Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Summary

Last week's data was positive, as was the stock market reaction.

Volatility remained high, but attention turned away from Europe and China.

All eyes are now on the Fed and the possibility of the long-awaited first rate hike.

Quite possibly we will have a repeat performance in December.

Short term indicators are more bullish and there are many attractive stocks.

After many years of standing pat on interest rates, there is finally a genuine chance of a shift in Fed policy. The punditry will be asking:

To hike, or not to hike?

Prior Theme Recap

In my last WTWA I predicted that the end of summer and market declines would create buzz about the need to change year-end market targets. That was mostly wrong, lasting for about one day! Once again there was plenty of volatility to discuss. As he does each week, Doug Short's recap explains what happened and his great weekly snapshot lets you see it at a glance. The full article always includes several other helpful charges. (With the ever-increasing effects from foreign markets, you should also add Doug's World Markets Weekend Update to your reading list).

The chart shows the gain for the week (over two percent), but you can readily see why it did not feel that good. Wednesday's big gap opening turned into a 1.39% loss on the day. At least the week was good enough for the Texas boys to take over from "Markets in Turmoil" in CNBC prime time!

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week's Theme

Whether or not the Fed decision this week actually matters is one of the questions, but it is still the story of the week. With an actual policy change in play, expect every pundit to explain what the Fed has done wrong and what it should do now. The question on the lips of all will be:

To hike, or not to hike?

There are secondary questions of what the Fed will do, as opposed to the more popular discussion of what it should do. And finally, everyone wonders about the market reaction.

The Viewpoints

We have a three part question with multiple viewpoints on each. The story has enough complexity to satisfy interviewers, pundits, and even some actual experts.

- Should the Fed raise rates?

- Yes. Why has it taken so long? (Popular among Fed critics).

- No. The U.S. economy remains weak and is threatened by a worldwide recession.

- No. The U.S. is OK, but too many worldwide issues. (The World Bank, the IMF, and Larry Summers are taking this viewpoint).

- The difference between September and December is not relevant if there is a clear statement.

- Will the Fed raise rates?

- Yes. The stated economic conditions have been met.

- No. Fed members are worried about the world economy.

- No. Fed members are worried about propping up financial markets.

- Tossup. The FOMC members are equally split so it is a close call.

- What will be the market reaction to a hike?

- Lower. That is what happens at the start of a tightening cycle. And no semantic nonsense! Removing accommodation is tightening.

- Higher. Removing uncertainty is good.

- Initial reaction is meaningless.

As always, I have my own ideas in today's conclusion. But first, let us do our regular update of the last week's news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week's Data

Each week I break down events into good and bad. Often there is "ugly" and on rare occasion something really good. My working definition of "good" has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially - no politics.

- It is better than expectations.

The Good

There was some very good economic news.

- PPI was flat. Some seem to misunderstand this as bad news. Low inflation is fine as long as the economy is growing.

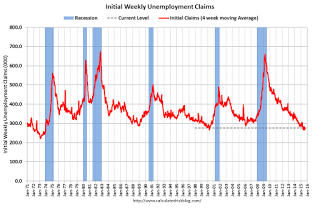

- Initial jobless claims moved even lower, to 275K. Calculated Risk showshow strong this is:

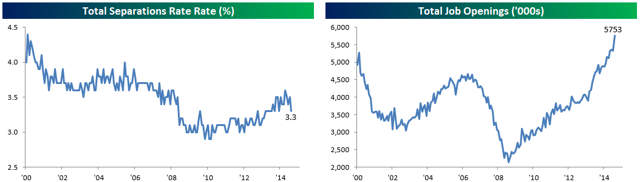

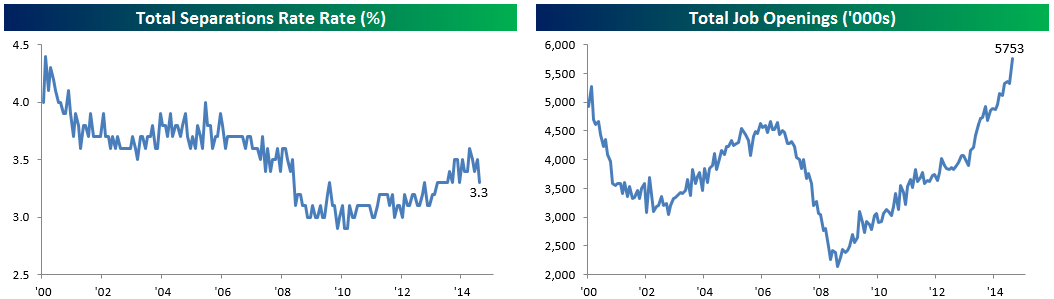

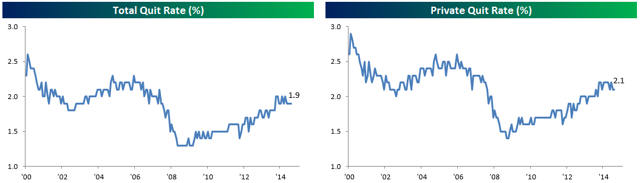

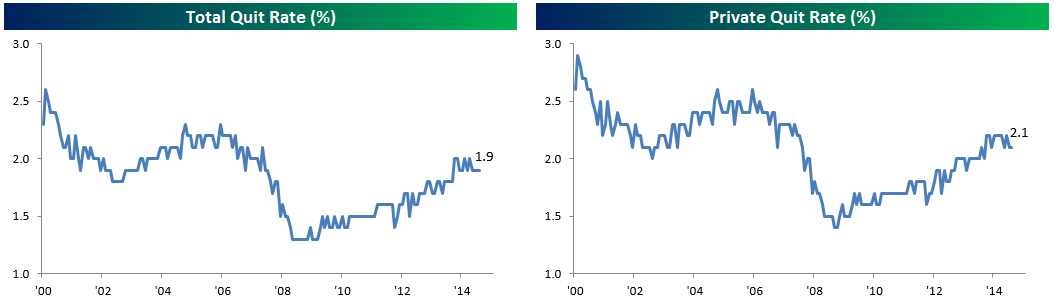

- Job openings increased to all-time highs for the series. Most are reading this as a solid report, as reported by Bespoke with the charts below. New Deal Democrat disagrees, noting some similarities with shifts in the past business cycle. I share concern about the quit rate.

(click to enlarge)

(click to enlarge)

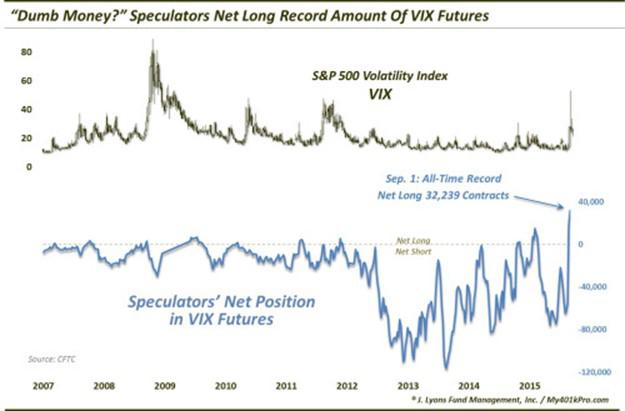

- There are many signs of bearish sentiment, generally regarded as a contrarian indicator.

- Sentiment polls have all swung into bearish territory, some as weak as in 2009.

- Speculation in volatility futures hits a high. Dana Lyons wonders if this is the "dumb money?"

- The budget deficit as a percentage of GDP continues to decline. Scott Grannis has the story and this chart:

The Bad

There was also some negative news last week.

- Automobile accident deaths spiked higher, up 14% last year. Insurance expert Warren Buffett attributes the increase to texting while driving. "If cars are better - and they clearly are - drivers must be worse." (WSJ)

- A looming U.S. government shutdown. Wasn't this supposed to be behind us? Election year dynamics have changed the odds. Chuck Todd, host of Meet the Press, opined on CNBC that odds are now about 50-50. This has gotten little market attention. Putting aside the substantive issues of the parties, a shutdown would be a market negative. (The Hill).

