Editor's notes: FCU.V could be in line for a takeover based on its unique portfolio of projects. Impressive early results and ready low-cost access to infrastructure should lead to a premium valuation.

This article was first released only to PRO subscribers. Learn More

This article was first released only to PRO subscribers. Learn More

(Editors' Note: Fission Uranium trades under the symbol FCU.V on the TSXV with average daily volume of ~$1.4 million CAD)

Company Overview

Following the completion of the Alpha arrangement, Fission is the 100% owner of the PLS project, its sole asset. Fission now has ~313,000,000 shares outstanding, as well as warrants and options representing approximately 43,000,000 shares bring the fully diluted total to ~356,000,000. At the current price of $1.06, the market is valuing Fission at under $377 million (USD). With the exercise of all in-the-money warrants and options, the company will have upwards of $50 million in cash less the costs of the winter drill program (it currently has ~$25 million). This is more than sufficient to advance the project through the upcoming winter and summer drill programs and attain an NI 43-101-compliant resource with cash leftover. The recently-commenced winter drill program is more than double the size of 2013's winter and summer programs. Fission will drill at least 30,000 meters (90 holes) for resource development and an additional 14 holes to explore other high-priority targets determined using radon anomalies and other conductors on the property, a strategy used with much success to date. Despite the large scale of this drill program, it will cost only about $12 million thanks to the favorable shallow nature of the deposit.

