Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

By Jayson Derrick

Introduction

Verizon Wireless (VZ) will continue to drive higher profitability, with competitive risks not much of a concern. Margins are likely to expand from 2012 and expect Wireline to stabilize and return to top-line growth in the next few years. I am going to outline several key factors which support my thesis that Verizon is a strong buy.

Verizon Wireless (VZ) will continue to drive higher profitability, with competitive risks not much of a concern. Margins are likely to expand from 2012 and expect Wireline to stabilize and return to top-line growth in the next few years. I am going to outline several key factors which support my thesis that Verizon is a strong buy.

Can You Hear Me Now?

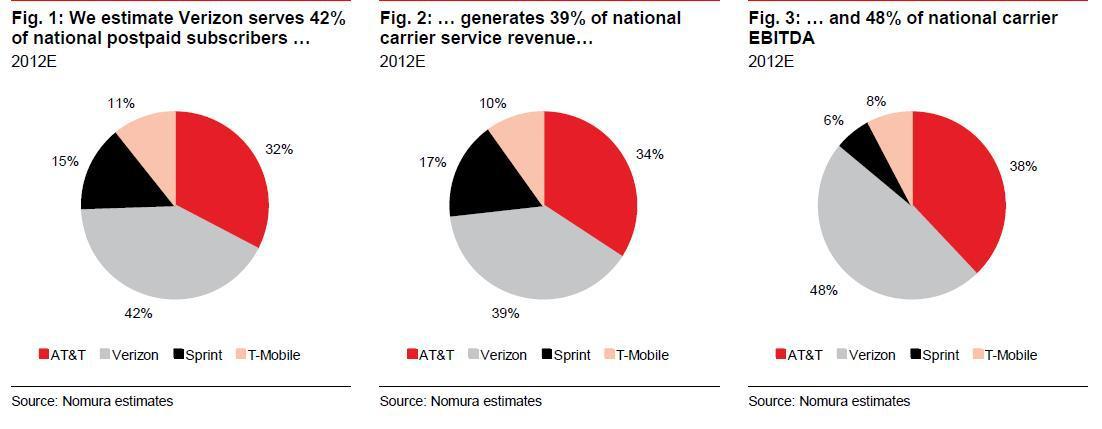

Verizon is the clear market leader with the largest share of high-value postpaid subscribers, controlling 42% of the market (and earning 39% of total revenue in the industry) which translates to having the industry leading EBITDA margins. Verizon should grow EBITDA in 2012 by $4.1 billion, taking a 70% share of national carrier EBITDA growth. Given a head start in LTE network and attractive data plans, Verizon is positively gearing itself towards continued long term profitability. Verizon should generate $14 billion in free cash flow in 2012 which will more than comfortably support the $2.06 annual dividend and maintain flexibility to buy out Vodafone should the opportunity arise. Vodafone maintains a 45% ownership in Verizon (and as such is entitled to nearly half of Verizon's profit) and it is obvious that Verizon and shareholders wants to control 100% of the company.

(click to enlarge)

The True Potential Of The "Share Everything" Plans

As mentioned previously the key to Verizon's success over the competition lies in their data offerings. In June 2012, Verizon launched its "Share Everything" plan providing unlimited voice and text with a shared data bucket that can be used by up to 10 devices. The plan is perfect for consumers that are rapidly shifting away from voice and text messages and demanding more data for less costs as users are now communicating over mobile appls like WhatsApp, iMessage and Facebook messenger.

The "Share Everything" plans lower the initial cost to add data devices or add additional smartphones. It costs $10 to add a tablet to a shared plan versus $30 for a standalone tablet plan with 2GB of data. Adding a smartphones on Verizon's "Share Everything" plan will set the consumer back $40, which is a savings of 50% as a single subscriber would typically pay $80 for the same data. Data usage is expected to grow tremendously over the coming years and Verizon benefits by customers taking larger buckets, with each 2GB of data costing an additional $10 a month.

Wireline Positioned for Future Growth and Margin Expansion

FiOS (a bundled internet access, telephone, and television service operating over a fiber optic communication network) has proven to be a superior product offering, and Verizon has taken the necessary steps now to compete in the future by preparing for customers increased bandwidth needs, driven largely by IP video. FiOS has a 37% penetration of marketed homes, and video a 33% penetration rate. Wireline margins should expand in 2013 driven by lower revenue declines, forced DSL Conversions and a cost savings from the newly signed union contractthat will generate $250-500 million in annual expense savings over its three year time span.

Equipment Subsidies Rising? No Problem, Network Costs Are Falling

Verizon has been very well positioned to overcome rising handset subsidies through rising average revenue per unit and taking $1-$2 billion of cost out of the business in the last several years. Verizon boasts a lower subscriber churn, a better subscriber mix, fewer cell towers, and a slower smartphone adoption curve that feature a wider variety of smartphones. All this translates to the fact that the company simplyearns more revenue per customer at $55.43 than any other carrier. Verizon has been able to lower costs of services and limit the growth of non-equipment-related selling and general administration expenses (SG&A) thereby helping generate incremental EBITDA margins.

Competition Remains Way Behind

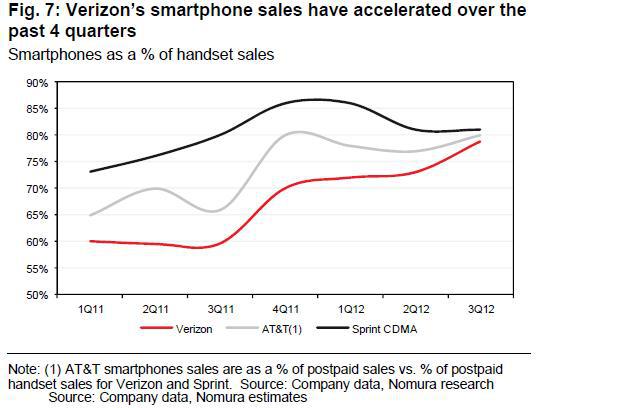

Verizon and AT&T (T) are battling head to head in the high-end, more profitable, postpaid contract customers while Sprint (S) and T-Mobile are battling head to head in the lower end postpaid and prepaid/no contract subscribers. Sprint and T-Mobile pose no threat as Verizon is not a major player in the pre paid market, as only 6% of subscribers chose the prepaid option. It is unlikely to see Sprint and T-Mobile competing with Verizon, making AT&T the only real competition. AT&T currently holds a single edge by offering a 64% smartphone uptake, compared to Verizon's 48%. AT&T also sells more smart phones than Verizon which accounts for nearly 80% of all cell phones sold. A closer analysis reveals this is not so much a concern as Verizon customers have a lower upgrade rate, as well as a later launching of compelling smartphones like the iPhone. Moving forward Verizon should catch up to their peers and in fact Verizon's smartphone sales have accelerated over the past year and are catching up to AT&T very quickly.

(click to enlarge)

No Major Expenses Coming Up

Capital spending should not rise materially from current levels. Verizon has steadily invested in its network. Limiting the need for significant upgrades. Capital spending in 2011 was $9 billion. 2012 should end with Verizon's total spending at $8.4 billion, and the company has already announced that 2013 spending will be similar to 2012.

Conclusion

Verizon stock hit a 52 week high of $48.77 in October but since has seen its shares pullback to where it stands currently at $44.12. This pullback is not based on any fundamental reason and is likely due to profit taking from long term investors which is natural and this can present a good buying opportunity. Verizon is a strong long term buy based on their fundamentals, product offering, positive reputation and clear understanding of their customers current and future needs. Investors should be rewarded with a nice return on investment from "Big Red"

No comments:

Post a Comment