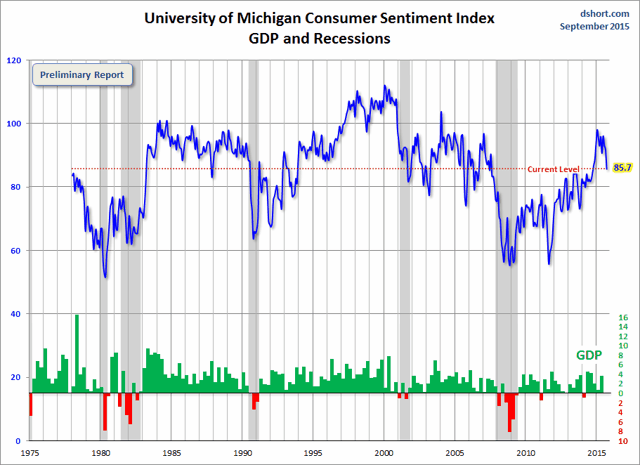

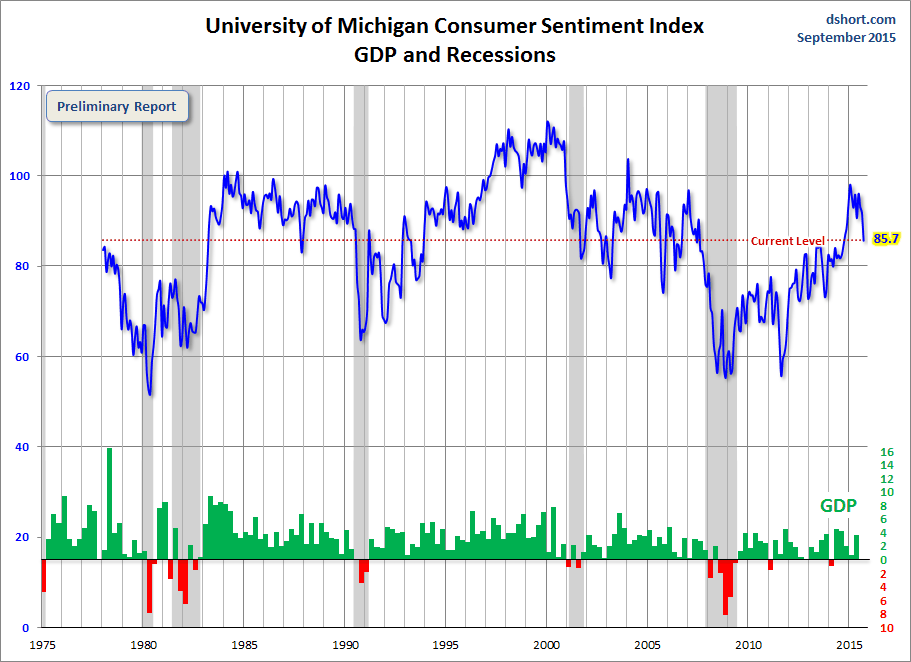

- Michigan sentiment disappointed seriously with a decline to 85.7. Doug Short has the full story and the best look at long-term sentiment data.

(click to enlarge)

The Ugly

The Syrian refugee crisis. There are important economic consequences, but for now the focus is on the human costs.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