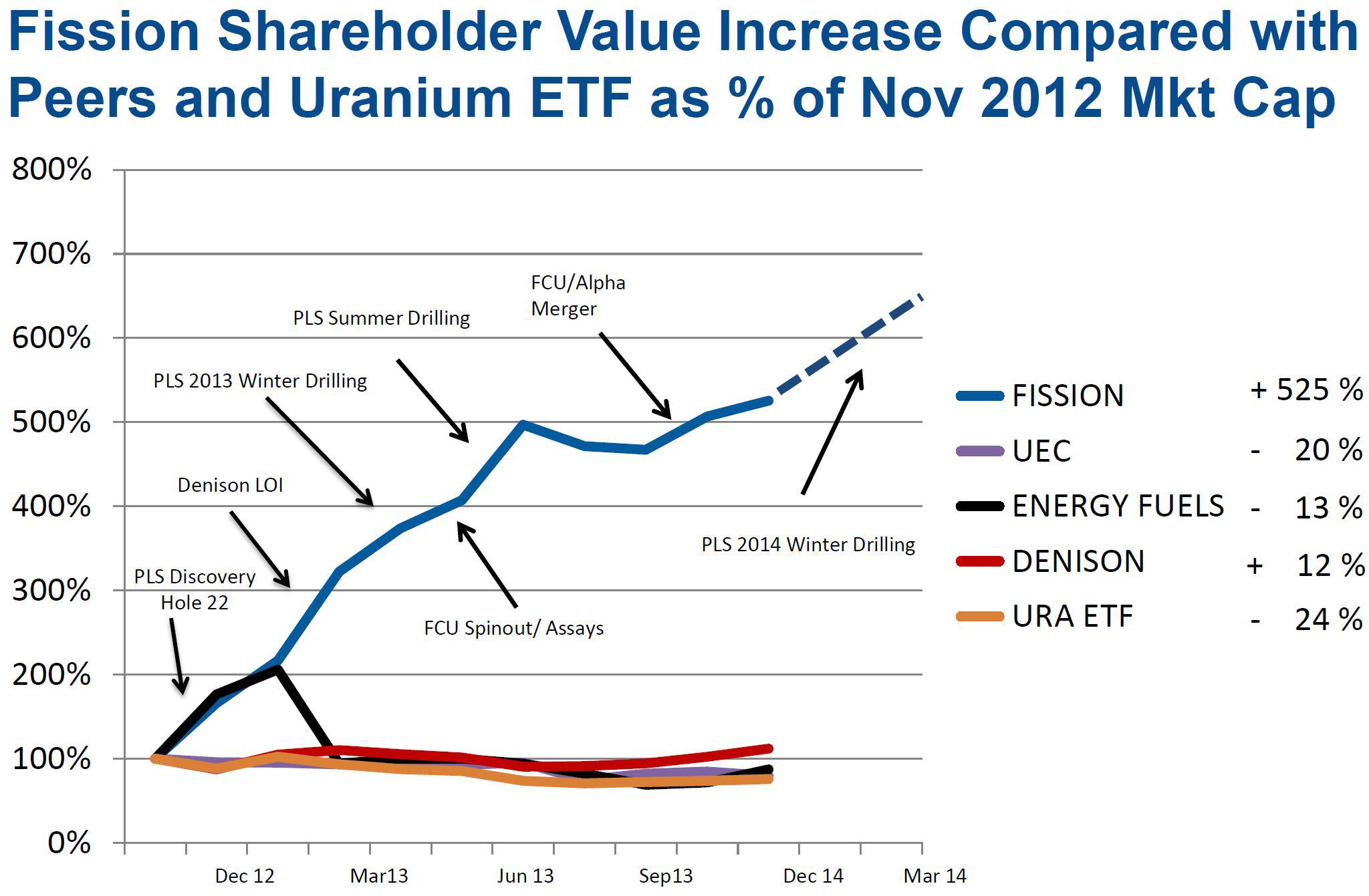

Fission has a top-quality management team with a proven track record of making, advancing and monetizing discoveries. Already in 2013, Fission Energy (the pre-spinout company) sold its Waterbury Lake discovery to Denison Mines Ltd. (DNN) and spun out PLS and its other properties, which now make up Fission Uranium and another new spinco (due to the Alpha Minerals takeover), Fission 3.0 (OTC:FISOF). Shareholders have already seen triple-digit returns this past year in the face of a weak market for junior resource companies and a low and falling uranium price.

(click to enlarge)

This is a testament to management's performance and consistency in producing value through the drill. On the ground, led by President and COO Ross McElroy, P. Geol., Fission has done an impressive job targeting its drill programs. Using radon surveys in combination with traditional techniques, it has struck mineralization in over 80% of holes to date, including 12/12 holes to start the winter program. Another radon survey is planned for this winter, which will extend coverage and provide more drill targets for potential expansion outside of the current strike. Management has also stated, and demonstrated through past transactions, a willingness to sell at any time as long as any deal is in the best interests of shareholders.

Brief Uranium Bull Case

While very relevant to the article, I will not go into detail on this topic here as it deserves its own treatment. There are several quality articles that lay out the bull case for uranium, and I recommend researching this before investing in any uranium stock. Here are 4 of the most important factors that have lead to my bullish outlook for uranium:

- The US-Russian HEU agreement (the "Megatons to Megawatts" program) which has supplied 15% of the world's uranium by down-blending highly-enriched Russian warhead uranium ended in December 2013.

- Japan, under pro-nuclear Prime Minister Shinzō Abe, will most likely restart as many as 16 reactors this year, providing more clarity as to future demand. Also, the LDP (Abe's party)-supported pro-nuclear candidate, Yoichi Masuzoe recently won the Feb. 9 Tokyo gubernatorial election against anti-nuclear former Prime Minister Morihiro Hosokawa.

- Under current projections from organizations, including the World Nuclear Association, there will be a long-term structural supply deficit due to new plants coming online and insufficient mine development to meet this demand.

- There are currently 435 reactors operable in the world. There are 71 plants under construction, 172 planned to begin construction in the next 10 years, and an additional 312 plants proposed to be built by 2030. This will not only replace the closure of aging reactors but will also represent significant growth, and these numbers have been continuously rising.

- The uranium spot price is now below the marginal cost of production for many producers, a situation that is unsustainable.

