January 9, 2013 | 3 comments | includes: ERUS, EWZ, FXI, INDY, VWO

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I have expressed my bullish views for U.S. equities in several of my earlier articles. I maintain that view with a 3-5 year time frame. In this article, I would be focusing on emerging economies and the reasons to consider meaningful equity allocations to emerging markets. I can say with some conviction that emerging markets will easily outperform developed market equities over the next decade. Therefore, I would not hesitate in allocating 30-50% of my equity portfolio in emerging markets.

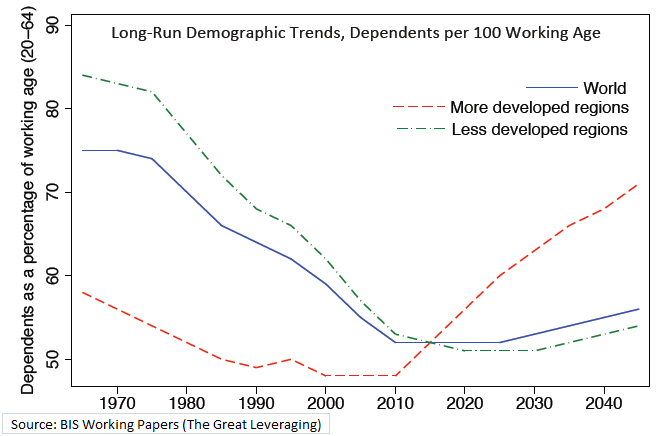

I would consider demographics as one of the most important factors to back my case for meaningful investment in emerging markets. The chart below gives the long-term demographic trend for emerging and developed economies. It is evident that there will be a sharp rise in dependents as a percentage of working age population over the next 2-3 decades for developed economies. For emerging economies, the trend is favorable for the same period.

(click to enlarge)

I am listing this as the most important factor because the change in demographics would impact consumption for largely consumption-driven developed economies. The increase in the number of dependents will put pressure on the working population and the spending trend might decline as a percentage of GDP. I proved this point in one of my earlier articles, which showed that the GDP growth in the U.S. has largely been driven by social programs along with healthcare spending after the financial crisis. Clearly, it is not healthy or sustainable growth.

For emerging economies, the demographics are very favorable and there is a gradual increase in standards of living. This is a perfect recipe for robust GDP growth in the long term. With the high savings rate in most of the emerging economies, the consumption story will unfold going forward leading to a healthy production and consumption-oriented economy.

Just as an example, the retail sector in India (home to over 1.2 billion people) is just worth $350 billion currently. However, it is expected to grow at a CAGR of 15-20% over the next few years. China (home to over 1.3 billion people) will see a similar growth in the consumption story with a high savings rate. At the same time, infrastructure and production will also continue to grow as urbanization increases in emerging economies. All these factors will aid in robust GDP growth.

The trend I am talking about is already evident from the next two charts. The first chart shows the gradually rising share of developing countries in global growth. Over the years, developing countries' contribution to global GDP growth has been trending higher. I expect this trend to continue in the long term.

(click to enlarge)

The second chart shows the time in expansion for emerging and advanced economies and the median growth in GDP per capita during expansion. The trend is clear; the time in expansion of advanced economies is on a gradual decline while the time in expansion of emerging economies and low-income countries is trending higher. Similarly, the median growth in real GDP per capita during expansion has been falling significantly for advanced economies.

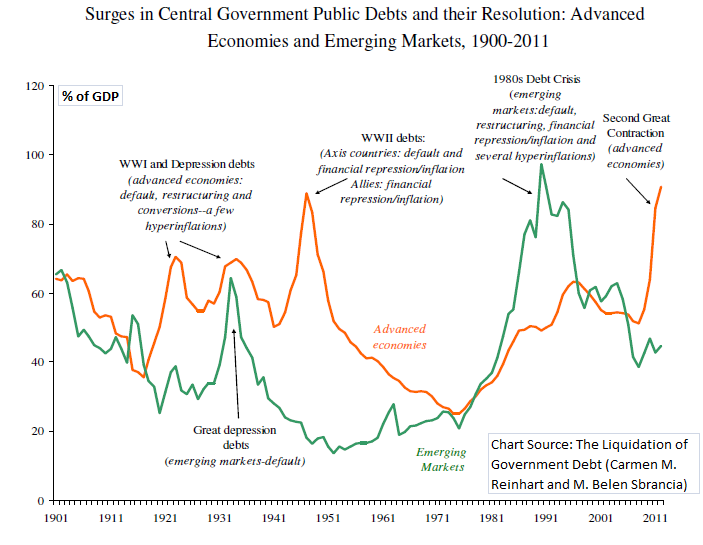

One might argue that this trend will reverse in the near term. I assign very low probability of that outcome as demographics and high government debt will hinder growth in the advanced economies for the long term. I discussed the demographic factor above. The chart below gives the debt factor, which has a detrimental impact on GDP growth. The public debt in advanced economies is near historical highs. According to the research by Carmen M. Reinhart and Kenneth S. Rogoff, above 90% debt to GDP, median growth rates fall by 1%, and average growth falls considerably more. For most of the advanced economies, this threshold level has been breached. Further, high government spending in the advanced economies can also lead to crowding out of the private sector. This can be disastrous for the economy as the private sector has been driving growth after the financial crisis.

(click to enlarge)

Coming back to the government debt problem, I am of the opinion that debt in the advanced economies can only increase from this point intime. Therefore, the situation is likely to get worse in terms of the impact of rising debt on GDP growth. I had discussed the reasons for most advanced economies being in an inescapable debt trap in one of myearlier articles.

Considering these critical factors, it is important for investors to have a good portion of their equity portfolio in emerging markets. There can be periods where the advanced economy equities outperform the emerging market equities. However, in the long term, the returns will be meaningfully higher for emerging equities. I am not suggesting that investors immediately allocate 30-50% of their equity portfolio in emerging markets. A gradual shift towards emerging markets is, however, needed in order to boost portfolio returns.

For the long term, I would consider the following ETFs -

- Vanguard MSCI Emerging Markets ETF (VWO) for exposure to emerging market equities. The fund invests in stocks of companies located in emerging markets around the world, such as Brazil, Russia, China, Korea, and Taiwan. The fund has a low expense ratio of 0.2%.

- iShares FTSE/Xinhua China 25 Index (FXI) for specific exposure to Chinese equities. China looks attractive at current levels and growth in China has bottomed out in all probability in 2012. I would still take a cautious stance and gradually invest in China.

- iShares S&P India Nifty 50 Index Fund (INDY) for specific exposure to Indian equities. I would like to mention here that Indian markets have rallied significantly in the last few months. Therefore, investors can wait for some correction before considering exposure to Indian equities.

- iShares MSCI Brazil Index ETF (EWZ) for specific exposure to Brazilian equities. I consider Brazil as an excellent natural resource play and I remain bullish on agricultural and industrial commodities for the long term.

- iShares MSCI Russia Capped Index Fund (ERUS) for specific exposure to Russian equities. Natural resources (energy) will be the primary growth driver for Russia in the long term. The market does look attractive with a long-term perspective and can give the double benefit of currency and stock market appreciation.By Economics Fanatic

Source:seekingalpha.comcurrency and stock market appreciation.

No comments:

Post a Comment