Buy MetroPCS: The Value Is Too Compelling To Ignore

April 18, 2012 | about: PCS, includes: CLWR, LEAP, S, T, VZ

Our investment philosophy for the most part is based on investing in companies that leverage clear, secular trends that have little correlation to business cycles. These include growth in smartphones and tablets, cloud computing, and biotechnology. Our preference for leading companies in these growth industries means that we usually have little exposure to what may be considered a classic "value stock," meaning one with a low P/E ratio and a solid dividend yield.

That is not to say that we do not see the merits of "value" investing. Like any strategy, it has its own set of benefits and detriments, and for us, it is simply not the strategy that we choose to follow. However, there are times when we come across a stock whose value is simply too compelling, and too deep to ignore. And we believe that we have found such a stock in MetroPCS (PCS).

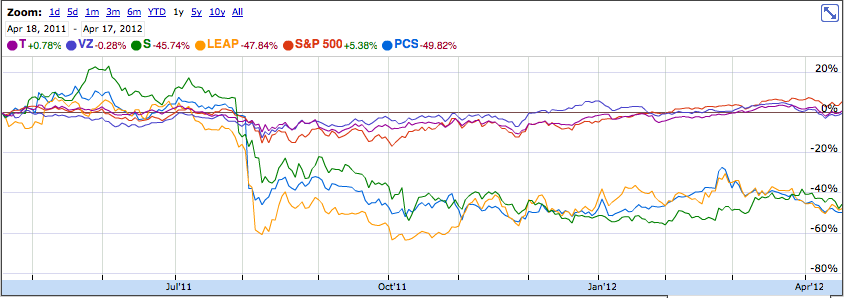

MetroPCS is the nation's 5th largest wireless carrier, and currently serves9.3 million subscribers. Over the past year, the stock has fallen sharply, losing nearly half its value, placing its performance in line with fellow regional cellular company Leap Wireless (LEAP).

Competition in the wireless sector is fierce, and has taken its toll on all companies in the sector, including AT&T (T), Verizon (VZ), and Sprint (S). Some companies are simply not able to generate profits at the present, such as Leap and Sprint (although Sprint's situation is much more complex). Yet, MetroPCS is still profitable, and the fall it has experienced over the past year has caused the stock to arrive at valuations we think are too compelling to ignore. We profile MetroPCS's valuations below, as well as those of its peers in the wireless industry.

Valuation: Cheap by Almost Any Measure

MetroPCS trades at a price/cash flow ratio of 3.57 (according to Schwab figures), earning it the distinction of being the 11th cheapest company in the S&P 500 (SPY) on that basis (different financial websites arrive at different price/cash flow figures; our own calculations yield a price/cash flow ratio of 2.84). MetroPCS reported operating cash flows of $1.061808 billion in 2011, a 6.77% increase from its 2010 oenerating cash flows of $994.5 million. Looking at MetroPCS's stock price would lead one to assume that it is suffering financially, yet its actual results disprove that notion.

MetroPCS also trades at a discount to the rest of the wireless sector on a price/book basis. Based on the company's fourth quarter and full year 2011 results, the company has a book value of $8.05 per share, giving it a price/book ratio of 1.03 as of this writing. For comparison, AT&T has a book value per share of $17.85, giving it a price/book ratio of 1.73. Verizon has a book value of $30.26, giving it a price/book ratio of 1.24. MetroPCS trades at a P/E ratio of 10.1, and a forward P/E of just 9.4.

While this is a very low level for a company projected to grow earnings, we do not think that this metric should be used to evaluate MetroPCS' superiority as an investment over AT&T and Verizon, for their earnings were depressed in 2011 due to a variety of one-time charges and expenses (and Leap and Sprint do not have P/E ratios as they are unprofitable).

Value or Value Trap?

Critics may argue that MetroPCS is not a value stock, but a value trap, for it cannot compete effectively in the wireless industry. And there have been times when that may have been the case. In August, shares fell 37% as the company missed analyst expectations for the quarter. MetroPCS reported earnings of 23 cents per share, below the consensus estimate of 29 cents, and announced 200,000 subscriber additions, below the consensus estimates of 240,000.

The miss was further exacerbated by the company offering only a "soft economy" as reasons for the slow subscriber growth. Still, a 37% drop was too much in our opinion. MetroPCS, despite operating in a fiercely competitive environment, posted improved results in 2011 over 2012 across almost all operating and financial metrics.

MetroPCS Financial & Operational Results, 2010-2011

| 2011 | 2010 | |

| Revenue | $4.847382 Billion (+19.12%) | $4.069353 Billion |

| ARPU | $40.57 (+1.96%) | $39.79 |

| Adjusted EBITDA | $1.331783 Billion (+13.21%) | $1.176355 Billion |

| GAAP EPS | $0.82 (+51.85%) | $0.54 |

| CPGA (Cost per Gross Addition) | $173.11 (+10.08%) | $157.26 |

| Net Subscriber Additions | 1.2 Million | 1.5 Million |

| Churn | 3.8% (+5.55%) | 3.6% |

| Stockholder's Equity | $2.9276 Billion | $2.541576 Billion |

MetroPCS may have added less users in 2011 than in 2010, but its subscribers generated more revenue as they signed up for higher priced plans. Churn rose by 5.5%, but the prepaid business is inherently more volatile than the postpaid business. Leap Wireless, MetroPCS' most direct competitor, reported churn of 3.8% as well for 2011 (Leap Wireless, however, managed to improve this metric from 4.7% in 2010, further demonstrating the variance that can be seen in the prepaid business).