Project Characteristics and Results

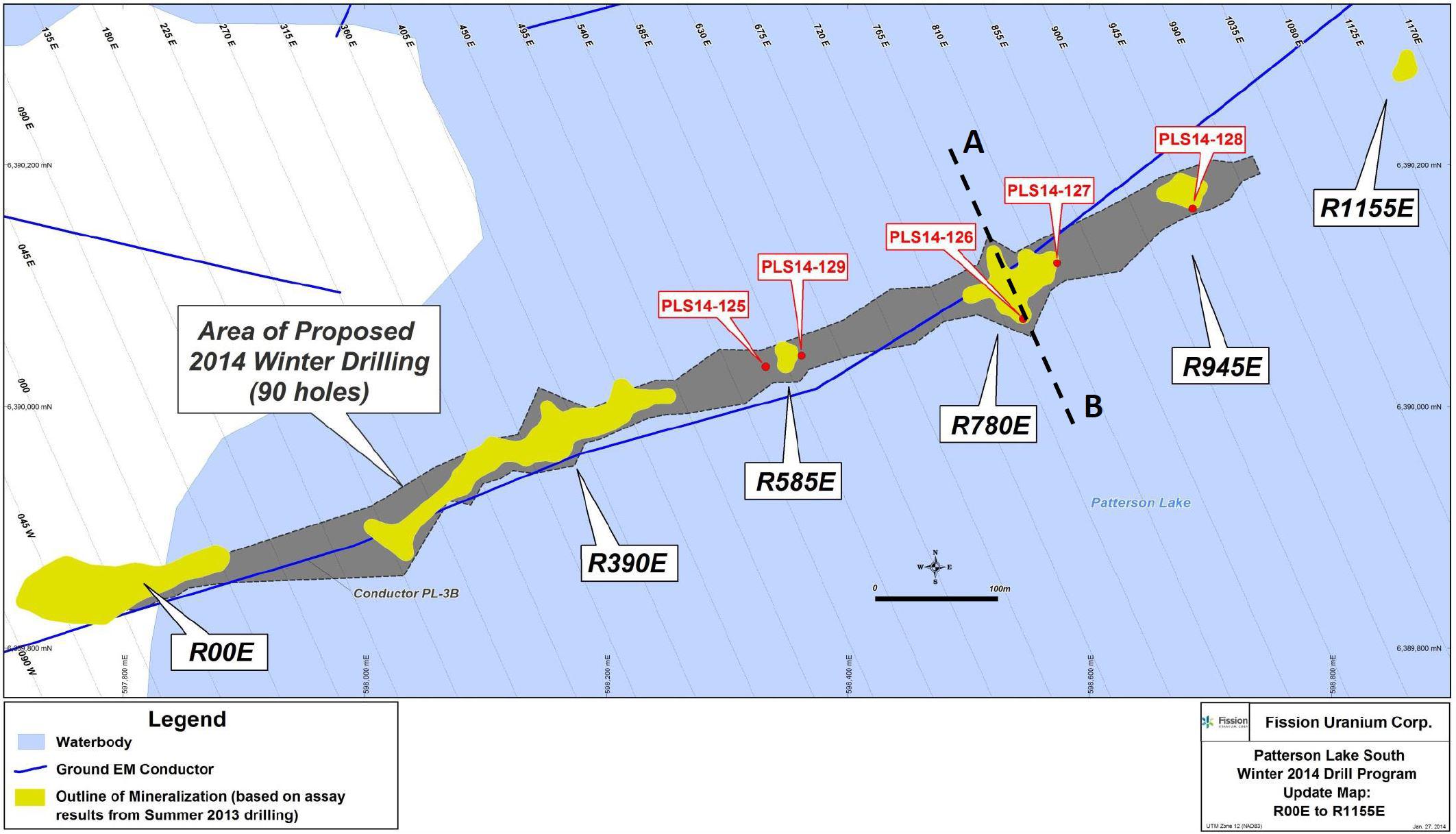

At the commencement of the winter drill program, the project consisted of 6 mineralized zones and remains open in all directions.

(click to enlarge)

All figures taken from investor presentations here.

The focus of the winter 2014 program is to fill in the gaps between zones in order to prove that this is one large connected deposit. Uranium in the basin pinches and swells and deposits tend to be narrow and irregular in shape, so it will take a lot more drilling before the resource is fully defined. Here are some of the characteristics and results that make this project extraordinary:

- The summer program extended the strike of the six open-ended mineralized zones to a length of 1.76 kilometers. For a bit of perspective, consider that Hathor Exploration's Roughrider deposit was under 400 meters.