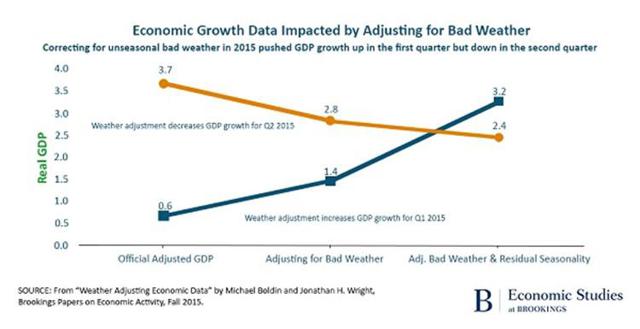

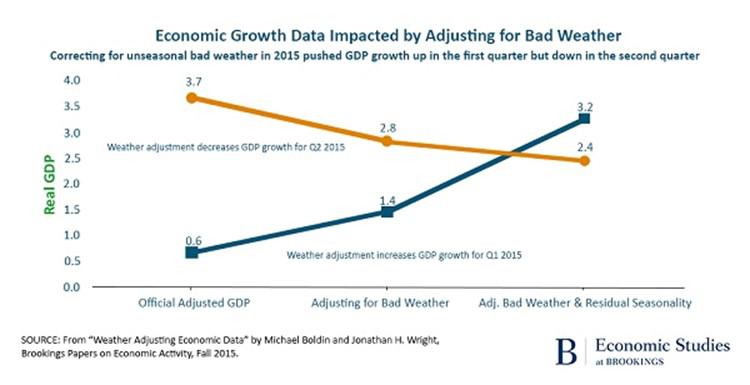

This week's award goes to Michael Boldin and Jonathan H. Wright for their discussion of the effect of weather on economic data. This is a favorite pundit theme, generally used to diminish the significance of all data and/or seasonal adjustments. (e.g. Surprise! It was cold and snowy this winter.) The authors show that there is an important weather effect that goes beyond seasonality. Here is an illustration of the GDP impact:

(click to enlarge)

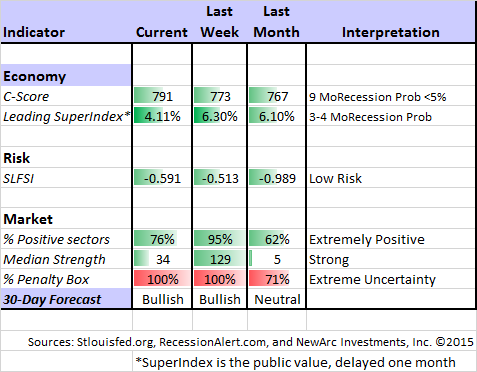

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured "C Score."

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI's business cycle analysis. Jill Mislinski has joined Doug's team and provides this week's update.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a new market climate indicator to reflect risk levels. The market climate was upgraded to positive this week.

Financial Stress. I have been featuring the SLFSI for years, after making it one of our summer research projects. More complete findings are available upon request, but here were two key conclusions:

- This is not a market-timing tool, but a measure of risk.

- The important risk threshold is somewhere around 1.1.

We are not even close to a high risk level.

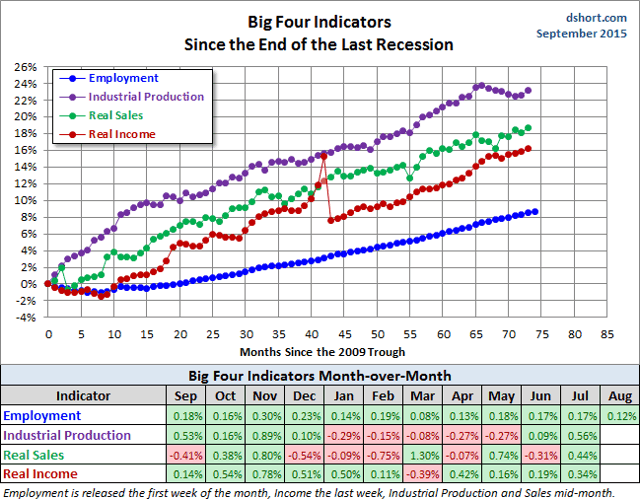

Recession Commentary. Several sources this week were straining to put the R-word in their commentary - "not there yet," redefining recession to mean 2 ½% growth as one major bank did, and other similar tricks. There is a reason that the NBER recession dating is so carefully done, without an effort to provide contemporaneous identification - historical accuracy that we can use for correlations with important factors like corporate earnings and stock prices. The big stock declines are all associated with recessions, so accurate identification is vital. You do not get to cook up your own rules.

