Stonegate Mortgage (SGM) is a rarity among IPOs recently; it came public at a reasonable price despite having a real business, which is profitable and offers enormous opportunities to capitalize on the recovery in the US real estate markets. While most of the Street hasn't yet picked up on the opportunity yet, I believe this ~$440 million market cap firm is a strong candidate to more than triple EPS from $1.85 this year to $5.70 for 2015. Given this, and with SGM currently trading around $17.00 a share, I see the stock as an extremely attractive play in the financials space with upside of more than 65% versus very limited downside of 10%.

Firm is seeing Significant Growth in its Core Businesses:

Stonegate is a residential mortgage company with three different business lines. It is a mortgage originator (1) and mortgage servicer (2) with a separate wholesale funding business (3) that the firm picked up via a bolt-on acquisition of independent mortgage warehouse NattyMac in August 2012. These three business lines all are doing well currently, but look like they will grow significantly in the next few years as well.

The firm originates new prime conforming mortgages on a nonagency platform through three different channels; wholesale, retail, and correspondent.

SGM has been growing the correspondent side exceptionally rapidly with new third party originators (or TPOs) increasing 14% sequentially in the second quarter. NattyMac will help Stonegate in picking up market share in this category as Stonegate can offer quicker turn-around times for third party originators because of its direct ownership of NattyMac. This category is extremely important for SGM as correspondent origination makes up ~70-75% of the firm's new origination business.

On the wholesale side (~15-20% of origination), SGM operates through a network of mortgage brokers, and on the retail side, the firm originates around 5% of its volume through its 27 retail offices in 12 states. I believe this retail origination share will grow markedly in the next few years as SGM looks to increase its retail platform by buying new locations and acquiring existing correspondent branches. This alone will help increase SGM's margins by around 50-60bps (retail originations are roughly 300bps more profitable than other alternatives and I see SGM increasing its retail origination funnel to perhaps 20-25%).

(Industry Wide Origination Volumes)

Stonegate benefits from being both an originator and a servicer in that by originating prime-quality mortgages in the current low rate environment, the firm should be assured of a healthy portfolio with a long service life ahead of it (as consumers will have little reason to refinance). Thus the service segment should benefit directly from strength in the origination segment. Beyond that though, SGM is a healthy servicer already. As of Sept 2013, the firm services roughly $9.5B in outstanding mortgages; a figure which grew 25% since the end of the second quarter! As rates rise, the servicing income on the portfolio should dramatically increase. What's more, I believe that SGM can more than triple its service book by FYE 2014 (based on its origination run-rate of $20B in 2014 which is conservative compared with estimates from the few other analysts who are currently following the stock), and a $60-70B service portfolio by the end of 2015 looks very feasible. Combined with expected rate increases by that point, this will add roughly $2.40 a share to EPS by 2015.

Finally, late last year Stonegate acquired mortgage wholesaler NattyMac as a means of providing warehouse financing to wholesale mortgage brokers. This business is profitable on its own (earning a net interest margin spread on its book), but the real value I see in it to SGM is as a critical differentiator for the firm. In particular, by owning a source of financing for use by correspondents, SGM can provide faster loan closings to the correspondents and ultimately the mortgage client. This is a critical advantage as the length of time between a loan application and a closing date is something that both consumers and mortgage brokers care a great deal about. Thus, the NattyMac acquisition should help drive increased growth in the correspondent business for the foreseeable future as it has been doing for the last year already.

I have already hinted at the catalysts for Stonegate a bit, but to be more explicit, I see four primary catalysts driving the stock going forward.