- Mineralization commences at a depth of 50 meters below the surface. The graphic below demonstrates just how impressive this is when compared to other unmined deposits.(click to enlarge)

- The deposit appears to be open-pittable, and as such costs are likely to be as low as $15 per pound with favorable geology.

- Highlights from the summer program include:

PLS13-072: 34.5m @ 8.15% U3O8, including 7.5m @ 19.28%PLS13-075: 54.5m @ 9.08% U3O8, including 21.5m @ 21.76%PLS13-080: 43.0m @ 6.93% U3O8, including 14.0m @ 15.63%PLS13-096: 85.5m @ 6.93% U3O8, including 5.50m @ 18.20%

The assays above represent highlights of results that continue to be up there with the best in the history of the Athabasca basin (aside from maybe McArthur River, which is in a class of its own). Using a cut-off grade of 0.1% U308, including all 93 mineralized assays released to date (15 unmineralized holes and 17 pre-discovery holes have been excluded), an average ore density of 2.66 g/cm3, and using a 7.5 meter radius of influence, my rudimentary model already puts the project at 44 million lbs with an average grade of 2.79%.

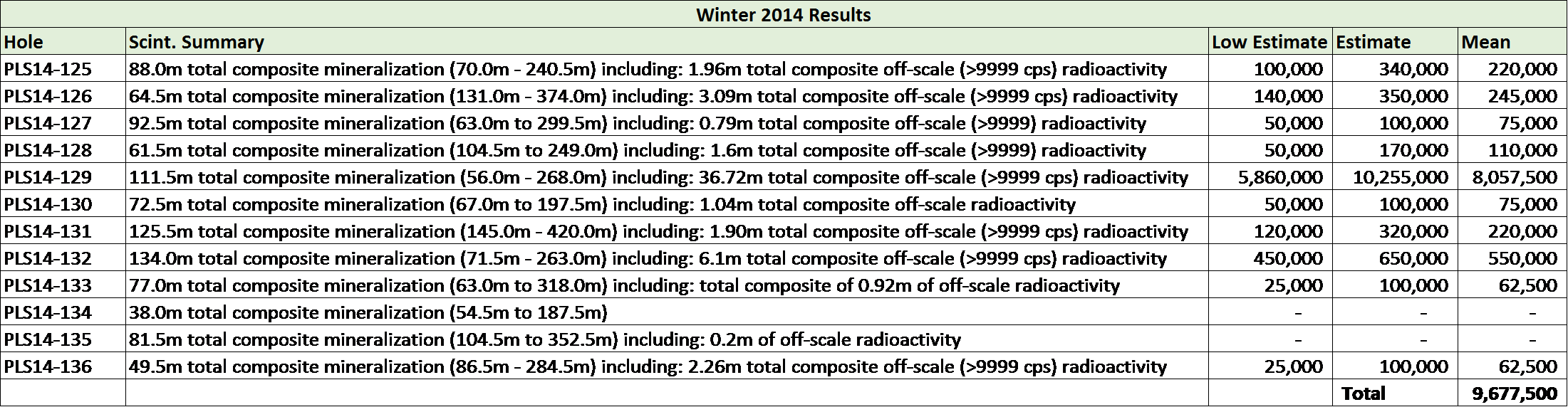

Fission has now also released the first 12 assays of the winter 2014 program. All 12 holes struck mineralization, including PLS14-129 on line 600E. As per Fission's news release on January 27, 2013, the hole intersected 36.72 meters of total composite off-scale mineralization. This far exceeds hole PLS13-075 (previously the best hole), which intersected 21.65 meters total composite off-scale and assayed 21.76% U3O8 over 21.5 meters in 9.08% over 54.5 meters. This means PLS14-129 has a whopping 70% wider off-scale mineralization than any hole to date. My model has PLS13-075 contributing ~5.9 million lbs, which shows how significant big holes like this are. As assay results have been consistently correlated to initial scintillometer results, I also have produced a very rough estimate for the first results of 2014. In order to do so, I looked at the overall correlation between scintillometer and assay results from the project, placing particular emphasis on local results from each of the zones. For example, of particular note is PLS13-098, which is adjacent to PLS14-129. The scintillometer showed 76 meters total composite mineralization, including 7.62m total composite off-scale radioactivity, and assayed 16.5m of 8.47% U3O8, including 60.3% over 0.5m, the highest individual assay value on the property to date. This is certainly a good sign that PLS14-129 will not disappoint, and as the nearest hole, its scint./assay result correlation was considered more relevant.

