Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Oh, yeah, there was probably also a small mention of Buffett's $5 billion stake in the company, which has since doubled. I wonder who paid the lunch bill.

CNBC.com reported:

Shares of Bank of America have risen more than 100 percent since Buffett took a similar stake in Bank of America in August 2011-leading Buffett to thank Moynihan for what is now a $5.27 billion paper profit for Berkshire Hathaway in just two years, these people said. A spokesman for Bank of America declined to comment.Berkshire gets a dividend of 6 percent, or $300 million a year, for the money it, in effect, loaned to BofA through the purchase of preferred shares. Even more lucrative for Berkshire, though, are warrants it received as part of the deal that allow it to purchase $5 billion worth of BofA common stock at $7.14 per share.With the stock now trading at $14.36, that's a paper profit of just over $5 billion.There has been no indication of when Berkshire could look to exit the 10-year deal. While the $300 million annual dividend is costly for Bank of America, it must pay a 5 percent premium to Buffett to buy him out before the deal is over. Nonetheless, both Goldman Sachs and General Electric chose to buy out Buffett in less than three years.

As I've often noted in the past, it's the best investors that are usually the most diligent about locking down and taking their profits once they're substantial on paper - it doesn't look like Buffett is ready to make that move here and he's $5 billion in the black - interesting.

Perhaps the lunch and meet up with Moynihan was a litmus test for Buffett, to try and get a grasp on his outlook - if not on the company - then at least how he feels about the sector and the economy from a macro sense. Any stock moves in the coming days from Buffett will be very telling. If he reports to have sold, he clearly wasn't happy with how things went. Should we hear silence, we can assume what we're assuming now: Buffett is still riding the Bank of America wave. QTR is bullish on Bank of America here, as well.

And why not? Last month, Bank of America beat earnings expectations on both lines, reporting Q2 EPS of $0.32 and revenue of $22.9B. The bank's Q2 profits skyrocketed, up 70%, assisted by cost cutting and investment banking. Bank of America, the second-biggest bank in the country, managed to cut expenses about 6%. It cut about 18,000 jobs and reduced total employees by about 11%. Their cost cutting has continued, with Financial Times reporting earlier this week that Merrill Lynch is going to dissolve into Bank of America:

Under chief executive Brian Moynihan, BofA has been attempting to shed expenses through cost-cutting programmes such as "Project New BAC." Merging Merrill with BofA could help the bank avoid some legal and regulatory expenses, including having to file separate reports with the US securities regulator."As part of Bank of America's efforts to streamline its organisational structure and reduce complexity and costs, it has reduced and intends to continue to reduce the number of its subsidiaries, including through intercompany mergers," the filing said.

In addition, the company's stock has been performing consistently over the last year, having nearly doubled in price. Investors that have been in for the last three months have yielded a rather pedestrian 4.7%, but those that have been in for the last twelve months have been rewarded with an upside that's more than 70%.

(Click to enlarge)

So, Monynihan continues to show that he has his head screwed on straight and is concerned with getting the company's fundamentals in order before moving forward.

In keeping with getting the fundamentals in order, Moynihan has put his head down and knocked out an onslaught of BAC's legal woes through settlements, slowly and steadily, one at a time.

As I stated in my last article, "Why You Should Ignore Bank of America's Legal Woes":

In all seriousness, this legal onslaught is a battle that the company has been at since earlier this year, as CEO Brian Moynihan has been systematically knocking lawsuits out of the way slowly, steadily, and one at a time. The year started with a $1.7 billion settlement with mortgage insurer MBIA, which was mostly cash with a small investment in MBIA securities.Although this DOJ civil suit is likely to give investors pause when they see the headline, it's likely to be settled for a much smaller amount than the others once it goes through the legal ringer headlines.

At the end of that article, I reiterated my bullish sentiment on the company, citing the same reason I just suggested that Zillow (Z) isworth a buy at its "out of whack" valuation : the underlying macro catalyst of the housing market recovery.

I remain bullish on Bank of America, even in the midst of these recurring legal troubles. One by one, as they're settled, they cannot be brought up or dealt with again in the future. A settlement in this case essentially knocks out another piece of the total litigation spawning from the 2008 collapse. Soon, there will be no one left to deal with.Sure, it's likely to cost the company some money in the interim, so we may not see a significantly reduced amount of spending in terms of legal expenses, but as the company continues to go "lean and mean", cutting branches and employees, it shouldn't make a difference.