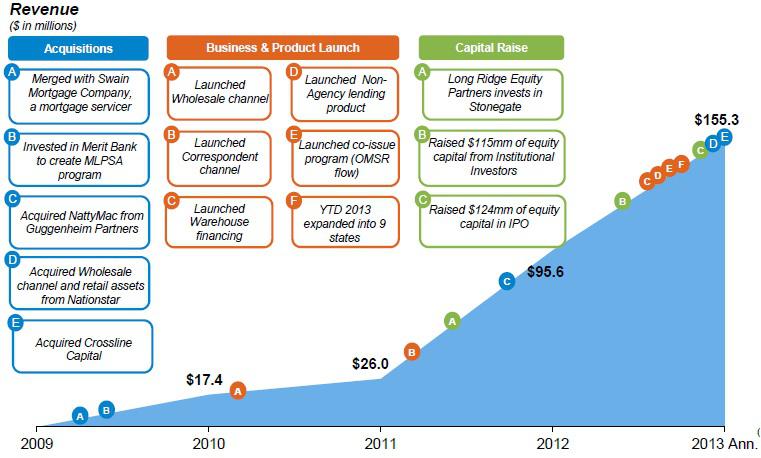

First, the firm's recent acquisitions from NattyMac last year to Nationstar and Crossline in the last couple of months, suggest that Stonegate is pursuing a growth strategy by trying to consolidate a large number of small players in related businesses in the mortgage origination space. By pulling together many small firms, Stonegate should be able to achieve significant advantages to scale while avoiding the legacy issues that currently plague many of the pre-crisis big financial players. In fact, the Nationstar and Crossline acquisitions alone will add at least $4-5B in additional originations for Stonegate next year alone, which makes my $30B forecast very achievable. Nationstar alone produced $3.3B in wholesale originations in 1H '13. Given the unique situation where legacy players have been (and continue to be) battered by legacy issues from the financial crisis, yet players within the industry clearly benefit from greater scale, SGM looks well positioned to gain net benefits from smart acquisitions going forward. Though Stonegate is still small, the firm's rapid revenue growth is very impressive and the company is profitable (adjusted EPS of $0.35 in most recent quarter, GAAP EPS of $0.10), and given the firm's track record, I see its revenue trajectory as likely to continue upward at an accelerating pace for the next few years.

(click to enlarge)

This growth is likely to be both organic as SGM rolls out to the full US late this year and early next year, as well as via acquisitions. The mortgage market is extremely fragmented since the crisis, and this leaves lots of potential targets for Stonegate to buy up at reasonable prices.

(click to enlarge)

Second, Stonegate has been very successful at growing their originations and servicing levels despite an overall slowdown in the mortgage markets this year. Given that the firm is seeing double-digit growth in a very tough mortgage market, it seems like that SGM will be able to continue to outperform as the economy improves and mortgage activity begins to increase again. For those investors looking for strong growth, either organic or through acquisitions, I believe Stonegate is a great choice. The firm is not yet widely followed by analysts in part due to the fact that it only did an IPO a few months ago, but as more analysts start coverage in the next few months, I think the firm's growth characteristics will become much more evident to the market. For evidence of this growth, investors need look no further than SGM's latest earnings report where the company reported adjusted revenues that were 50% higher than year ago levels.

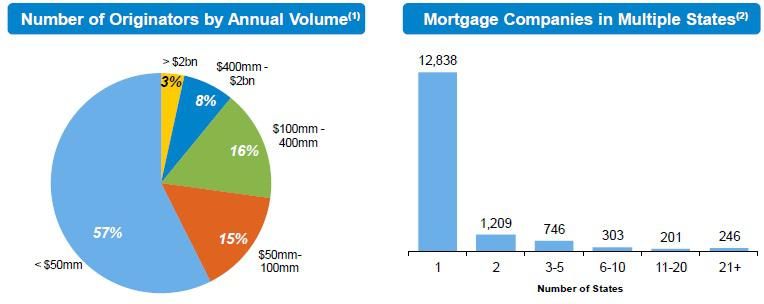

Third, SGM faces a much less daunting slate of competitors today than it would have five or ten years ago. Despite the fact that the housing market and overall economy appear to be gaining speed, legacy issues and greater regulatory scrutiny are holding back firms that previously would have been major competitors for Stonegate. In fact, SGM is among the fastest growing players in the mortgage banking space while big banks, historically the firms that could have crushed SGM through superior marketing muscle and efficiencies, are mostly shrinking as the chart below shows. Big banks are constrained by regulatory capital constraints, the need for cost cutting via layoffs, scrutiny over virtually any acquisition by regulators, and negative public sentiment. By contrast, SGM faces none of these issues and in fact the firm is just getting to the point where it has full geographic coverage across the US. This increased coverage alone should let Stonegate grow EPS roughly 50% over the next year.