With this in mind, I will limit further discussion of these very preliminary projections to the fact that I have used what I believe to be conservative metrics to come up with a low and "most likely" estimate, and then used their average to calculate a resource.

(click to enlarge)

Also of note for PLS14-129 is that it appears to have been drilled outside of a radon anomaly, which so far has been used very effectively to target holes, demonstrating that high-grade mineralization is by no means limited to these anomalies.

If these projections are accurate, it would bring the project to just under 54 million lbs, pushing it over what many consider to be an important milestone at 50 million lbs.

While this already represents an impressive resource that would likely be developed, this remains in its early stages and the deposit is open in all directions. Filling the gaps between zones will greatly expand the resource, and with at least 78 holes left for this purpose during the winter program, the pounds should add up fast. With numerous other highly prospective conductors and anomalies on the property remaining to be tested as well, this project continues to have the potential to be up there with some of the best in the history of the Athabasca basin.

Why is the market missing this?

- The uranium spot price remains extremely depressed and is hovering around the $36 mark.

- Negativity and fear continue to drag on nuclear energy-related stocks following the Fukushima disaster in 2011.

- Growth in the industry will be dominated by developing nations outside of North America, so U.S. investors remain hesitant.

- Overall, it has been a negative environment for commodities and junior resource stocks in particular.

- Although increasing, there is still a lack of attention on the project and analysts have been slow to update reports and estimates.

- Many institutional investors will not, or are unable to, invest in a small cap junior explorer, particularly one without an NI 43-101-compliant resource.

Catalysts

Fission has a busy year ahead of it, with several catalysts that should drive the stock higher. The company is just 12 holes into its massive 100+ hole winter program. This program will continue to expand the 6 zones of high-grade mineralization, and it also appears more and more likely that it will show that these zones are connected. On top of this, any success testing the numerous other high-priority targets on the property (14 holes planned this winter) could take this project to another level. The news flow should be steady over the next several months, with initial scintillometer results followed by assays. This will be followed up with a similarly large summer drill program and a NI 43-101-compliant resource before the end of the year.

If you look at the three near-surface projects in the basin that were open-pittable (Cluff Lake, Key Lake, and McClean Lake), they have all been mined out. This is not surprising due to the significantly lower costs involved. The majors will likely be particularly cost-conscious in the current low-price environment. This is why the PLS discovery is so unique and should receive a premium valuation. This project is not just a top-quality high-grade deposit, it appears to be the ONLY near-surface, high-grade, open-pittable known uranium resource in the world. This is what makes Fission probably the best takeover target in the uranium space. While often the majors would wait for an NI 43-101-compliant resource, this may not necessarily be the case with such a unique project. Having the project now consolidated into a single entity has removed the largest barrier to a takeover. There are numerous potential candidates, in particular Cameco (CCJ), Rio Tinto (RIO), Areva (OTCPK:ARVCF), and several Asian utilities. Cameco would make the most sense due to its dominant position in the Athabasca basin as well as an explicit commitment to focus on its core operations there. Although they backtracked slightly in the most recent conference call, management has stated that they are actively looking for acquisitions and they have been beefing up the balance sheet for a while now, including a recent $450 million sale of the company's stake in Bruce Power. While Cameco already had plenty of liquidity to fund growth before the sale, according to CEO Tim Gitzel, it plans to "reinvest in our core uranium business where we see strong potential for growth." On the other hand is French nuclear giant Areva, which continues to face operational challenges at mines in Africa. Areva is already active in the basin, and with the recent Canada-EU trade agreement that will allow European companies to control majority stakes in Canadian uranium mines, this would also be a good fit as it looks to focus on safer jurisdictions. This agreement could also increase the likelihood of Rio making further moves in the basin, following up the $650 million acquisition of Hathor Exploration in 2011. Rio also appears to have synergies with Denison Mines (another likely takeover target), which would give it partial ownership of the McClean Lake mill as well as the impressive portfolio of properties and projects in the basin that the company has assembled.

