Supervalu Is Drastically Undervalued

Students of physics know that a spring stores energy proportional to the square of the displacement from equilibrium. A variety of factors have caused Supervalu (SVU) stock to be drastically oversold, pushing Supervalu far below fair value. Supervalu's inevitable return to equilibrium may provide an excellent return to investors.

Supervalu is oversold - far from equilibrium - for a number of reasons. It is one of the most shorted stocks on the New York Stock Exchange, with over 33% of the outstanding shares currently being shorted. This has led to institutional ownership over 100%. Traditional wisdom of Wall Street is not to fight the "smart money," and Supervalu was the worst-performing stock in the S&P 500 in the first quarter. The bear case for Supervalu, however, consists of a number of myths. Much of the rest of this article will describe these myths and explain why they are incorrect.

Myth 1: Supervalu is losing prodigious amounts of money

The source of this myth is fairly obvious. Supervalu reported a large quarterly loss in January that turned the trailing twelve months earnings negative. Yahoo reports earnings per share of -$2.46, and this has been used by many as evidence that Supervalu is hemorrhaging money. This large loss, however, is due to non-cash charges of $800 million due to a goodwill write-down and asset impairments. Without that charge, Supervalu would have reported earnings of 24 cents per share in the last quarter, and would have trailing twelve months earnings per share of $1.31.

I like to use owner earnings as the best measure of a company's profitability. The calculation of owner earnings starts from net earnings, adds back non-cash charges such as depreciation and amortization, and subtracts capital expenditures necessary to maintain the business. Supervalu has falling revenues, even though it is expanding some of its properties (such as Save-a-Lot stores). I therefore subtracted all of Supervalu's capital expenditures to obtain an owner earnings figure for fiscal 2011 of $681 million, or $3.21 per share. The myth of Supervalu losses is wrong; Supervalu actually has incredibly strong cash flow and earnings per share.

Myth 2: Supervalu has a crushing debt load

Supervalu has $6.35 billion in long-term debt, while its market capitalization is currently $1.14 billion. 85% of its enterprise value is debt. While this is a high level of debt, it is easily handled by Supervalu's cash flow. In fiscal 2011 Supervalu paid $547 million in interest costs, which is significant, but only about 30% of EBITDA (earnings before interest, taxes, depreciation, and amortization). Interest expenses have fallen steadily from $707 million in 2008 because Supervalu has steadily paid off total debt from $9.5 billion in 2007 to about $6.2 billion currently. Management has committed to reducing the debt load, cutting about 35% of it since 2007, and plans to continue paying off at least $500 million each year. To put this in perspective, management paid off debt greater than three times its current market capitalization since 2007. Yes, Supervalu's debt is high, but it's not nearly as high as the debt to equity ratio makes it look. Management has proven effective at reducing debt and plans to continue to reduce debt; even at this level debt is not handcuffing the company.

Myth 3: Supervalu will be forced to cut its dividend

Some investors see Supervalu's high dividend - currently at 6.8% - and latest quarterly loss and think a dividend cut is inevitable. But, like the above two myths, this reflects a fundamental misunderstanding of Supervalu's finances. When non-cash charges are accounted for, Supervalu generates plenty of cash to pay its interest expenses, pay down debt, and pay its dividend. Supervalu's high yield is a function of its extreme value, and is not a function of an unsustainably high dividend payment. Supervalu recorded net earnings (excluding non-cash writeoffs of goodwill) of $260 million in fiscal 2011, and I calculated owner earnings (cash available for distribution to owners and to expand the business) for the same year of $681 million. Supervalu's yearly dividend payment is just $74 million, for a payout ratio of 28% on net earnings and 11% on owner earnings.

Having debunked three common myths about Supervalu used to support short positions, I'd now like to discuss a few facets of Supervalu's stock and business that you might not be aware of.

