Cellceutix has been overlooked on the market because of its unknown status as a biotechnology company. It trades on the OTC which lacks a lot of coverage, which is part of the reason it is not well known. We believe that upcoming trials along with catalysts/presentations could lead the share price to rise in 2014 as people analyze the true value of the company. We believe that Cellceutix is a good long term stock to own in 2014 and beyond!

Cellceutix has been overlooked on the market because of its unknown status as a biotechnology company. It trades on the OTC which lacks a lot of coverage, which is part of the reason it is not well known. We believe that upcoming trials along with catalysts/presentations could lead the share price to rise in 2014 as people analyze the true value of the company. We believe that Cellceutix is a good long term stock to own in 2014 and beyond!

There are so many biotech companies out there that are looking to create new advances in cancer therapy. There are currently a lot of chemotherapy drugs that leave patients with a lot of toxic side effects. The hope now is to come up with potential treatments for cancer that allow the patient to live a life free of toxicity. One such Company making advances in the clinical oncology area is Cellceutix Corporation(OTCQB:CTIX)

Cellceutix is a biotechnology company that creates small molecule compounds to treat today's cancers, and inflammatory diseases. The company is headquartered in Beverly, Massachusetts and was founded in 2007. The lead drug compound for Cellceutix is Kevetrin, which is being developed to treat patients with various types of cancers.

Lead Drug Compound Kevetrin

Kevetrin is a small molecule compound that has a unique chemical structure compared to other cancer drugs on the market. Kevetrin has been shown to induce the activation of the "p53" gene. This p53 gene is known as "the guardian angel" gene. The reason for being known as the guardian angel gene is, because the p53 gene is known to control the mutations of cancerous cells. The company believes that by controlling the mutations of these cancerous cells, they can inhibit them from multiplying in the human body.

In pre-clinical studies Kevetrin has shown potent anti-tumor activity in multiple cancer cell lines in these xeongraft models

- Lung

- Breast

- Colon

- Prostate

- squamous cell carcinoma

- Leukemia

In a pre-clincial study conducted with Kevetrin on a xeongraft model of head and neck cancer, the drug showed significant improvement for the patient. The delay for tumor growth was increased by around 36 days when Kevetrin was administered with radiation. The delay of the tumor growth was two times greater than placebo control in the trial. This analysis shows just how powerful of a compound Kevetrin is when it is combined with other chemotherapeutic agents.

More pre-clinical results came from in vivo studies of Kevetrin combined with another compound known as sutinib (A multikinase VEGF receptor Agonist). Sutinib was a compound used by Beth Israel Deaconnes Medical Center (BIDMC). Both Cellceutix, and BIDMC entered into an agreement to develop the compound. This study was conducted in patients with drug-resistant renal cancer on cell-line 786. What is interesting to note is that Kevetrin combined with sutinib had for the first time shown tumor shrinkage in drug resistant renal cancer. This first known tumor shrinkage is noted by researchers at BIDMC:

"Research by BIDMC combined Kevetrin™ with sunitinib on cell line 786, a drug-resistant renal cancer. Cellceutix was advised by the researchers that "the Kevetrin/sunitinib combination is the first we've used in which actual tumor shrinkage is noted."

As explained in the above quote the activation "p53" gene in Kevetrin along with sutinib, was able to shrink the tumor effectively. So effectively that Cellceutix contacted BIDMC to conduct further collaboration research on the combination of the two drugs.

