By Saibus Research :Disclosure: I am long BRK.B.

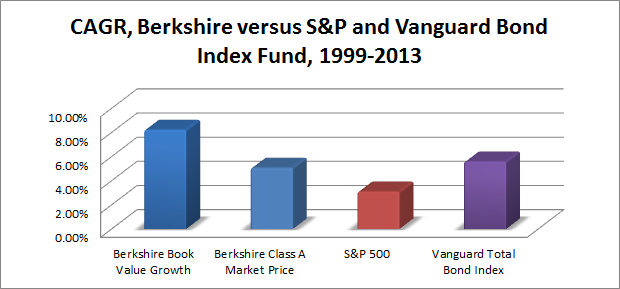

Source: Morningstar Direct

Warren Buffett Says Stop Coddling The Super-Rich

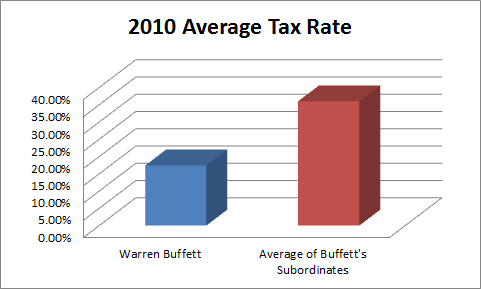

As everyone knows, Warren Buffett wrote an editorial in The New York Times in 2011 in which he urged the government to raise his taxes. In his editorial, Buffett was quoted as saying that he and his "mega-rich friends" have been "coddled long enough by a billionaire-friendly Congress" and "we mega-rich continue to get our extraordinary tax breaks." Buffett highlighted that although he paid nearly $7M in federal income taxes in 2010, it only represented 17.4% of his taxable income and that was actually a lower percentage than was paid by any of the other 20 people in Berkshire's executive office. The rest of Berkshire's executive office staffers saw their tax burdens range from 33 percent to 41 percent and average 36 percent. We think that was real sporting of him to express concern about how his subordinates pay a higher percentage of taxes than him and that led Buffett to advocate for higher taxes on individuals making more than $1M annually.

Warren Buffett Doesn't Practice What He Preaches

One thing we've learned from our 16 years investing is that if something is too good to be true, many times it is. About two weeks after Buffett wrote his Tax-Me-More Op-Ed in The New York Times, the New York Post published a rebuttal to Buffett's Op-Ed that pointed out that Berkshire openly admitted that it owed back taxes going back to 2002. Berkshire had net unrecognized tax benefits of $1B as of its 2010 Annual Report. As of its 2011 Annual Report, Berkshire Hathaway had settled its 2002-2004 tax issues during the 2011 fiscal year, plans to settle its 2005 and 2006 tax issues in the 2012 fiscal year and has $928M in net unrecognized tax benefits as of 2011. We suspected that part of the reason behind Warren's willingness to acquire newspapers for Berkshire Hathaway was to ensure a reduced likelihood that other papers will bring up information that may damage the "Saint Warren" brand. News Corporation (NWS) (NWSA) is the parent company of the New York Postand we believe that this is why the soon to be new News Corporation (which consists of News Corporation's publishing operations) is more profitable than The New York Times Company (NYT) even without the benefit of its soon-to-be former Fox Media and Entertainment properties. We also believe that if Warren Buffett practices what he preached, either Berkshire should pay the $928M in disputed taxes out of corporate funds or Buffett should pay those taxes personally.

Sources: MRQ Reports for News Corporation and The New York Times Company

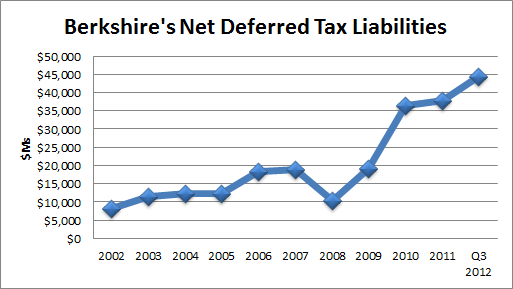

We actually enjoy how Warren Buffett goes around pounding the table for more taxes while working hard to minimize personal and corporate tax expense, particularly with regards to cash tax payments. Berkshire's net deferred taxes payable have increased from $8B in 2002 to $44.5B as of the third quarter of 2012. This includes $13B of deferred taxes payablefrom the 2010 acquisition of Burlington Northern Santa Fe and is primarily due to temporary differences between taxable income as reported to the IRS and pre-tax income as measured by GAAP. The most notable temporary difference between GAAP pre-tax income and taxable income as reported to the IRS is accelerated cost recovery depreciation methods for property, plant and equipment. Berkshire's deferred taxes payable do not include $6.6B undistributed earnings of certain foreign subsidiaries. Berkshire expects to reinvest these earnings permanently rather than repatriating them back to the states and paying up to 40% in net federal and state corporate income tax.

