PRCP Highlights

- Perceptron, Inc. (PRCP) produces technology that is used in two of the fastest-growing industries, robotics and 3D printing. It has a lowenterprise value of $60 million compared to its market cap of $92 million, and the company has $33 million in cash with no debt in a hot and growing industry. This makes PRCP an attractive acquisition target.

- Three 3D-imaging companies have been acquired during 2013, and all three acquiring companies are in different industries: AMTEK, Inc.(AME), a diversified machinery manufacturer, LMI Technologies Inc., a 3D-imaging company, and 3D Systems (DDD), a 3D-printing company. This proves PRCP technology is useful in a variety of industries.

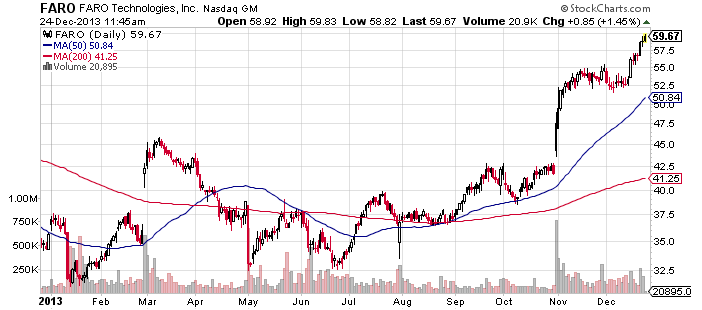

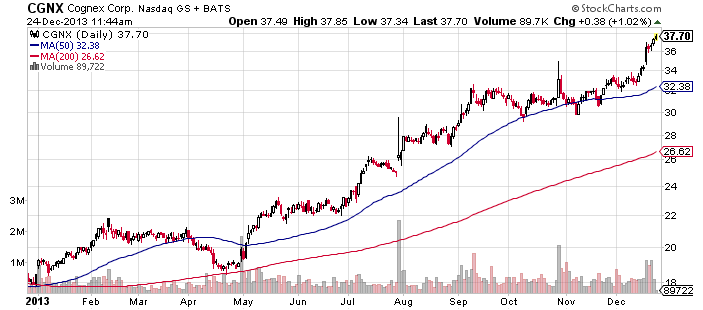

- FARO Technologies Inc. (FARO) and Cognex Corp. (CGNX), both of which are competitors to PRCP, are actively looking to put their excess cash to work by acquiring other companies. PRCP sensors are used in robot guidance solutions, but FARO and CGNX sensors haven't evolved that far yet, a fact that makes PRCP an attractive investment.

- Credit Suisse analysts believe this sector is ripe for future mergers and acquisitions because of increasing demand for industrial automation. Over the past half-year, Google, Inc. (GOOG) has acquired seven technology companies related to robotics. The company's expected targets are in manufacturing, not consumers.

- The 3D-imaging market has a synergistic relationship with both robotics and 3D printing giving PRCP unlimited future potential. The 3D-imaging market is expected to grow as quickly as the 3D-printing market, around a 25-percent CAGR.

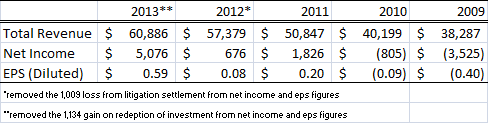

- PRCP's revenues and net income have consistently grown for the past five years. With the company's current backlog at record levels, we foresee even higher sales and growth in future quarters, making it a "Star."

- We believe PRCP is severely undervalued and should be valued at around $26.50 per share, which is up about 250 percent from current levels.

- With FARO and CGNX continuing to make new highs, we expect PRCP also will make new highs soon.

- PRCP has $33 million in cash ($3.69 per share), and that figure is growing. It is possible an acquisition, stock repurchase or special dividend could be announced in the not-too-distant future.

Background

Perceptron is a global, non-contact vision and metrology company with more than 30 years of experience in laser-based technology and applications. Perceptron offers a wide range of specialized inspection and measurement solutions, including dimensional gauging, robot guidance, gap-and-flush, wheel alignment, robotic scanning and portable scanning.Helix is Perceptron's newest 3D-metrology solution and is the world's only sensor of its kind. It utilizes Intelligent Illumination to process features in 3D and then translate the 3D point-cloud data into CAD. This technology is used in two of the fastest-growing industries, robotics and 3D printing.

