Summary

- Micron is an innovation leader in the industry trading at less than 10x earnings.

- Improved pricing environment should provide tailwinds for Micron's share price.

- Both the fundamental- and the technical picture support an investment in Micron.

Mobile demand is skyrocketing (which is not a surprise if you look at the DRAM bit content from the new devices announced at Mobile World Congress a week ago), among other things, and supply of some segments will fall short of demand which will lead to pockets of high prices as the market will not be perfectly efficient. Long contract times are also a sign of increasing concern by manufacturers, and will occasionally lead to massive pre-payments to secure supply. Also, if you look at the typical contract times and use the information that contract prices have been steady, you can conclude that the average price has greatly increased as old contracts come up for renewal. Due to these factors, most sell-side analysts have significantly underestimated the earnings ability of Micron, both this quarter and in the longer term.With an improving price environment supporting Micron's share price and Micron's Elpida transaction potentially being the source of positive earnings surprises, the company has more room to grow its equity valuation. The chipmaker currently fetches only a forward P/E ratio of 9.76 -- despite a one-year return of 177% -- highlighting how severely undervalued Micron has been and still is.

What I also always liked about Micron was its leadership in innovation. Similar to Alcatel-Lucent (ALU), the market just discounted the company's market-leading position in coming up with new technologies and processes and setting new industry standards. This oftentimes leads to severe mispricings -- both in the case of Micron and Alcatel-Lucent (I mention Alcatel-Lucent because it was a similarly neglected and misunderstood company that faced short-term obstacles and negative investor sentiment). Micron is a top notch innovation leader which I also pointed out previously. I wrote:

Micron commits substantial resources to come up with cutting edge technology. One area where Micron excels is process technology: The development of the 16nm NAND technology sets industry standards in terms of storage capabilities. Micron also remains an innovative industry leader in Phase Change Memory [PCM] and I/O virtualization. Technological cooperation with Intel has led to significant first mover advantages in server and SSD applications of NAND technology. Micron also gained outside recognition for innovative capabilities being featured on Thompson/Reuters list of 2012 Top 100 Global Innovators. Innovative capabilities represent competitive advantages which come in form of higher-efficiency products. Micron's innovation track record raises confidence in Micron's future product pipeline.From a fundamental point of view, Micron still makes an attractive value proposition: Pricing tailwinds, a savvy Elpida transaction that could lead to EPS surprises in the coming quarters and an industry leadership position in terms of innovation reflect the upside potential that Micron still retains. And best of it all: The company can be bought for less than ten times earnings.

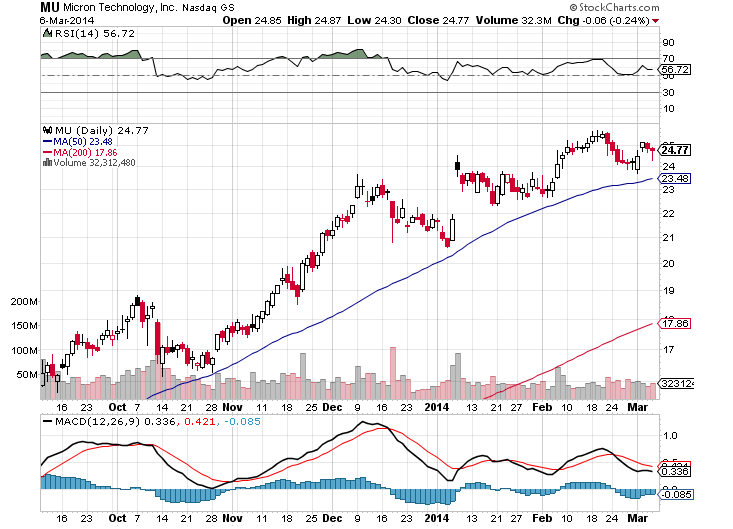

Technical picture

From a technical standpoint, Micron is not even overbought at the moment and holds up nicely at the $24 level. The Relative Strength Index also doesn't suggest that Micron is a candidate for a pullback any time soon. Micron's short-term upward trend is intact and I have a near-term price target of $30 on the stock.(Source: StockCharts.com)

Conclusion

Both from a fundamental perspective as well as a technical one, Micron still has potential to add to last year's share gains. Despite a 177% increase in share value, Micron still trades at less than ten times forward earnings -- even though the company has created a substantial catalyst for itself (Elpida acquisition) and is a recognized innovation leader. Pricing effects and a cyclical demand situation also add to the appeal of the chipmaker. The technical picture indicates that Micron's upward trend canal is intact. Further momentum and good news from Micron could quickly propel shares to $30.Source:http://seekingalpha.com/article/2076313-micron-technology-not-too-long-until-we-see-30

No comments:

Post a Comment