In addition to following Buffett, there's a whole host of reasons that I continue to be bullish on Bank of America going forward:

- The stock, along with other banking stocks, had significant momentum coming out of earnings.

- The aforementioned attention that Moynihan places on the basics, fundamentals, and not spreading the company too thin in a restructuring time. From The Wall Street Journal online:Last fall, Mr. Moynihan announced plans to speed up cost cutting. The bank had 257,158 full-time employees at the end of the second quarter, down 6.6% from a year earlier. It also reduced branches by 4.8% to 5,328 at the end of the quarter. Executives said they hope to slim down to about 5,000 branches by the end of 2014.

- There's a pretty good chance that they're going to increase dividends moving forward as they gain momentum and profits continue to rise. In March of this year, the bank won Federal Reserve support to buy back up to $5 billion in stock. This was the first primary "give back" to shareholders since the financial crises ended.The Fed's change of heart and "all clear" on BAC's operations here show that there's a momentum of shareholder goodies that could be starting - while inadvertently also giving investors the idea that if the Fed approves, BAC must be back in good shape.In addition, it's worth noting that some banks, including BAC, may have to retain earnings in order to meet the proposed leverage ratio minimum - at the risk of getting bonuses, stock buyback, and payouts to shareholders curbed.

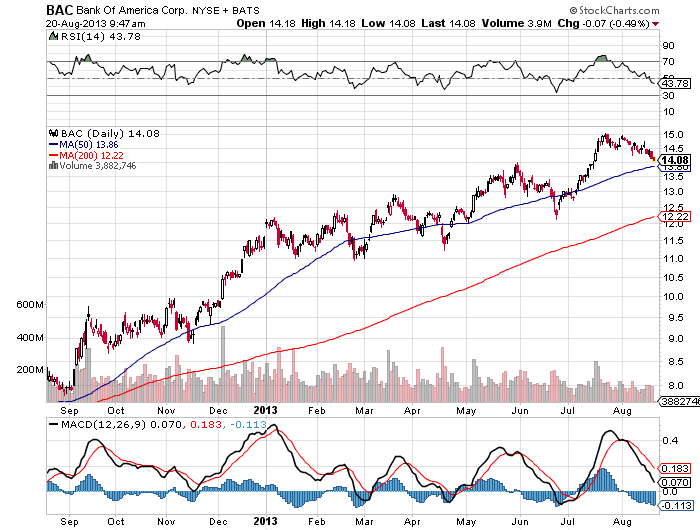

- The stock has significant technical momentum, from a charting perspective.

- Analysts almost everywhere seem to be bullish on the company. See "Reason 5" in my article "5 Simple Reasons..." for more on this.

- Possibly one of the things discussed at lunch between Moynihan and Buffett, the banking sector as a whole seems to be improving; but not only that, improving in the face of what's going to be a coming Federal Reserve Taper. Make no mistakes about it, the Fed is going to be the single biggest catalyst for how banks perform in the upcoming year. The fact that BAC, along with the rest of the sector, continues to show strength, is a bullish sign.

- The housing market recovery - can't state this one enough. Best of all, you don't really need to be an analyst to figure this one out. It's clear as day, even in my Midwestern town that I live in. Houses that were foreclosed on are being sold, housing projects that stalled years ago are being completed, and housing values and new home prices are noticeably higher than they've been in the past few years.

- Finally, as I stated in a previous article, I like the company's forward looking innovation through automation.Bank of America has consistently been making strides to go automated in its entirety, in terms of banking; similar to the way tons of food stores now have implemented self-scan devices for checkout. The more machines in place, the more automation, the less tellers needed, the less the bank spends. This has been an initiative that the bank has been working on for the past few years, and it's my contention that this forward looking "automation innovation" is going to yield the bank tangible results in terms of cost cutting and general efficiency in the future.

It is with these sentiments that I continue to reaffirm my bullish sentiment on the company. Short term risk here does exist, should Buffett sell his position - money is likely to follow him out the door. Also, Bank of America, like most other banks is vulnerable to potential negative impact from rising interest rates. Neither of these two are likely to effect the stock in the coming months, in this investor's opinion, so QTR remains bullish on Bank of America. Best of luck to all investors.

By Quoth The Raven

No comments:

Post a Comment