated by junior miner Brigus Gold, until the company was bought out by a larger company called Primero Mining (PPP).

Sandstorm has the right to purchase 8% of the life of mine gold at Black Fox and 6.3% of the life of mine gold from the Black Fox extension, at $509 per ounce of gold. Sandstorm paid $32 million for this stream. In 2013, the mine produced 98,710 ounces of gold. The mine has a resource base of 660,000 ounces proven and probable, with 820,000 ounces measured and indicated and 40,000 ounces inferred.

Primero bought Brigus because they believe Black Fox has big exploration upside, which benefits Sandstorm. The company has committed a $48 million budget for 2014 at Black Fox, which will focus on increasing underground throughput and exploration.

The Bachelor Lake Gold Stream: This is one of Sandstorm's most important gold streams in my opinion. The company purchases 20% of the life of mine gold produced at the Bachelor Lake mine in Quebec, at a price per ounce of $500. The company paid $20 million to buy the stream in 2011.

Bachelor Lake has a measured and indicated resource base of 546,507 ounces, with 994,311 ounces in the inferred category. The company is slowly ramping up to full commercial production: the mine produced 12,751 ounces of gold in the fourth quarter of 2014, up from just 4,684 ounces in the previous year. The mine is currently expected to produce around 45,000 ounces of gold annually, ramping up to 60,000 ounces per year.

Bachelor Lake has tremendous upside in my opinion, for a few reasons. First, exploration drilling has seen excellent results, which means there is a good chance to increase the resource base, and convert inferred resources to higher-confidence categories. The company believes there is the potential to add at least 300,000 ounces with further exploration drilling as well.

Placing a Value on Sandstorm

In my opinion, the best way to value Sandstorm is on its cash flow against its enterprise value.

Enterprise Value: With a current share price of $5.20 and 110 million shares outstanding, Sandstorm has a market cap of around $570 million. With $110 million cash in the bank and zero debt, the company has an enterprise value of approximately, $460 million.

EV/Cash Flow: Sandstorm recorded first quarter 2014 cash flow of $9.2 million. If we use the company's full-year cash flow of $47 million, this gives the company a 2014 EV/Cash Flow of 9.8. This is based on $1,300 gold.

*However, if we take the company's 2016 estimates of 60,000 ounces gold production and a $1,300 gold price, the company should record cash flow in the area of $57 million - which gives the company a 2016 EV/Cash flow of just 8. If Sandstorm completes no more deals the company is on track to have an accumulated cash balance of $180 million by 2016 (by the company's estimate) with no debt.

- Keep in mind that Sandstorm currently has $210 million in available capacity (cash and undrawn line of credit) to complete more deals. By the end of 2015, the company estimates that it will have at least $286 million capacity to complete deals, based on the current capacity and accumulated cash flow. I expect Sandstorm to complete at least 1-2 mid-size deals in 2014-15 ($30-$50 million range), in addition to smaller royalty type deals ($5-10 million). If Sandstorm can pull off another deal like Aurizona or Santa Elena, it could mean big gains for shareholders.

Why Sandstorm Will Outperform

It appears that Sandstorm is fairly valued at the present time, based on its current earnings and assets. However, I personally feel that Sandstorm's assets have massive upside potential which the market appears to be ignoring and I think the company deserves a higher valuation. If the company's partners can successfully expand mine operations to their full potential, I think investors will be quite pleased at the results.

Here are my 2017 production estimates for Sandstorm in an upside-case scenario.

Aurizona Mine: The Aurizona mine still holds the greatest potential for Sandstorm shareholders. This is a mine that has the potential to produce 125,000 ounces once the phase 1 expansion is completed this year - that would result in 21,250 ounces of gold attributable to Sandstorm.

However, what some people are forgetting is that Luna Gold is also evaluating a phase II expansion plan at Aurizona, which will "evaluate a range of process plant, mining fleet and infrastructure scenarios to deliver a life of mine average annual gold production of 200,000 to 300,000."

