Ford: Strong Buy Recommendation

In October I

recommended Ford (F) as a Buy, and my

recommendation for this Stock comes again. This company has performed

exceptionally well in regard to its peers and its improving industry. Despite not taking a Government bailout, Ford was able to rise up

through the rubble and raise its credit rating in the process. With continued growth

in the market and upside in sales I believe Ford is a smart choice both on the

road and in your portfolio.

The current market price for Ford is $11.71 with a one-year analyst price target of $16. This represents a 36.65% upside potential. Ford has a market cap of $44.50B and an enterprise value of $119.06B. This behemoth car company also has a gross profit margin of 14.83% compared with its competition: Genereal Motors (GM) gross margin is 12.18% and Toyota Motor Corporation's (TM) is 11.31%. Quarterly revenue growth is at 10.60% while GM’s is 7.80% and TM’s is a sluggish -4.80%. Furthermore, F's ROE is the highest within its Auto & Truck Manufacturers Industry. For two years now Ford has continued to outshine its peers.

Restructuring the business has been a major part of its business and in doing so optimized its financial health and performance. In 2000, Ford acquired Land Rover from BMW Group for $1.9 billion. In June 2008, the company sold Jaguar and Land Rover to Tata Motors for $2.3 billion, but used about $600 million of the proceeds to fund the Jaguar and Land Rover pension plans. In late 2008, the company reduced its stake in Mazda from 33% to 13.8% (now 3.5%).

From the Ford site: - (click chart to expand)

I feel this shows a sign of what’s to come from this auto company. I must admit I am partial to this company because I own stock and drive a Ford. However, this bias does not come without warrant. The years following the recession were devastating for the auto industry, and even forced GM to file bankruptcy even after a government bailout. This explains the low price that haunted this automaker, but this also opens the door for substantial growth potential. Now that Ford has proven itself a strong company that can weather any storm whether that is a global recession or rising gas prices, it is time to load up on shares. While it may take some time to get back to the $35 days, the $20s may not be as far away as we think. Sales are expected to continue to grow past 2012 further helping the company’s bruised financials.

While net income and EPS may fall slightly due to higher taxes, pretax profits are expected to rise. Also, at 11% of estimated net income the reinstatement of its dividend I feel is a very good move on its part, even though it is a mere $0.05 quarterly (1.71% yield). A rise in sales of 11% is a milestone achievement and once again is a glimpse of what I feel is yet to come.

Overall, Ford plans to focus its investments on smaller, more fuel-efficient vehicles that will result in a more balanced global portfolio to keep pace with the worldwide shift in demand. This pattern mixed with its growth projections I feel offers a great buy opportunity for any portfolio.

Disclosure: I am long F.

January 17, 2012 | about: F, includes: GM, TM

The current market price for Ford is $11.71 with a one-year analyst price target of $16. This represents a 36.65% upside potential. Ford has a market cap of $44.50B and an enterprise value of $119.06B. This behemoth car company also has a gross profit margin of 14.83% compared with its competition: Genereal Motors (GM) gross margin is 12.18% and Toyota Motor Corporation's (TM) is 11.31%. Quarterly revenue growth is at 10.60% while GM’s is 7.80% and TM’s is a sluggish -4.80%. Furthermore, F's ROE is the highest within its Auto & Truck Manufacturers Industry. For two years now Ford has continued to outshine its peers.

Restructuring the business has been a major part of its business and in doing so optimized its financial health and performance. In 2000, Ford acquired Land Rover from BMW Group for $1.9 billion. In June 2008, the company sold Jaguar and Land Rover to Tata Motors for $2.3 billion, but used about $600 million of the proceeds to fund the Jaguar and Land Rover pension plans. In late 2008, the company reduced its stake in Mazda from 33% to 13.8% (now 3.5%).

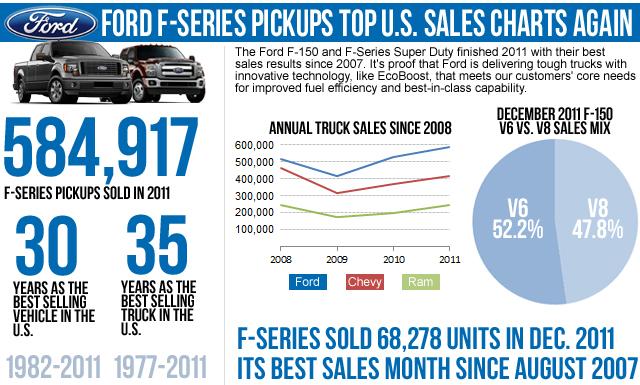

From the Ford site: - (click chart to expand)

Ford brand 2011 U.S. sales increased 17 percent, totaling 2,062,915 vehicles, sealing the brand’s first three-point market share gain over three consecutive years since 1970. Total Ford Motor Company sales for the year increased to 2,148,806 vehicles, up 11 percent for the year.

In December, Ford brand sales were 201,737, up 16 percent from a year earlier. Ford sold 68,278 F-Series pickups in December, representing its best December sales results since 2006. For the year, F-Series sales totaled 584,917 trucks, making it the only vehicle to break the 500,000 vehicle sales mark last year.

I feel this shows a sign of what’s to come from this auto company. I must admit I am partial to this company because I own stock and drive a Ford. However, this bias does not come without warrant. The years following the recession were devastating for the auto industry, and even forced GM to file bankruptcy even after a government bailout. This explains the low price that haunted this automaker, but this also opens the door for substantial growth potential. Now that Ford has proven itself a strong company that can weather any storm whether that is a global recession or rising gas prices, it is time to load up on shares. While it may take some time to get back to the $35 days, the $20s may not be as far away as we think. Sales are expected to continue to grow past 2012 further helping the company’s bruised financials.

While net income and EPS may fall slightly due to higher taxes, pretax profits are expected to rise. Also, at 11% of estimated net income the reinstatement of its dividend I feel is a very good move on its part, even though it is a mere $0.05 quarterly (1.71% yield). A rise in sales of 11% is a milestone achievement and once again is a glimpse of what I feel is yet to come.

Overall, Ford plans to focus its investments on smaller, more fuel-efficient vehicles that will result in a more balanced global portfolio to keep pace with the worldwide shift in demand. This pattern mixed with its growth projections I feel offers a great buy opportunity for any portfolio.

Disclosure: I am long F.

January 17, 2012 | about: F, includes: GM, TM

No comments:

Post a Comment