(click to enlarge)

Finally, a lot of ink has been devoted to the deleterious effects of rising rates on mortgage origination volumes. And it is certainly true that rising rates make people less likely to buy houses on the whole (and thus take out a mortgage). Yet SGM is likely to actually benefit from rising rates. While the total originations market will shrink as rates continue to rise, financing the remaining originations, and servicing existing originations will become more lucrative. I see this as a major catalyst that should add up to $0.80 per share to EPS by 2015 for the firm assuming rates rise 2%. This is an issue, which investors have so far ignored; regardless of what happens with rates SGM is poised for a great outcome. If rates stay low, the firm can keep building their originations volume and funnel those loans to the service side while waiting for rates to eventually normalize. If rates rise, then Stonegate makes more money off the financing warehouse and the service pipeline.

(click to enlarge)

Recent Results and What is the Market Missing?

Recent earnings are beginning to bear out my thesis on SGM as the firm is continuing to see strong growth. Originations were up 12% in the most recent quarter while origination expenses fell 7 bps (via greater economies of scale), while the firm went from 54% addressable market penetration in the second quarter to 84% in the third by expanding its geographic footprint.

For the full year analysts are looking for adjusted EPS for Stonegate of $1.80-$1.90, which gives the firm a rough P/E of around 9. Granted so far analyst coverage on the stock is very limited, (which in itself presents an interesting short-term catalyst as I think coverage and awareness of the firm will grow in the next few months), but no matter how you look at it, a P/E of 9x on a stock growing as fast as SGM is absurdly cheap. This is especially true when you consider that Stonegate comes with a current tangible book value of about $13 (estimated TBV of $16.10 for FYE 2014), and consensus expectations of $3.15 EPS for 2014. In this case, investors are simply far too concerned about a slowing housing market and the lack of track record for SGM is blinding the investing community to a very interesting opportunity.

Based on my estimates, SGM should earn $1.85 this year, $3.20 next year, and $5.70 in 2015. This gives Stonegate a sizzling 75% growth rate in profits for the next two years (and by 2015 a very healthy portion of the profits should be coming from servicing rather than the more volatile and interest rate sensitive origination side). If my projections are anywhere near right, and my numbers are similar to other analyst forecasts I have seen, Stonegate is massively undervalued. Probably at least 100% undervalued, especially when you consider the multiple expansion that should come from increased profit contribution from the servicing side. (Ocwen for example trades with a P/E of around 25-30x historically.)

Risks:

As big an opportunity as SGM is, there are some risks investors should consider. First and foremost, if the economy were to go back into a recession, Stonegate would definitely suffer (originations would fall and rates would likely decline hitting both sides of its business). This seems very unlikely to me given recent economic data, but it is something all investors should consider.

More practically, intense competition from other mortgage servicers could hurt SGM. Thus far there is no indication that this level of competition will emerge any time soon, and traditional mortgage services like Bank of America are still struggling, but other firms may emerge to challenge SGM. Given the improving economy, Stonegate's aggressive acquisition strategy, and the firm's experienced management, I think SGM would be a formidable competitor for most firms and I don't see competition as being an immediate threat.

Finally, assuming that SGM's mortgages start to go bad or refinance in increasing numbers that would be a very big problem for the firm. But again, with the economy improving and rates rising, neither of these scenarios seems likely to me.

Further, an important point to be aware of is that even if one of these risks should materialize, I see SGM's downside limited to 10% or less. The firm has a tangible book value of around $13 right now, and this is increasing rapidly. I estimate that book value should be around $16.10 by the end of 2014, and so practically speaking, I see that as the floor for the stock. With shares around $17.00 today, this leaves a lot of upside (target price of $38.40 based on 12x forward EPS of $3.20) against very little downside.

Given SGM's growth, its inexpensive valuation in a fairly expensive market, and the limited downside risk, investors should look seriously at establishing a long position in the stock before the stock catches the Street's attention.

Note: All graphics are taken from the firm's investor presentation, but analysis of those graphics is my own.

By Asleigh Rogers

No comments:

Post a Comment