Some of the Supervalu shorted stock appears to be from paired trades

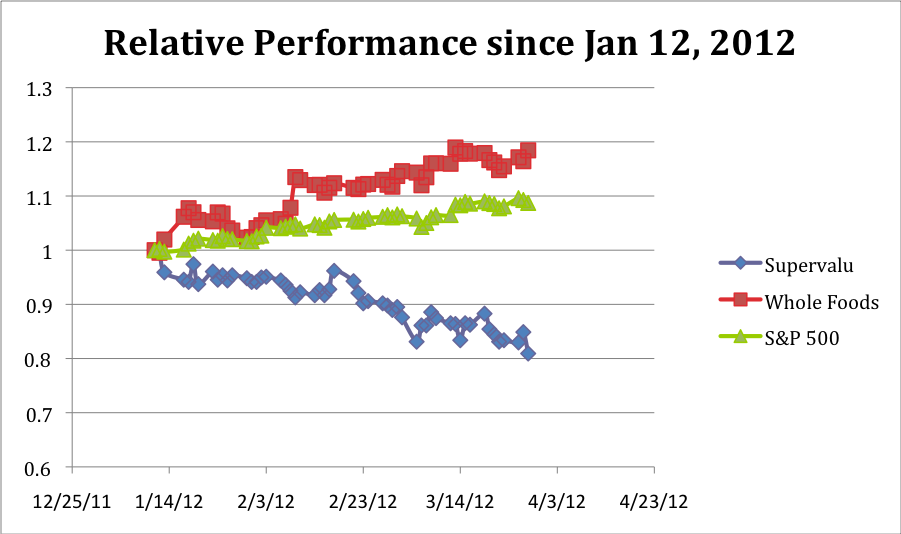

While it's impossible to know exactly how common this strategy is, at least some of the heavy short selling results from paired trades, where an investor buys one stock while shorting another in the same industry. This allows investors to in theory separate the performance of an individual stock from the sector of the market. There has been considerable investment buzz recently regarding several of Supervalu's competitors, including Whole Foods (WFM), Kroger (KR), Safeway (SWY), and The Fresh Market (TFM). Whole Foods in particular has been compared favorably with Supervalu. A chart of relative performance since January 12, 2012 (after Supervalu released its last earnings report) shows that Supervalu is strongly negatively correlated to Whole Foods.

click to enlarge images

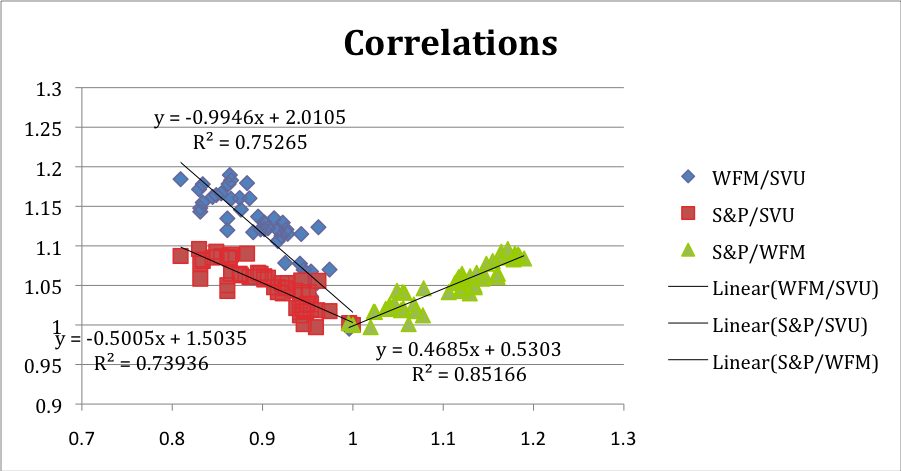

My next chart may be esoteric, but I think it provides a modicum of support for the idea that Supervalu may be used as the short side of a paired trade with Whole Foods. The green triangles show that the S&P 500 and Whole Foods have a positive correlation, although Whole Foods has gone up more than the S&P has. The red squares show the relative percentage changes in the S&P 500 and Supervalu, and show that Supervalu has declined by about twice the percentage change that the S&P 500 has gone up. The blue triangles, however, show an almost perfect match (99.5%) between the percentage increase in Whole Foods and the percentage decline in Supervalu.

There is tremendous insider buying of Supervalu

Unlike the broad market as a whole, which is currently showing insider selling that presages a broad-market decline, Supervalu insiders are buying Supervalu stock. The rough long-term average of broad-market insider selling:buying ratio is 2:1 -- that is, over time, insiders sell about twice as much stock as they buy, since they are often awarded shares as part of total compensation. In February, insiders sold nearly $45 worth of stock for each $1 worth of stock they purchased, and in March, theratio was over $29 to $1.

Supervalu insiders have made 31 buys of Supervalu stock in the last 12 months, compared to just 3 sells. The number of shares bought is 230,091, while the number of shares sold was 48,598. So in the last 12 months, the buy:sell ratio of insiders is 10.3:1, while the ratio based on number of shares is 4.7:1. In the last 3 months, that ratio has improved, as 10 insiders have bought a total of 55,960 shares while no insiders have sold shares. While there are many reasons insiders may sell shares, there's only one reason insiders buy shares: they think the stock is a good investment. So the insider buying is an excellent bullish indicator. In the larger context of dramatic insider selling throughout the market, the insider buying of Supervalu is an astonishingly bullish indicator.