Here's a few reasons why I think the expansion will be successful. First, Luna Gold is a profitable company, with all-in sustaining costs under $800 an ounce and $31 million cash in the bank. Next, Aurizona has a resource base of more than 4.6 million ounces of gold (measured, indicated and inferred), but is currently producing less than 100,000 ounces a year. The phase I expansion is being constructed to handle additional capacity, and with a resource base that large, I feel there is a good chance Luna Gold can handle at least 200,000 ounces production per year and still have a mine life of at least 15+ years.

At the low end of the range, if Luna can produce 200,000 ounces a year that would mean 17% to Sandstorm or 34,000, which is more than half its total current production.

At the higher end of the range, it would mean 300,000 ounces of production, or a whopping 51,000 ounces to Sandstorm - which is more than its total current production.

Black Fox Mine: When the Black Fox mine was in the hands of Brigus Gold, it was a very underexplored, underdeveloped property since Brigus was a small cap miner with balance sheet difficulties. Now that Primero Mining, a much larger company, has taken over, Primero is investing the money needed to realize Black Fox's full potential. Black Fox will only produce 80,000 ounces in 2014, but Primero expects 110,000 ounces of production at the mine annually, which would mean 8,800 ounces to Sandstorm.

Past drill results at Black Fox that are not included in the current resource include 11.3 metres of 12.9 g/t gold, 5.4 metres of 3.4 g/t gold and 3.3 metres of 15 g/t gold. The deposit remains open for expansion laterally and at depth.

Based on these excellent drill results I expect the company to announce an expansion of the resource base. I am looking forward to seeing Primero unlock Black Fox's true value.

Bachelor Lake Mine: Sandstorm is only estimating around 50,000 ounces annual production from the Bachelor Lake mine. In June of 2014, Metanor announcedthat Bachelor Lake produced 5,202 ounces in May - on an annual basis, that's more than 62,000 ounces of production. If Metanor can produce 62,000 ounces annually, this would mean 12,000+ ounces to Sandstorm.

There have also been a number of very impressive drill results from Metanor which are not included in the current resource base. The company is actively drilling at Bachelor Lake, with the goal of defining new resources to increase the resource base and production. Take this release on May 31, 2014 for example, when Metanor intersected 9.5 g/t gold over 10.1 metres. Other results included 16.4 g/t gold over 1.4 metres and 16.3 g/t gold over 4 metres. Perhaps the most impressive result came on February 6, 2014, when the company announced a drill intersection of 10.4 g/t gold over 17 metres.

Bachelor Lake is exactly the type of property that Sandstorm wants to invest in - a high-grade gold mine with huge exploration and production upside. Even though the mine is currently producing 60,000 ounces on an annual basis, I believe there is potential for even higher production. It's hard to tell at this point just how much upside production potential there is, but I wouldn't be surprised to see Bachelor Lake turn into a 100,000 ounce a year mine one day.

Remember, Sandstorm management is only forecasting 60,000 ounces for 2016 and only slightly higher in 2017. Here's the upside case scenario for Sandstorm for 2017/18.

| Mine | Ounces |

| Aurizona | 34,000 |

| Black Fox | 8,800 |

| Bachelor Lake | 12,000 |

| Santa Elena | 6,000 |

Total Ounces: 60,800

You will see that these four streams alone can possibly account for the entire production guidance given by Sandstorm by 2017.

If we take Sandstorm's other assets, it would include roughly 10,000 - 12,000 ounces from royalties, as well as 2,000 - 3,000 ounces from other assets such as the Ming stream and the Bracemac-McLeod royalty.

Total Ounces: 72,800

This would represent an impressive production growth of 60% from 2014's estimate of 40,000 - 50,000, higher than the company's estimates.

I am bullish on gold so I expect the price to be much higher than $1,250 an ounce by 2017. However, if we use a gold price of $1,300 an ounce, and cash operating costs of $350 an ounce for Sandstorm ($355 in the last quarter and lower in previous quarters).

*Production of 72,000 ounces at $1,300 an ounce would equal $93.6 million revenue.

*Margins would be $950 an ounce ($1,300 minus $350 costs).

*Operating cash flow would be $68.4 million.