MetroPCS is solidly profitable, and posted record results in both the fourth quarter (GAAP EPS of 25 cents and adjusted EBITDA of $362 million) and 2011 as a whole. 2012, based on current estimates is set to be yet another record year. Current analyst estimates, as reported by Reuters, call for a profit of 17 cents per share in the first quarter, and full year 2012 earnings of 88 cents per share. While this represents a decline in growth from 2011 levels, profits will still rise 7.32% from 2011 levels, and revenue is projected to come in at $5.3 billion for 2012, representing growth of 9.34%.

Even though growth will decelerate in 2012, the company's valuation is low enough to mitigate that impact. At under 10 times 2012 earnings, MetroPCS is being valued as if it will be destroyed by AT&T, Verizon, Sprint, and T-Mobile. We, however, do not see it that way and think that it is better to invest in the stock now before others realize this fact.

Analyst Opinions

Analysts are mixed in their opinions of MetroPCS, but overall sentiment is bullish. It is interesting to note that several analysts have seeming contradictions in the ratings and targets. Several have neutral ratings and offer very lukewarm opinions on the company, but have price targets implying substantial upside. Credit Suisse, for example, rates MetroPCS neutral, yet has a $13 price target on the stock, implying upside of 57%. We offer several analyst opinions below. For the record, the Reuters average price target on shares of MetroPCS currently stands at $12.31, implying upside of 48.67% as of this writing.

- Argus: Argus is quite bullish on MetroPCS, rating the shares a buy and assigning a $15 price target. The firm notes that although shares may be volatile, it believes that MetroPCS has a sustainable business model and that current valuations are quite attractive, on both an absolute and a relative basis. The company's enterprise value/EBITDA ratio is currently 4.4, placing it below the sector average of 5.7 and the 5.9 ratio of direct peer Leap Wireless. MetroPCS' enterprise/EBITDA ratio of 4.4 is also well below its historical average of 7-8.8. Argus' earnings estimates for 2012 are above the Street, with the firm calling for 92 cents in EPS on revenues of $5.2 billion.

- Merrill Lynch: The firm is bearish on MetroPCS, rating the stock an underperform and assigning it an $8 price target. Merrill Lynch believes that shares will be pressured due to the need to acquire either spectrum or another competitor. The firm also cites elevated churn risk as a potential headwind for the company. Furthermore, delays in tax refunds, a key driver of first quarter growth are a source of concern for Merrill Lynch.

- Credit Suisse: The firm has a neutral rating on MetroPCS and a $13 price target. This call is interesting in that even though Credit Suisse recommends moving to the sidelines due to the collapse of the deal with Sprint, they maintained their price target and cited that MetroPCS is now in play.

- S&P: S&P has a buy rating and $15 price target on MetroPCS, citing the company's strong balance sheet, and recent initiatives to reduce churn and accelerate subscriber growth. S&P also thinks the company's early moves towards a 4G LTE network provide it with a first-mover advantage, and that consolidation in the pre-paid wireless market will ultimately reduce pricing pressure across the industry.

- Morningstar: The firm has a buy rating and $14 "fair value" for MetroPCS. Morningstar believes that operating margins will be stable for the foreseeable future, thanks to the company's economies of scale, but its enthusiasm is tempered by the inherently unpredictable nature of churn in the prepaid market.

Sprint: Deal or No Deal?

We turn now to rumors of a takeover by Sprint. The offer was reportedly nixed at the last minute by Sprint's board. We think that this move was for the best, at least from Sprint's perspective. Sprint's stock price is too low to effectively fund a takeover without massive dilution. Furthermore, the company has far too much to deal with as it is without adding another element into the mix (however, we applaud Sprint for its solid execution on Network Vision, the iPhone launch, and the general turnaround that the company has seen).

The termination of the deal with Sprint calls to question whether or not another suitor for MetroPCS will emerge. Verizon, as the other national CDMA carrier, seems like a logical choice, but we do not think that such a deal will pass an anti-trust review. Nor will a deal with AT&T, which would add a host of other technological issues to resolve.

A merger with another, "non-national" carrier, namely Leap Wireless, is certainly possible, but we have not seen any solid rumors or evidence to suggest that such a deal is in the works. MetroPCS, however, has hinted that it is open to a spectrum deal with Clearwire (CLWR), a move thatLeap Wireless has already made. Clearwire and Leap signed a 5-year wholesale LTE deal in March.

Conclusions

We think that there is too much value in shares of MetroPCS for investors to ignore the company. The stock has fallen sharply over the past year, even as the company reported record profits and revenues, and is forecast to do so again in 2012. We think that this contradiction between the company's performance and its stock price will eventually end. MetroPCS is trading as if the company will be driven into bankruptcy because of competition in the prepaid wireless market.

But its results disprove that thesis. The company is solidly profitable, has increased ARPU, and has solid operating cash flows. In addition, MetroPCS is valued at deep discounts to both its peers and the broader market (on a price/cash flow basis, the stock is one of the cheapest in the S&P 500). While we may not gravitate towards value stocks, we believe the value in shares of MetroPCS is too compelling to ignore. And we think that investors who add to or initiate positions in MetroPCS will be rewarded for their belief in the company.

By Helix Investment Management

Additional disclosure: We are long shares of T and VZ via the SPDR Dow Jones Industrial Average ETF. In addition, we may initiate a long position in PCS in the next several days.

No comments:

Post a Comment