Supervalu is trading at a much lower valuation level than its competitors

Price to earnings ratios from Yahoo! Finance are not the final word on stock valuations. As discussed above, those earnings subtract one-time non-cash charges due to the write-down of goodwill. A more meaningful earnings level excluding those charges is $1.31 per share. But Supervalu is likely to see lower earnings in fiscal 2012, so for comparison I'll use analyst estimates of the next reported years earnings. As you can see, at 4.2 times this year's estimated earnings, Supervalu trades at far lower valuations than any of the listed competitors. Supervalu trades at a P/E 60% below Kroger and Safeway, and about 88% below The Fresh Market and Whole Foods.

Company

|

Price

|

Current Year

|

P/E Ratio

|

Est. Earnings

| |||

Kroger

|

23.84

|

2.32

|

10.28

|

The Fresh Market

|

48.50

|

1.3

|

37.31

|

Safeway

|

19.72

|

1.96

|

10.06

|

Whole Foods

|

83.67

|

2.34

|

35.76

|

Supervalu

|

5.13

|

1.23

|

4.17

|

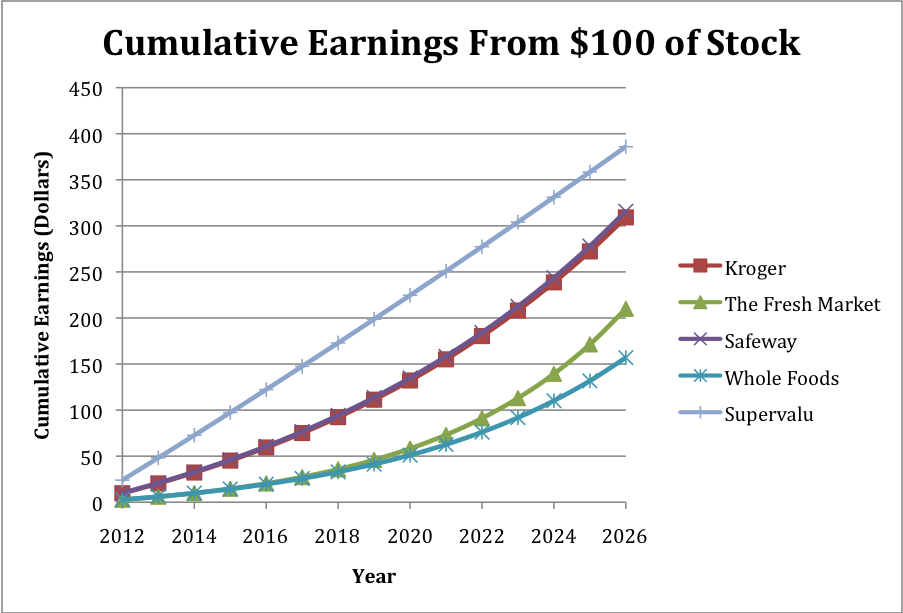

But, you, say, this ordering makes sense. Supervalu has falling revenues, while The Fresh Market and Whole Foods are growing rapidly. Kroger and Safeway have intermediate prospects, and so have intermediate valuations. But while the relative ordering may make sense, the absolute valuations have much more divergence than can be rationally justified. Though each of the other companies is expected to grow faster than Supervalu, Supervalu will provide its investors with far more earnings for many years. Using estimated growth rates provided by Zack's, I've plotted the cumulative earnings made from a hypothetical $100 investment at current prices in each of the 5 companies. As you can see, the faster growth rates of Supervalu's competitors can't catch up to Supervalu's astonishingly high earnings yield. Even 15 years from now, Supervalu well outpaces Kroger and Safeway, and would accumulate roughly twice the total earnings of Whole Foods and The Fresh Market, even assuming 17% and 21% annual growth in perpetuity for Whole Foods and The Fresh Market, respectively.

Conclusion

Supervalu is and has been the target of short sellers who apparently misinterpret the financial status of Supervalu and/or use Supervalu as the short end of a pair trade. This has distorted the equilibrium value, building up substantial potential energy. When Supervalu releases this substantial potential, the stock price may expand rapidly and powerfully, yielding potent profits to patient investors. Though there is no guarantee this will happen in the short term, the more Supervalu departs from equilibrium value, the more Supervalu will appreciate when the potential energy of Supervalu's compressed valuation is released. When Supervalu reports earnings on Tuesday, this could be a catalyst for the shorts to either build or reduce their position. Supervalu is an excellent investment now, and if the earnings numbers are seen as disappointing, an even better buy opportunity may present itself this week.

By Analytical Chemist

No comments:

Post a Comment