(click to enlarge)

Introduction

PRCP has a low enterprise value of $60 million compared to its market cap of $92 million, and the company has $33 million in cash with no debt. Poised to benefit from two of the fastest-growing industries, PRCP is a prime, attractive acquisition target. The stock recently has pulled back from its highs, giving investors a buying opportunity as PRCP is much cheaper in valuation than its peers. The 3D-imaging market is expected to grow as quickly as the 3D-printing market, and PRCP technology is used in robotics and 3D printing. This gives PRCP unlimited future potential. 3D Analytics has completed a thorough review of PRCP and determined the stock is grossly undervalued. Consequently, we assign a buy rating on the stock with a $26.50 price target, which is up about 250 percent from current levels.

(click to enlarge)

AMETEK acquires Creaform

On Oct. 29, 2013, AMETEK, Inc. announced it had acquired Creaform, Inc. for approximately $120 million. Creaform is a leading developer and manufacturer of innovative, portable 3D-measurement technologies and a provider of 3D-engineering services. Creaform is a privately-held company based near Quebec City, Canada, with annual sales of approximately $52 million.

LMI acquires 3D3 Solutions

On May 1, 2013, LMI Technologies Inc. signed an agreement to acquire 100 percent of the shares of 3D3 Solutions, a Burnaby, Canada,-based company and a leading supplier of 3D-scanning software and hardware products. The takeover will result in the integration of 3D3 under the LMI Technologies brand to create a powerhouse in 3D-scanning, visualization and measurement solutions for both inline factory automation and offline 3D-scanning markets such as reverse engineering and 3D printing. The terms were not disclosed.

3D Systems acquires Geomagic

On Jan. 3, 2013, 3D Systems announced it had signed a definitive agreement to acquire Geomagic, Inc., a leading global provider of 3D-authoring solutions, including design, sculpt and scan software tools that are used to create 3D content and inspect products throughout the entire design and manufacturing process. This acquisition was subject to customary closing conditions and was expected to close during the first quarter of 2013, after those conditions were met. Terms of the transaction were not disclosed.

(click to enlarge)

FARO Technologies looking to acquire

In the Q3 conference call, FARO Technologies President and CEO Jay Freeland said, "Our cash balance, up 15 percent since Jan. 1, now sits at $182 million. This gives us plenty of flexibility. We continue to look at acquisitions that could enhance our business strategically."

Cognex looking to acquire

In the Q3 conference call, Cognex CEO, President and COO Robert J. Willet said, "The best use of that cash, from our perspective, would be to use it to - in acquisitions. And we have an active program. We are looking at potential entities to buy in different markets, in different geographies." CGNX currently has a cash balance of $217 million.

(click to enlarge)

Google aggressively acquiring technology companies used in robotics

On, Dec. 4, 2013, The New York Times published an article titled, "Google Puts Money on Robots, Using the Man Behind Android." The following excerpt is taken from that article:

Over the last half-year, Google has quietly acquired seven technology companies in an effort to create a new generation of robots. And the engineer heading the effort is Andy Rubin, the man who built Google's Android software into the world's dominant force in smartphones. The company is tight-lipped about its specific plans, but the scale of the investment, which has not been previously disclosed, indicates that this is no cute science project. At least for now, Google's robotics effort is not something aimed at consumers. Instead, the company's expected targets are in manufacturing - like electronics assembly, which is now largely manual - and competing with companies like Amazon in retailing, according to several people with specific knowledge of the project. A realistic case, according to several specialists, would be automating portions of an existing supply chain that stretches from a factory floor to the companies that ship and deliver goods to a consumer's doorstep. "The opportunity is massive," said Andrew McAfee, a principal research scientist at the M.I.T. Center for Digital Business. "There are still people who walk around in factories and pick things up in distribution centers and work in the back rooms of grocery stores."

PRCP specializes in using robotic technology for industrial manufacturers to automate assembly processes, which could make the company a favorable target for Google to acquire.

(click to enlarge)

3D imaging market is expected to grow substantially

Robotics are the future of industrial automation, putting PRCP in a strong position to benefit. A group of Credit Suisse analysts pointed out last year that companies which make and sell industrial-automation technology that both monitors and runs industrial manufacturing processes are an attractive long-term investment target. The $152 billion global industrial-automation market has grown 6 percent a year, on average, since 2003, which is nearly twice as fast as overall industrial production. There is increasing consolidation among makers of automation technology. Companies have been looking to expand horizontally by making products for different types of manufacturing, and vertically, by targeting different levels of manufacturing operations. Thus, the sector has become ripe for mergers and acquisitions. PRCP already has been paving the way toward automating the manufacturing process for automakers.

