5 Reasons To Buy Astex Pharmaceuticals

May 13, 2012 | about: ASTX

Astex Pharmaceuticals (ASTX) is a leader in innovative drug discovery, development and commercialization, and is committed to the fight against cancer and other life-threatening diseases.

I see at least 5 reasons to buy the stock currently.

1. Promising Pipeline

Astex Pharmaceuticals has established a broad pipeline of small molecule, molecularly-targeted drugs using its drug discovery engine, Pyramid, which is also used to support the company's drug discovery collaborations with leading pharmaceutical company partners.

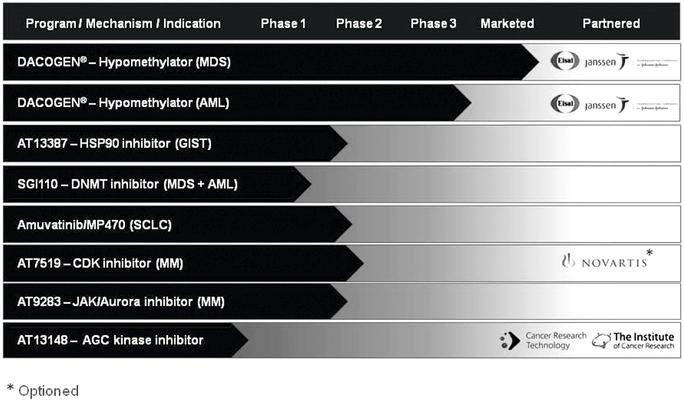

Product pipeline

Astex has a marketed product, Dacogen, indicated for the treatment of myelodysplastic syndromes. Dacogen is marketed by Eisai (ESALY.PK) in North America and Janssen Cilag GmbH, International, a Johnson & Johnson company (JNJ), in the rest of the world.

The company's primary developmental efforts revolve around the products progressing out of their small-molecule drug discovery programs. The company's two lead internal programs are AT13387, a novel HSP 90 inhibitor, and SGI-110, a novel second generation hypomethylating agent.

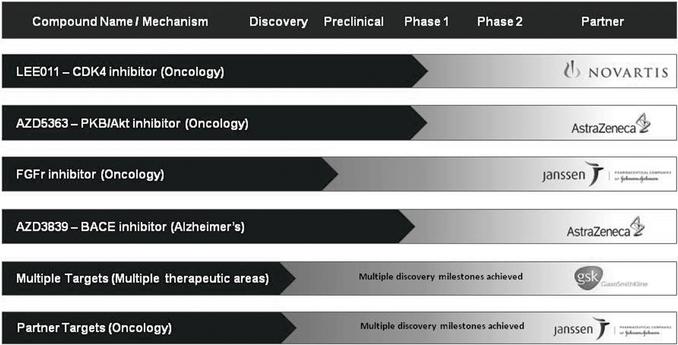

Partnered products and programs

In addition to the company's own clinical pipeline, the company maintains several partnerships with pharmaceutical companies and may receive development and license revenue in the future based on program advancement.

2. Strong financials

The company reported net income for the 2012 first quarter of $4.2 million, or $0.05 per basic share and $0.04 per diluted share, compared with $5.5 million, or $0.09 per basic and diluted share, for the same prior year period.

As of March 31, 2012, the company had $126.2 million in unrestricted cash, cash equivalents, and current and non-current marketable securities compared to $128.1 million at December 31, 2011. The company has no debt. Average annual shares outstanding for 2012 are expected to be approximately 93 million common shares. That creates cash of $1.35 per share.

Royalty revenue for Dacogen is expected to increase up to 10% from the prior year 2011 to a range from $64 million to $67 million in 2012. The company continues to expect to be at or near cash flow neutrality for 2012.

3. EMA decision for Dacogen expected in 2H 2012

On March 2012 Astex's Dacogen partner Eisai received a complete response letter from the U.S. FDA to respond to the application for approval of Dacogen in elderly acute myeloid leukemia or AML. The FDA declined to approve the application. However, in the second half of this year, the European Medicines Agency, or EMA, will rule on Eisai's sublicensee Janssen-Cilag's Marketing Authorization Application, or MAA, for Dacogen in elderly AML. The FDA and EMA drug review and approval processes are not the same. Historically, there have been applications which one agency has approved and the other has not approved. It is important to note that there is currently no approved therapy for elderly AML patients in any jurisdiction worldwide.

4. Clinical data in Q4 2012 for 4 different Phase II trials

Clinical data from SGI-110, a second-generation hypomethylating agent, a follow-on drug to Dacogen, was presented on April 2012 at an oral presentation at the American Association for Cancer Research or AACR Meeting. The company expects to have a clinical data update from the ongoing SGI-110 study by December in time for the American Society of Hematology or ASH meeting.

The company's HSP90 inhibitor AT13387 in combination with amuvatinib is progressing in a Phase II trial in patients with tyrosine kinase inhibitor-resistant gastrointestinal stromal tumors or GIST tumors. Data from this trial is expected in Q4 2012.

Amuvatinib, or MP470, is continuing to accrue patients in an international Phase II clinical proof-of-concept trial in patients with small cell lung cancer. Preliminary results are expected in the fourth quarter.

AT7519, a drug that inhibits multiple cyclin-dependent kinases, or CDKs, is in a Phase II trial in combination with bortezomib in patients with multiple myeloma. Data from this trial is expected in Q4 2012.

5. 4 different ASCO abstracts submitted

The company is going to present 4 abstracts at the upcoming ASCOmeeting in June.

| Compound | Abstract Title |

| Amuvatinib | A phase 2 study of amuvatinib (MP-470), the first RAD51 inhibitor in combination with platinum-etoposide in refractory or relapsed small cell lung cancer (ESCAPE) |

| AT13387 | Phase I study assessing a two-consecutive-day (QD X 2) dosing schedule of the HSP90 inhibitor, AT13387, in patients with advanced solid tumors |

| AT13387 | First in human phase I study - results of a second-generation non-ansamycin heat shock protein 90 (HSP90) inhibitor AT13387 in refractory solid tumors |

| AT9283 | A Phase I Trial of AT9283 (a selective inhibitor of Aurora kinases) given for 72 hours every 21 days via intravenous infusion in children and adolescents with relapsed and refractory solid tumors |

Conclusion

I believe that Astex has very little downside risk at current levels with cash of $1.35 per share and cash flow neutrality for 2012. The company has plenty of upcoming catalyst starting from ASCO in June and with the major EMA decision later in 2012. I would be looking to accumulate the shares below $2.

By Markus Aarnio

Disclosure: I am long (ASTX).

No comments:

Post a Comment