According to a series of recent Reuters' articles (one, two, three), Western Canadian Select ("WCS") heavy

blend for July has risen from a $19.25 discount to WTI to a $14.00 discount in

just the past week. The quick $5.25 move was attributable to the expected

startup of BP's (BP) upgraded crude distillation unit at its 405,000 bpd

Whiting, Indiana refinery in late June and news that Exxon

Mobil (XOM) was conducting

preliminary restart activity at its 238,600 bpd refinery at Joliet, Illinois.

The Joliet refinery has been undergoing an overhaul since April 14. Both US

refineries process Canadian heavy crude. The upgrades at BP's Whiting refinery

will enable it to run up to 350,000 bpd of Canadian heavy, up from about 80,000

bpd. That is a 270,000 bpd increase.

According to a series of recent Reuters' articles (one, two, three), Western Canadian Select ("WCS") heavy

blend for July has risen from a $19.25 discount to WTI to a $14.00 discount in

just the past week. The quick $5.25 move was attributable to the expected

startup of BP's (BP) upgraded crude distillation unit at its 405,000 bpd

Whiting, Indiana refinery in late June and news that Exxon

Mobil (XOM) was conducting

preliminary restart activity at its 238,600 bpd refinery at Joliet, Illinois.

The Joliet refinery has been undergoing an overhaul since April 14. Both US

refineries process Canadian heavy crude. The upgrades at BP's Whiting refinery

will enable it to run up to 350,000 bpd of Canadian heavy, up from about 80,000

bpd. That is a 270,000 bpd increase.Light synthetic crude prices from the oil sands is also rising. The July contract, according to Reuters, last traded at a premium of $4.50 per barrel to WTI, up from a settlement price on Wednesday of $2.00 above WTI.

The increase in US refining demand for discounted heavy crude, and the resulting rise in Canadian crude prices, will be strong catalysts for major oil sands producers like Suncor Energy (SU), Cenovus (CVE), ConocoPhillips (COP), and Exxon Mobil going forward. Here is an overview of these companies' oil sands operations:

Suncor Energy

Suncor Energy is the largest producer of Canadian oil sands. In the Q1 earnings release, SU had record quarterly production of 357,800 bpd and a 9% decrease in cash operating costs per barrel in its Oil Sands operations. Through May of this year, SU's monthly oil sands production has averaged 322,000 bpd. An increase of $5.25/barrel is obviously a huge windfall for Suncor.

Cenovus

According to Cenovus' Q1 2013 earnings report, total oil sands production was 100,347 bpd, up 22% year-over-year. Production at Christina Lake averaged 44,351 bpd net, an increase of 79% from a year earlier, resulting mainly from the successful ramp-up of the phase D expansion.