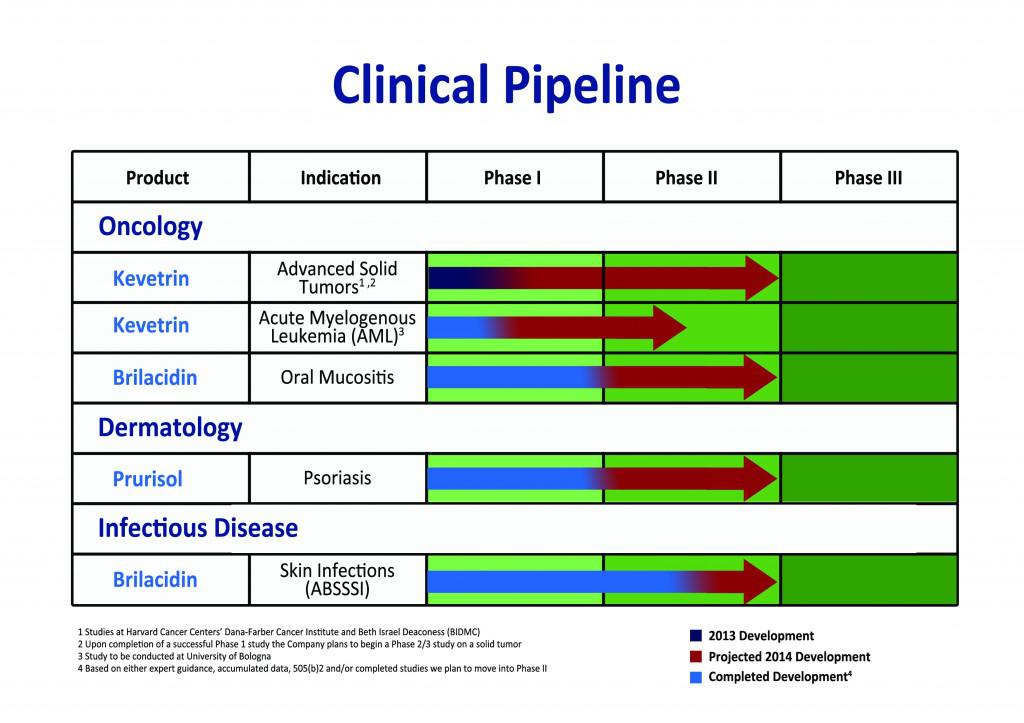

Current Study Of Kevetrin (Phase 1)

Kevetrin is currently being evaluated in a Phase 1 dose escalation study in patients with advanced solid tumors. The phase 1 study has recruited 40 patients, and is being conducted at Harvard Cancer Centers--including The Dana-Farber Cancer Institute.

Some preliminary results for Kevetrin were presented at ASCO (American Society of Clinical Oncology). The preliminary results dealt with the pharmokinetic profile (absorption of the drug by the body) of Kevetrin, along with some evidence of anti-tumor shrinkage. One thing to note about the press release from the ASCO presentation comes from this quote:

"The trial, which is currently in the fourth cohort, is progressing with data to date on par with our laboratory studies," commented Dr. Krishna Menon, Chief Scientific Officer at Cellceutix. "Through three completed cohorts, we have seen no signs of dose limiting toxicity. Dana-Farber's extensive tumor mapping technologies will help us pinpoint which patients will benefit the most from Kevetrin as we move towards defining the Maximum Tolerated Dose. We are very pleased with the results so far and believe that as dose escalation continues, the potential therapeutic benefits will rise significantly.

As noted in the above quote the Chief Scientific officer states that Kevetrin had been showing great preliminary results even though the maximum tolerated dose (MTD) had not even been reached yet. As of ASCO 3 doses had been completed. Although Cellceutix is currently treating patients with the 6th dose of the escalation study. The company expects to eventually reach a 9th or 10th escalated dose to conclude the study. The fact that Kevetrin has already shown such great clinical activity at the lower doses bodes well once patients can be treated with the highest dose possible. The way the company is determining the maximum tolerated dose is by their collaboration with the Dana-Farber Cancer Institute. The Dana-Farber Cancer Institute has highly sophisticated data imaging machines that can show how patients are reacting to higher level doses of Kevetrin. What is also being monitored is the potential biomarker activation of another gene known as "p21".

Just recently Cellceutix announced that it has established a safety committee to come together by mid December to determine the 7th tolerated dose for patients with advanced solid tumors. The company has also filed with the FDA for the ability to limit the dosing duration of Kevetrin to around 6 hours. The company is doing this, because it is increasing the doses for Kevetrin substantially.

Kevetrin Pre-Clinical Activiity In Retinoblastoma

Cellceutix is targeting advanced solid tumors as its first indication but it is not afraid of going up against unmet medical needs. One such unmet medical need being looked at to be treated with Kevetrin is retinoblastoma. Retinoblastoma is eye cancer in children that are under the age of 5 years old. The children that suffer from this disease have limited treatment options that produce too much toxicity. Such treatments include: Removal of the eye, radiation, and chemotherapy. Even then these treatments they are sometimes not effective enough causing further problems along the way. Below is a picture that shows a trial of Kevetrin conducted in mice with retinoblastoma.

The picture shown above was a pre-clinical trial for Kevetrin targeting the retinoblastoma human cells in nude mice. In order for the company to go after retinoblastoma it has to target the (Weri-Rb-1 gene). This is because the Rb1 gene is overexpressed in children with retinoblastoma, and the company had shown that kevetrin was able to reduce the tumor size by 50% or more. As you can see above the clarity of the eyes in the mouse that was given Kevetrin was substantially superior than the mouse in the placebo group above, that was only given control. Furthermore the Kevetrin compound showed continuous improvement even at day 35 of the trial, while placebo started to deteriorate at the same time point.