Source: Morningstar Direct

We actually have to tip our hats to Berkshire for its tax moves. We really do, we can see that Berkshire has made its deferred tax liabilities a permanent cornerstone of its financials and has transformed its deferred tax liabilities into a de facto equity source. Granted, Berkshire would have to continue making new investments in its businesses in order to maintain the benefits of this de facto equity source, but we expect Berkshire to be able to continue to do so since its businesses and its investment portfolio generated $7B in free cash flows during the first nine months even after taking into account acquisitions. Berkshire's deferred tax liabilities represent over 10% of its assets and, assuming a 10% pre-tax return on this source of float, this would represent $4.5B of pre-tax interest, dividends and other realized and unrealized investment return and would be almost 11% of Berkshire's 2012 annualized pre-tax total comprehensive income of $40B. Other impressive tax moves include Berkshire's $2.8B in tax-exempt municipal bond holdings and how Buffett allocated Berkshire's portfolio of marketable equity securities to the insurance subsidiaries in order to take advantage of dividend received deductions. These two deductions help Berkshire permanently shelter about $500M annually from taxes.

Relevance of Berkshire's Tax Planning Strategies

Why is Warren Buffett's tax moves for Berkshire relevant for investors? That would be a fair question and to answer it we should turn to Warren Buffett himself. In his book The Warren Buffett Way, Robert Hagstrom pointed out that Buffett, Graham and their followers can see that investors effectively own Class D shares of a corporation while Class A, B and C shares are technically and effectively owned by federal, state and local governments and represent their tax claims. While Class A, B and C owners from the government have no capital risk in the business, these owners get a major share of the corporation's earnings and can vote to increase or decrease their payments on a whim. We agree with Buffett that governments would seek to increase tax rates on companies during inflationary periods and that this would have a negative impact on a firm's ROIC performance.

We think that Warren Buffett said it best when he said if you can eliminate the government as a (39.6%-46%) business partner, the business will be far more valuable. Let us analyze and evaluate just how good Warren Buffett's tax saving strategies has been for Berkshire's shareholders:

- $44.5B in net deferred tax liabilities that have an effective interest expense of 0% and which Berkshire can utilize for investment purposes much like the insurance float.

- $500M in reduced annual tax expense and cash payments due to Berkshire's portfolio of municipal bonds and dividend paying stocks.

- $200M in reduced annual tax expense and cash payments due to Berkshire's mix of foreign business operations.

- $6.6B in permanently reinvested earnings worth up to $2.64B based on a combined federal and net state tax rate of 40% offset by foreign taxes paid net of any foreign tax credits received.

- $928M in unrecognized tax benefits due to difference in what Berkshire owes versus what the IRS has assessed Berkshire.

- Warren Buffett is planning on giving away substantially all of his $51.5B stake in Berkshire Hathaway to charities run by family and friends, and this will help him avoid $12.26B in capital gains taxes and $20.6B in estate taxes.

- Berkshire bought back $1.2B of shares from the estate of a long-time shareholder (which was rumored to be Albert Ueltschi). Ueltschi had joined Buffett's Giving Pledge and if Berkshire bought Ueltschi's shares, then this transaction generated capital gains tax savings of $286M thanks to the stepped up cost basis upon the death of the shareholder and $480M in estate taxes as we expect the proceeds will be donated to charity.

Why Buffett Doesn't Just "Write A Check"

In response to Buffett's "Tax-Me-More" demands, a number of individuals including the principals of our firm have suggested that if Warren Buffett was really serious about wanting to pay more taxes, he should write a check. Supporters of Buffett's "Tax-Me-More" demands have said that even if Buffett gave every penny he had to deficit reduction, it would only be about 4% or 5%. We believe that if Buffett was serious, he would make a significant contribution of his Berkshire Hathaway shares as a gift to pay down the public debt in conjunction with his Tax-Me-More speeches. CNBC anchorwoman Becky Quick actually asked Buffett in a 2007 interview as to why he gives his money to charities instead of to the federal government. We think that Warren Buffett said it best as to why he actively seeks to minimize his tax expenses even though he beats the drum for higher statutory taxes when he said, "I think that on balance the Gates Foundation, my daughter's foundation, my two sons' foundations, will do a better job with lower administrative costs and better selection of beneficiaries than the government." That's why we admire Buffett. We're pleased that he doesn't practice what he preaches and we're pleased that he gave us a ready-made argument against higher taxes.

Conclusion

In conclusion, we have reinforced our thesis behind our Berkshire Hathaway position. While we don't expect Berkshire to generate the compounded annual growth of 19.8% it enjoyed from 1964 to 2011, we expect it generate strong earnings performance and steady book value growth over the long term in excess of the S&P 500. One reason that is less well known as to the secret of Buffett's success with Berkshire is his uncanny ability to mitigate and defer his tax expenses. We calculated that the implied present value of the legal tax loopholes and deferrals that Berkshire utilizes is worth about $55B to Berkshire's shareholders assuming a discount rate of 10% and this represents about 25% of Berkshire Hathaway's market value. We also expect that whoever Buffett taps to succeed him as CEO of Berkshire Hathaway will be tutored on how Berkshire mitigates its tax expenses and payments in order to create a secondary source of float in conjunction with the float from Berkshire's insurance operations.

Additional disclosure: This article was written by an analyst at Saibus Research. Saibus Research has not received compensation directly or indirectly for expressing the recommendation in this article. We have no business relationship with any company whose stock is mentioned in this article. Under no circumstances must this report be considered an offer to buy, sell, subscribe for or trade securities or other instruments.

No comments:

Post a Comment