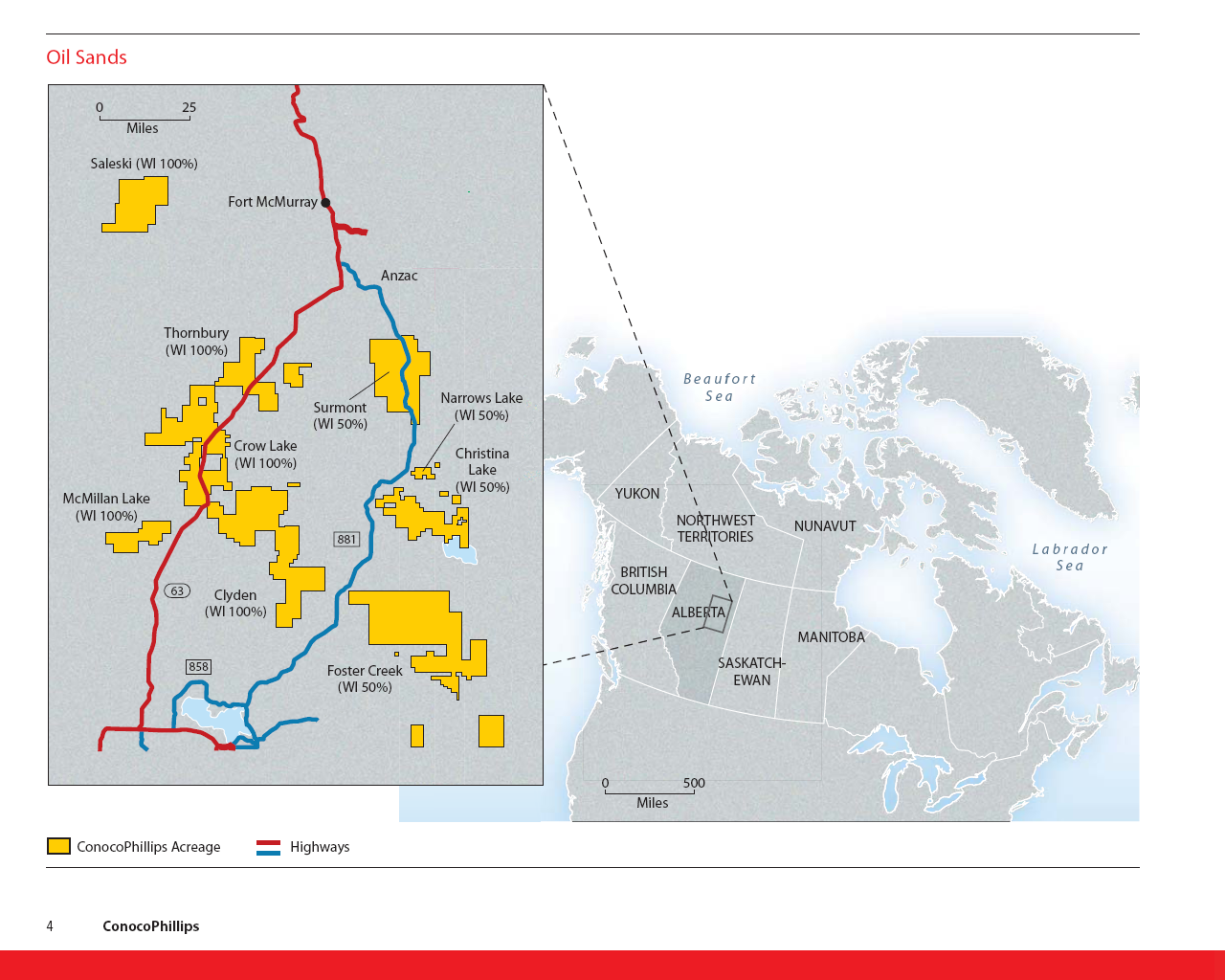

ConocoPhillips

According to ConocoPhillips' Canadian Fact Sheet, the company averaged 93,000 boe/day from its oil sands operations (see chart below). Conoco has three major projects in Canadian oil sands:

- Foster Creek

- Cristina Lake

- Surmont

Conoco's net bitumen production from its Surmont steam assisted gravity drainage (SAGD) operations has grown by an average of 23% over the past 3 years. Surmont is operated by ConocoPhillips Canada and is a 50/50 joint venture with Total (TOT) E&P Canada. When both phases I & II of Surmont reach total capacity, the project is expected to produce 110,000 barrels per day. The 83,000 bpd Phase II is expected to begin production in 2015.

(click to enlarge)

ConocoPhillips holds ~1.1 million net acres of land in the Athabasa Region of northeastern Alberta. The bitumen deposits on these lands is estimated to contain ~16 billion net barrels of resource, making COP one of the largest holders of land and resource positions in the region.

Exxon Mobil

The Kearl Oil Sands project is jointly owned by Imperial Oil (IMO) and ExxonMobil Canada. The project is expected to produce 4.6 billion barrels of oil over the next 40 years. The project will produce 110,000 bpd later this year and that's expected to double by late 2015. At full development, Kearl is expected to produce almost 500,000 bpd of diluted bitumen at full capacity.

Conclusion : Suncor Is The Big Winner

The recent rise in Canadian crude prices is a very positive development for all the companies mentioned in this article, but none so much as Suncor Energy. With oil sands production averaging 322,000 bpd so far in 2013, SU is a monster producer of oil sands and highly levered to realized prices. A $5/barrel increase annualized across 322,000 bpd equates to an extra $598.7 million dollars to SU, most of which would fall directly to the bottom line. That works out to about $0.39 cents per share of net income over 12 months. Put a P/E ratio of 19 (SU's current P/E) on $0.39/share and you get a $7.38 pop in the stock.

If 2013 average daily oil sands production meets the company's guidance of 350,000-380,000 bod, (let's call it 365,000 bpd), and I run $5/barrel extra over 12 months, we get $661.7 million added net income. That works out to an extra $0.44/share, or a corresponding $8.39 appreciation of the stock price (again, using a P/E=19). As you can see, Suncor is very levered to the price of WCS.

Meantime, there are other positive catalysts for Suncor. SU's cash operating costs per barrel have been trending lower. Cash operating costs per barrel for Oil Sands operations decreased by 9% in Q1, averaging $34.80 per barrel compared to $38.10 per barrel in the first quarter of 2012 due to higher production volumes.

Suncor has also shifted from a cap-ex heavy company to a more shareholder friendly company. Back in April, SU increased the quarterly dividend from $0.13 to $0.20 per share. The company also amended its common share repurchase program by an additional $2 billion. Obviously, if the company has been buying shares, the per share numbers presented in the previous paragraph improve accordingly.

If the recent rise in WCS and light synthetic crude prices is sustained, SU will prove to be grossly undervalued at today's closing price of $31.05. The company has a PE=19 and yields 2.6%. Global Hunter recently put a BUY rating on SU with a $45 price target. Barclays recently picked Suncor (and ConocoPhillips) as two of the most undervalued energy companies.

Additional disclosure: I am an engineer, not a CFA. The information and data presented in this article was obtained from company documents and/or sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Please do your own research and contact a qualified investment advisor. I am not responsible for investment decisions you make. Thanks for reading and good luck!

By Michael Fitzsimmons

Source: www.seekingalpha.com

No comments:

Post a Comment