The market is currently valuing Sandstorm with an EV/Cash Flow of 10. If we placed the same value based on these upside-case estimates, Sandstorm would have an enterprise value of at least $680 million.

It's hard to say what the balance sheet will look like in 3-4 years, but if Sandstorm has $100 million cash in the bank at that time and no debt, the company would have a market cap of $780+ million, representing 50%+ upside.

Where Will the Growth Come From?

Keep in mind that this assumes Sandstorm completes no more deals between now and then. It is highly likely that Sandstorm completes more gold streams in the future to increase its production.

I believe there are more than a few opportunities for the company at the current time - in particular, there are a number of high-grade gold development projects in the mining-friendly country of Burkina Faso, Africa, projects that I hold in high regard. Other opportunities still exist in the mining-friendly countries Canada, Mexico, the United States, and even some opportunities in Europe. I'd rather not speculate on individual projects or companies in this article, but I'm more than willing to discuss my thoughts in private.

Investors also need to remember that Sandstorm has a number of organic growth opportunities outside of its major streams. I am referring to the Mt. Hamilton and the Coringa royalty.

Sandstorm purchased a 2.4% royalty on Mt. Hamilton for $10 million in June of 2012. The project is located in Nevada and is operated by Solitario Corp. Once in operation, the mine is expected to produce 48,000 ounces of gold a year and 330,000 ounces of silver for 8 years, with very good potential to add additional ounces to extend the mine life.

The agreement has an option for Solitario to convert the royalty to a gold stream:"If MH-LLC enters into a gold stream agreement with Sandstorm that has an upfront deposit of no less than US$30 million, MH-LLC will have the option, for a period of 30 months, to repurchase up to 100% of the NSR for US$12 million. In addition, MH-LLC has provided Sandstorm with a right of first refusal on any future royalty or gold stream financing for the Mt. Hamilton project."

I can see Sandstorm purchasing a gold stream of 10-20% from Mt. Hamilton at $350 - $500 per ounce. If that happens, Sandstorm would net another 8,000 to 10,000 ounces of gold per year.

As for the Coringa royalty located in Brazil, the company owns a 2.5% NSR on the project and has a right of first refusal on any gold stream.

Coringa is operated by Magellan Minerals and contains more than 1 million ounces of high-grade gold (measured, indicated and inferred). A 2012 preliminary economic assessment (PEA) gave the Coringa project a net present value of $110 million at $1,350 gold. The mine would produce 51,000 ounces of gold annually with a life of mine of 8.5 years, and Magellan would need $64.5 million initial CAPEX to bring the mine to production.

I can see Sandstorm converting its royalty to a gold stream of 10% of the life of mine production at a per ounce cost of $350 - $500. If this is the case, Sandstorm would realize at least 4,800 ounces of production a year.

The risk with this project, however, is the fact that the market has not been very kind to Magellan: the company has a current share price of just $.12 and a market cap of $15.47 million. Therefore, it might be hard for Magellan to come up with additional funding to advance the project to production, unless the gold equity markets rebound.

Still, Sandstorm has a number of organic and non-organic growth opportunities, and I can't wait to see the company's next move.

Sandstorm Metals Transaction is Positive for Shareholders

In 2009, Sandstorm Gold was founded alongside its sister company, Sandstorm Metals & Energy, with management holding the same roles at both companies.

Unfortunately, Sandstorm Metals & Energy did not have anywhere near the same amount of success as Sandstorm Gold, with many past deals going bust and little opportunities available for near-term growth. Sandstorm Metals was simply not worth management's time and focus.

*On April 14, 2014, Sandstorm Gold announced that it would be acquiring Metals & Energy and on May 29, 2014, the deal closed. This is a move which I feel is very beneficial for Sandstorm Gold shareholders for a number of reasons. The deal was valued at approximately $49 million, but I feel it was worth more for Sandstorm.

- Sandstorm gained $4.5 million in cash, plus a 3% royalty on the Bracemac-McLeod mine, with estimated annual cash flow of $5 million per year.