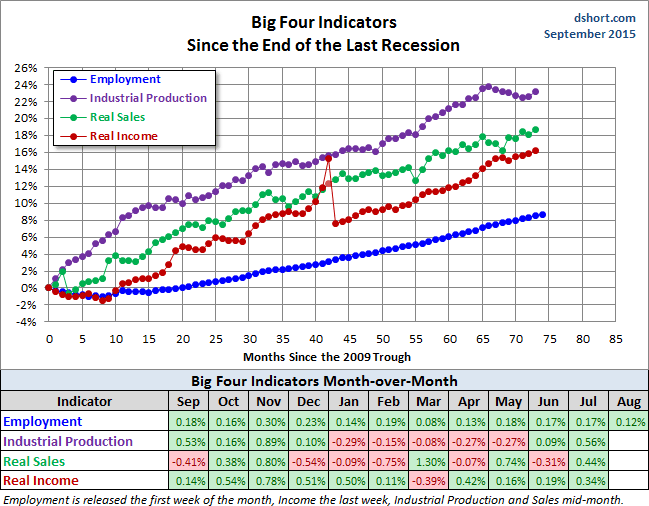

Doug Short is the best source for looking over the shoulder of the NBER committee. It is time for another update of his "Big Four" indicators.

(click to enlarge)

The Week Ahead

It is a big week for economic data. I highlight what I see as important. For a comprehensive listing I use Investing.com. You can filter for country, type of report, and other factors.

The "A List" includes the following:

- FOMC rate decision (Th). And of course, the press conference, dot plot, and supporting data.

- Housing starts and building permits (Th). Leading indicators in an important source of economic strength.

- Leading indicators (F). Popular measure of strength and recession chances, despite changes in the method.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Retail sales (T). Consumer rebound from lower gas prices?

The "B List" includes the following:

- Philly Fed (Th). Gaining recognition as an important early read on the new month.

- Industrial production. Volatile series on an important market sector.

- CPI (W). Continues at an uninteresting level for now.

- Crude oil inventories. Current interest in energy keeps this on the list of items to watch.

Chinese markets remain a wild card. I am not very interested in other regional Fed indexes. FedSpeak is on hold for the meeting and announcement.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a "one size fits all" approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has continued in bullish mode after one of our fastest changes in history last week. Felix is fully invested despite the extremely high level of uncertainty. Felix does not explain these changes, but I observe the sector charts. Felix likes sectors that pull back from the highs and show some evidence of basing. Many have that characteristic right now. The confidence in this three-week forecast remains extremely low with nearly all sectors in the penalty box. For more information, I have posted a further description - Meet Felix and Oscar. You can sign up for Felix's weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify (follow himhere).

Brett Steenbarger draws upon basketball to illustrate a key lesson for traders - discipline in finding and using your edge. I also look forward to reading hisnewest book.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

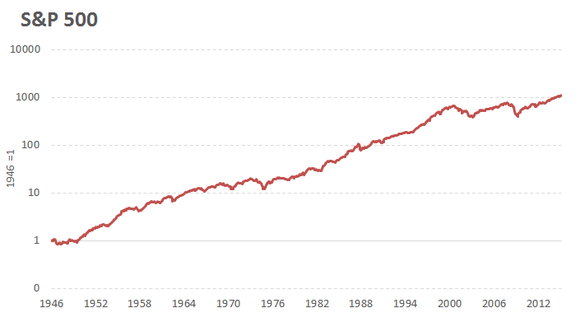

If I had to pick a single most important article, it would be Morgan Housel's helpful advice about market volatility.

(While I am not a fan of a buy-and-hold approach, favoring risk control when recessions loom and always finding the best stocks, I agree with the basic concept. Prepare for and expect volatility. I also like the "optimist/pessimist" approach, which I also employed last week.)

He puts the key argument very persuasively, before analyzing a long series of historical drawdowns:

The punditry world is usually split into two groups: optimists and pessimists. "Are you bullish or bearish?" People want a binary answer.There's not enough attention paid to a third group: Optimists who regularly expect terrible things to occur. It seems counterintuitive, but if you look at history, it's by far the most rational stance.

Here is his key chart, appropriately drawn on a log scale.

Tren Griffin's advice from Charlie Munger is a close runner-up with some similar themes. There are twelve points, but read the first one for Munger's explanation of how he views volatility. Hint: Think actual value, not price.

Stock Ideas

Chuck Carnevale's articles always provide a great mix of instruction and specific ideas. His recent article on building your retirement portfolio is a great example. Not only are there many good ideas (several of which we own), but you will learn how to assemble different stock types in an effective portfolio. You will also learn how to use Chuck's FAST graphs, an indispensable tool.