In our previous article on Cimatron (CIMT), we said CAD/CAM software is essential for the designing and manufacturing of 3D parts. 3D imaging also is essential to the 3D-printing revolution because it enables you to scan a part or physical object and translate the 3D point-cloud data into CAD, where it can be reproduced or modified. Helix, PRCP's newest technology, does just that. The 3D-imaging market is expected to grow as quickly as the 3D-printing market, with both expected to have compounded annual growth rates of around 25 percent.

(click to enlarge)

Source: MarketsandMarkets

(click to enlarge)

Financials

On Aug. 28, 2013, PRCP announced strong fourth-quarter results and record fiscal 2013 sales. The stock jumped from $8 to almost $15 a share. The stock recently has pulled back considerably from its highs, as on Nov. 13, 2013, PRCP announced disappointing results for the first quarter of its fiscal year 2014. According to its recent conference call, PRCP is making progress with Helix sales and bookings and expects to issue the next release of its Vector Software platform within the next 12 months. Also, backlog increased to $35.9 million (a record level), which generally leads to higher sales in future quarters.

With PRCP trading close to its $6.62 book value per share, one would assume the company is a slow growing "Cash Cow." However, over the past five years, PRCP quickly and consistently has been increasing revenues and income, with even a greater future ahead because of technology to be used in two of the fastest-growing industries. In thegrowth-share matrix, PRCP is a "Star."

(click to enlarge)

(click to enlarge)

A peer-group comparison shows PRCP is significantly undervalued

When comparing PRCP to FARO and CGNX, we find PRCP to be severely undervalued in all the valuation measures shown below.

By taking the ratios below and averaging them, we conclude PRCP should be valued at $26.50 per share, which is up around 250 percent from current levels.

(click to enlarge)

PRCP should soon make new highs

With FARO and CGNX making new highs, we believe PRCP will soon follow once investors realize how much the company is undervalued compared to its peers. Here are some yearly charts.

(click to enlarge)

(click to enlarge)

(click to enlarge)

(click to enlarge)

PRCP high cash balance

PRCP has $33 million in cash ($3.69 per share), and that figure is growing. Possible uses for this cash include acquisitions, a stock repurchase or a special dividend, any of which would benefit shareholders and increase the value of the stock.

- On Nov. 30, 2011, PRCP initiated a growth strategy through a combination of organic growth and evaluating the possible acquisition in a synergistic technology-oriented business in a complementary, non-automotive market segment.

- On Sept. 27, 2012, PRCP announced a special dividend of $.25 per share. On May 7, 2013, PRCP announced an annual dividend of $.15 per share. Currently, that is a 1.40-percent yield for shareholders.

- On Oct. 19, 2010, PRCP announced a $5 million stock-repurchase program.

Since the company is currently paying an annual dividend, we believe PRCP's best use of its cash would be the acquisition of a complementary, non-automotive company followed by a stock repurchase program.

Current Risks

In the recent 10-K filing, we found two risks worth noting:

First, PRCP revenues are highly influenced by the sale of products for use in the global automotive market, particularly by manufacturers based in the U.S., China and Western Europe. These manufacturers have experienced periodic downturns in their businesses that could adversely affect their level of purchases of PRCP products. We believe PRCP has technology that can be useful in a variety of industries and hope management will diversify the company's customer base.

Second, PRCP is a party to a suit filed by 3CEMS, a corporation based in the Cayman Islands and the People's Republic of China. The suit was filed on or about July 19, 2013, in U.S. District Court for the Eastern District of Michigan. The suit alleges that PRCP breached its contractual obligations by failing to pay for component parts to be used to manufacture optical video scopes for the company's discontinued commercial-products business unit. 3CEMS alleges that it purchased the component parts in advance of the receipt of orders from PRCP based on instructions 3CEMS claims to have received from PRCP. The suit alleges damages of not less than $4.5 million. PRCP intends to vigorously defend against 3CEMS' claims. The outcome is highly uncertain at this point, but the damages being sought are small compared to PRCP's cash of $32.8 million.

Conclusion

We believe PRCP is undiscovered, which creates a huge opportunity for investors to profit. PRCP should be an attractive acquisition target for a variety of industries, including two of the fastest-growing industries, robotics and 3D printing. PRCP is cheap in valuation despite being a growth company with an even brighter future ahead. Consequently, we assign a buy rating on the stock with a $26.50 price target.

By 3D Analytics

No comments:

Post a Comment