Fission is not in the business of developing mines and CEO Dev Randhawa has consistently stated his intentions are to sell the asset. Thus, the question of upside potential is mostly dependent on when and at what price a takeover will occur. At this point, putting a timeframe on it is little more than speculation. However, with the project now under one roof it could happen at any time, and if drilling success continues on its current trajectory, potential acquirers will only pay more the longer they wait. If there are no attempts during or following the winter drill program, I believe that the initial NI 43-101-compliant resource, expected by the end of the year, is likely to act as the catalyst for an acquisition. Putting a price target on a potential transaction is nearly as challenging. Looking at past deals should give a decent indication of where this is likely to be valued depending on how much the resource grows. The most recent comparable transactions in the basin were for the Millennium deposit at $8/lb, Waterbury Lake $8/lb, and Hathor Exploration's Roughrider deposit at $11 per pound. When comparing these deposits, it must be considered that at the time of these transactions, the long-term uranium price was over $60. Since then, it has steadily fallen to its current price closer to $50 due to a supply glut and hesitant utilities following the Fukushima accident. Hathor, the most comparable of the recent takeovers to Fission, had 58 million lbs at very high grades. Rio Tinto outbid Cameco in an extraordinary bidding war that saw the deposit sell for $650 million. To come up with a takeover price target for Fission, I have used $8 per/lb as a basement value based on the Millennium and Waterbury transactions. While these transactions occurred in a slightly higher uranium price environment, this is more than outweighed by the much larger scale of the PLS project, its shallow depth (mineralization starts at 60m vs 200m), and likely open-pittable nature. The best-case scenario of $12/lb sees this playing out similar to Hathor, while also being given a premium due to PLS being larger and shallower with an improving uranium outlook. The midpoint of these targets gives me a $10/lb takeover price estimate. This would put PLS at a small discount to Hathor but at a premium to the other recent transactions in the basin, which is very reasonable given this can likely be mined as a pit.

(click to enlarge)

Looking at these scenarios, it is obvious that the market continues to ascribe little value to the exploration potential of the project. To come up with a one-year price target for a scenario that involves no takeover, I used $7.50 per pound (in line with current peer valuations) and a 75 million pound resource, which is now a near-certainty even with just moderately successful winter and summer drill programs. This produces a target of $1.58 per share, almost 50% above Tuesday's close. My upside scenario sees Fission being bought at $10/lb with an 85 million pound resource. This would value Fission at $2.38, representing 125% upside. Although these are already outstanding numbers, they represent reasonable outcomes and do not come close to representing the full upside potential of the project if exploration continues to go very well.

Risks

Like most junior resource stocks, this should be considered a high-risk, speculative investment. There is a lot of drilling left to do before the deposit is defined, and the market is likely to discount results until there is an NI 43-101-compliant resource. Uranium stocks will depend on continued economic growth, particularly in emerging markets, where the majority of new nuclear power plants will be built. Finally, there is always a small chance of another nuclear accident, which would be devastating to the nuclear industry and uranium stocks.

Conclusion

I believe that due to the unique nature of the PLS project, Fission will eventually be bought out, more likely sooner than later. The share price continues to lag the impressive results while at the same time assigns no value to exploration potential, creating a favorable risk-reward scenario. A shallow, high-grade deposit in one of the most mining-friendly areas in the world with access to infrastructure already at its doorstep certainly deserves a premium valuation. Averaging my one-year non-buyout and buyout scenario targets, to which I have assigned equal probabilities, gives me a one-year target of $1.98, 87% above Tuesday's closing price of $1.06.

By Western Investor

Source:http://seekingalpha.com/article/2014421-fission-uranium-still-undervalued-with-50-percentminus-125-percent-upside

Your blog has wonderful information regarding Guidewire Services, I also have some valuable information regarding the Guidewire Testing in USA, Canada hopefully, this will be very helpful for you.

ReplyDelete