- The company also received advanced exploration and development assets, including royalties on Canadian Zinc's Prairie Creek Mine, and Entree Gold's Hugo North Extension and Heruga deposits.

- Sandstorm benefits from the use of Sandstorm Metals' non-capital loss carry forwards, for tax purposes. The company will have an estimated $7 million to apply against future taxable income.

- The company also expects to realize proceeds from the sale of non-core assets, including various coal, oil and natural gas assets. It is early to say how much money the company can gain from the sale of these assets, but it could be substantial.

- Perhaps most importantly, the company will now get to focus 100% of its attention on Sandstorm Gold. With Sandstorm Metals & Energy in the rear view mirror, I think management is more likely now to create value for shareholders, spending more time analyzing projects and acquiring accretive gold streams.

Highly Leveraged to Gold

Remember, due to the nature of its business model, Sandstorm is very highlyleveraged to a rise in the price of gold. This estimate assumes what I feel is a conservative gold price. If we use a gold price of $1,500 an ounce - just $200 an ounce higher - things can get pretty interesting. Here's some estimates at various gold prices and production levels:

Ounces/Gold

|

$1,200

|

$1,400

|

$1,800

|

40,000

|

$33.8

|

$41.8

|

$57.8

|

50,000

|

$42.7

|

$52.2

|

$72.2

|

60,000

|

$50.7

|

$62.7

|

$86.7

|

*Production of 72,000 ounces at $1,500 gold equals $108 million revenue.

*Margins would be $1,150 an ounce.

*Operating cash flow would equal $82.8 million.

If you take an ultra-bullish scenario of $1,800 an ounce gold, the company would have margins of $1,450, revenue of $130 million, and cash flow of $104 million.

As the price of gold goes higher, Sandstorm makes even more money - fixed cash costs means the company has no exposure to a potential rise in costs of mining production. This makes the company a really great hedge against inflation in my view.

What Are The Risks?

I believe that Sandstorm Gold is one of the lower-risk gold investments out there, but that doesn't mean this is a risk-free investment by any means. Here are a few potential risks:

No control over mining activities: Unfortunately, not even gold stream has worked out for Sandstorm. The company has no control over mining, development or exploration activities, so they are exposed to the potential failure or problems of their partners.

The company purchased a gold and platinum stream on the Serra Pelada mine in Brazil, for $75 million in 2012. Colossus Minerals faced several challenges getting the mine into production, with the company facing cost overruns and ultimately needing an additional $70 million to get the mine to production.

The company failed to raise the money required and filed for bankruptcy in January of 2014, with Sandstorm writing off the assets from its books completely and converting its gold and platinum stream into a 2% royalty. Colossus then announced a restructuring of ownership - on April 30, 2014, the company announced that a court has approved the restructuring, with Sandstorm owning 40.2% of the new company and 51.2% owned by holders of the previous gold-linked notes.

For Serra Pelada to get to production, a new investor(s) is required for additional funding, and that $70 million figure is likely higher by now. As of right now, it is uncertain just how much money Sandstorm will recoup from this deal. This deal is a reminder that not every gold stream works out, and Sandstorm needs to be careful choosing their projects and partners going forward.

Price of gold: The biggest risk to Sandstorm is a drop in the price of gold, as this obviously affects the company's profitability. If the gold price were to drop low enough, it could present problems to Sandstorm's partners, resulting in a mine shutdown or a company bankruptcy.

However, given the nature of the streaming mode, Sandstorm is profitable even at much lower gold prices. The company has also wisely bought gold streams on mines that have low all-in sustaining costs to protect against further downside.

The Bottom Line

Sandstorm is an exciting small-cap gold streamer with solid growth prospects. The gold streaming model has numerous advantages over traditional miners and makes for a far safer investment in my opinion. With $200+ million in available capacity, Sandstorm is on the prowl for its next deal - if management can deliver and the gold price can hold here or go higher, I believe shareholders are in for a nice surprise.

Disclosure: The author is long SAND.

This comment has been removed by the author.

ReplyDeleteThanx..

ReplyDeleteThis blog post very nice .I hope next update blog with immage.

http://sellgoldquebec.wordpress.com/