In our analysis we believe that the company should target retinoblastoma, because it would be eligible for a lot of leniency by the FDA in terms of regulations. Since retinoblastoma is an unmet medical need, Cellceutix could possibly achieve a number of certain advantages depending upon upcoming data. Such advantages would include orphan status, Fast Track, and Breakthrough. This trial is dependent upon the completion of the current phase 1 trial with Kevetrin in Solid tumors. If Kevetrin shows remarkable progress in the final dose of the phase 1 cohort, then the company should have no problem expanding upon further research against retinoblastoma.

Planned Trials/Catalysts For Kevetrin in 2014

- Phase 2 trial to evaluate Kevetrin with Cytarabine (Nucleoside Metaboloic Inhibitor) in patients with AML (Acute Myeloid Leukemia) at the University of Bologna, Italy

- Phase 2 trial in Drug-resistant Renal Cancer (cell lines 786)

- Phase 2 clinical Trial Solid Tumors (Kevetrin is awaiting to see Maximum Tolerated Dose-MTD in Phase 1)

Aileron's Deal With Roche (OTCQX:RHHBY)

Cellceutix isn't the only biotechnology company that wants to target the "guardian angel gene" p53. Aileron is another biotech company that wants to garner technology to target the p53 gene. Thus far though Aileron is only in pre-clinical work on their compound. The compound from Aileron uses stapled peptides, which are a collection of protein fragments. A completely different technological approach than the Kevetrin compound. The key belief for Aileron is that it expects the stapled peptides to travel freely through the human body without being degraded by enzymes. The company expects the drug to activate the p53 pathway. Aileron doesn't expect to begin human testing with its "p53" compound until the first half of 2014.

Aileron was able to make a deal with a big pharmaceutical company known as Roche in a $1.1 billion dollar deal. Roche will fund at least $25 million dollars for the research of Aileron's drug, and Aileron will be eligible to receive $1.1 billion dollars in milestones payments. Ironically the founders of Aileron -- Stanley Korsmeyer and Loren Walensky-- were a pair of biologists from Dana-Farber Cancer institute. One of the other founders Gregory Verdine was a Harvard University Chemist.

Cellceutix Is Not A One Hit Wonder

Cellceutix is pursing a phase 2 trial with a drug known as Prurisol. Prurisol is being developed to target a disease known as Psoriasis, which is a disease that causes skin redness and irritation. Before the company could begin the phase 2 trial with Prurisol, it hato conduct a short phase 1 trial requested by the FDA. Cellceutix has to also wait for a report from Dr. Reddy's Lab (RDY) before it could begin its phase 2 trial with Prurisol. Currently the company is in the process of choosing the site in which it will conduct this short phase 1 study. Afterwards the company must send the protocol to sites of the Institutional Review Board (IRB) for approval. The good news about this short phase 1 trial is that is expected to take only one month to complete.

In a preclinical trial in xenograft human models in mice, Prurisol showed significant efficacy in treating Psoriasis. The trial design was setup for 3 different factors: One was the oral version of Celldcutix's drug Prurisol, a control group (no treatment given at all), and methotrexate. Methotrexate is an antimetabolite drug, that is used currently for Psoriasis, and certain cancers such as breast cancer. It is known for the metabolism functions of cells which can control the production, and destruction of cells. Since Psoriais deals with rapidly fast production of cell growth, it is prudent for patients to receive methotrexate to treat their disease. The problem though is that methotrexate at high concentration levels can lead to many problems in the body, including kidney failure. Below is the first graph that shows the skin appearance in the trial.

The above graph shows the comparison of the 3 controls within the trial. The graph shows 0 as being the ability to clear the Psoriasis completely, while the 10 indicates a very high level of Psoriasis respectively. The graph on the left was the skin appearance in itself, while the graph on the right is the skin histology data (the data within the skin itself). As you can see above the control (untreated) group was nearly a 10 indicating the highest level of Psoriasis. Methotrexate fared well against the 10mg dose KM-133 once a day. Despite this though KM-133 taken twice a day achieved an even greater skin appearance than the Methotrexate placebo group.

This graph above shows once again the comparison of the 3 controls within the trial but does so in a different manner. This data deals with PRINS--RNA measurement of Psoriatic lesions, and IL-20-- measurement of blood levels in patients with psoriasis. Once again the KM-133 2X doses fared better in the PRINS psoriasis data, and the IL-20 blood levels data. A key thing to note is that even by giving patients a double dose of the KM-133 drug, there was hardly any toxicity observed. The Prurisol drug was able to do better against the control group on eat metric posted above.