Dividend stock expert David Van Knapp has a thorough analysis of the benefits of the dividend growth approach. Two weeks ago I highlighted Rob Martorana's article analyzing dividend strategies. David analyzes the original article, raising many excellent points and inspiring a spirited discussion in the comments.

Here are eleven blue-chip stocks at Ben Graham prices. We own several of these as well, so the methodology seems sound to me!

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked this discussion of the possible downside to early retirement.

ETF Investing

Matt Hougan, President of ETF.com, provides some important advice on how to select an ETF. If you trade or invest in ETFs you need to know these three key points. Hint: Don't just go by the name of the fund!

Market Outlook

Expect a lot of gloomy economic commentary.

Ed Yardeni explains that the bearish case seems compelling - but that it always does. He has a good point about psychology and frames the economic issues nicely.

Brian Wesbury (via Todd Sullivan) explains that the political debate brings out negative commentary from all sides. He lists the various reasons for "Everything is bad…" Here is one reason:

Third, there are so many outlets for thought these days that every voice and every opinion has an outlet. C'mon…rising wages and strong car sales are bad?All of this makes the "fog of war" look like a picture window. There is more bad economics, bad math and bad information masquerading as analysis these days than we have seen at any time in the past 30 years.

Read the full piece to see several good specific examples.

Todd Sullivan has another great report from "Davidson," who does a nice review of the generally positive economic data. Read the entire first-rate piece, but here are two key quotes:

The economic data clearly indicate we are well into economic expansion and have been so since early 2009. Perhaps the greatest deception is a result of our own proclivity (likely a genetic based survival trait) to pay far more attention to negative, fearful stories. Humans virtually ignore good news except when the majority of us are in near celebration of it. We do have a lemming quality to accepting consensus opinion as it has been established by 'recognized experts'. Market prices are if anything representative of human psychology at any moment in time. Value Investors who are less connected emotionally than most of us see through this psychological haze.

And…

Much of what we have seen has been driven by Hedge Funds (HFs) which slosh around $3Tril in highly leveraged positions much like panning for 'gold'. When a major shift occurs HFs can generate sharp price changes for an entire sector, but the fears of an end to the world scenario which often accompany these shifts have always translated to into muted economic impact. When prices change, Supply/Demand adjusts. Supply has always made the largest and quickest adjustment historically. We are seeing this in today's environment. A production decline in the rage of 2mil BBL/dy is likely before the end of 2015 based on the acceleration we have witnessed to date. I expect we are likely to reverse the price decline of the past 12mos and even hear that Demand is suddenly more than Supply. Energy demand is coupled tightly to global growth and global growth continues. The dip we experienced the past 12mo in my opinion we will look back on as a temporary dip in our longer term investment philosophy.

This week's Goldman Sachs "possible scenario" of $20 oil is a good illustration of this media/hedge fund process at work. It became a major story on an otherwise quiet Friday.

Final Thought

I'll weigh in on each of the questions about the Fed.

- Concerning appropriate policy, I see it as a close call. The U.S. economy is fine. The impact of a small change is meaningless. Despite this, there is a symbolic effect. Larry Summers noted that it is easy to delay and not so easy to change course once started. The rest of the world is looking for a signal. This Brookings piece did not get much market traction, but it should. Former Fed staffer Julia Coronado, now Chief Economist with Graham Capital, explains that the world will interpret this decision as an indicator of how the Fed interprets data. Fed expert Tim Duy has a similar suggestion.

- Concerning what the Fed will do, I expect no policy change. There will be a statement about the health of the economy and the slack provided by low inflation.

- Concerning market reaction, I think a rate hike would have an immediate negative effect, while standing pat will be a small positive. In the intermediate run (a few weeks?) it does not matter. Short-term market trading clearly reflects this bias.

I am more interested in the long end of the yield curve which will move when the Fed starts to reduce the balance sheet. James Picerno suggests that this is already happening.

Once again we can expect a market week where long-term investors may have a chance to exploit volatility while there is much ado about nothing!

No comments:

Post a Comment