It would be great for Cellceutix to get a drug out there to help patients with Psoriasis as it is desperately needed. As I mentioned earlier Methotrexate works slightly in terms of efficacy but it has many toxic side effects. The addressable market for patients with Psoriasis is very huge. There is a huge market opportunity as Psoriasis effects 7.5 million people worldwide.

Acquisition Of Assets From PolyMedix (OTC:PYMX)

On September of this year Cellceutix announced the acquisition of assets from PolyMedix. PolyMedix was a clinical stage biotechnology company developing small molecules for the purpose of treating immunity disorders, and infectious diseases. PolyMedix had trouble with financials, and on April 1, 2013 the company had announced Chapter 7 bankruptcy protection. Well the executive management of Cellceutix didn't waste anytime, because it filed a "stalking horse" bid for PolyMedix around August of this year. A "stalking horse" bid was made by Cellcuetix so that it could set the bar for the price it believed the assets were worth. This way other competing companies couldn't come in, and make offers at a much lower price. The management had apparently done some good due diligence, because they were able to acquire the assets at great value. To receive the assets of PolyMedix Cellceutix had to pay $2.1 million dollars in cash, and give away 1.4 millions shares of its common stock. This deal was substantial because it not only enhanced Cellceutix's pipeline, but they also got a 25,000 sq ft. laboratory to go along with it.

The main part of the acquisition had to do with the company getting an antibacterial drug known as Brilacidin. Brilacidin is a first-in-class defensin memetic antibiotic. What makes it a good purchase is the fact that it has already proven to be better than Cubist Pharmaceutical's (CBST) Cubicin. In a phase 2a trial testing patients with acute bacterial skin and skin structure infections--ABSSSI--Brilacidin was shown to hit its primary endpoint, and achieve better efficacy than its control arm with Cubicin. With the acquisition of PolyMedix the CEO LEO Ehrlich had this to say in aquote:

"This is a transformational development for our Company and shareholders; adding the assets of PolyMedix for a tiny fraction of what we believe the company is truly worth," said Leo Ehrlich, Chief Executive Officer at Cellceutix. "We are very excited about instantly having a strong antibiotic franchise to complement our already robust pipeline that now contains 18 compounds. We intend to quickly advance Brilacidin into a Phase 2b clinical trial, a drug that we believe could one day compete with drugs like Pfizer's Zyvox, which generated $1.35 billion in sales in 2012. The acquisition, which includes laboratory equipment and other furnishings that we are confident cost in excess of $1 million, makes us an even more formidable company. "

In the quote above the CEO talks about the acquisition of Brilacidin, and how good it is for the company. In our analysis we can see that Brilacidin can advance to a phase 2b trial, and possibly create a surge in the share price because of the potential market value for a drug of this caliber. The antibacterial market is expected to exceed $46 billion dollars by the year 2015. So an acquisition like this for $2.1 million dollars and exchange for stock seems like a very small price to pay. Also in the quote above Cellceutix talks about being able to compete against heavy hitter antibiotic drugs like Zyvox from Pfizer Inc. (PFE).

Phase 2b Trial Brilacidin

There are 2 key catalysts for the Brilacidin compound

- Brilacidin ABSSSI - initiate phase 2B clinical trial Q1 2014

- Brilacidin OM (Oral Mucositis) initiate phase 2 trial Q2 2014

Brilacidin had gone through a preliminary phase 2 trial which was done in Canada and Europe (Russia & Ukraine). This trial was done prior to the acquisition of PolyMedix assets. The trial had enrolled 215 patients, and had tested 3 various doses among the patients. The end result of this phase 2 trial was that the efficacy was substantial enough to merit further investigation.

This takes us to two phase 2 trials using Brilacidin against bacterial diseases that will be launched in 2014.

| Trial | Patients | Dosage | Endpoint |

| Phase 2 | 100~200 | 3 days 1.2mg, 1 day 0.6mg, 1 day 0.8mg (All doses are followed up with extra days of once daily placebo drugs after initial treatment) | 95% confidence interval |

| Trial | Patients |

| Phase 2 Proof Of Concept (POC) | 60~120 |

| Phase 3 | 240 |

Management

There is a vast amount of people that compose the management team at Cellceutix, but I will discuss two of whom we believe will drive value for the company going forward.

The first member of management is Leo Ehrlich, who is CPA, CEO, CFO, and on the board of Directors for Cellceutix. He co-founded Cellceutix back in 2007. Leo has 14 years of experience in publicly traded companies. He was the former founder, Director, and CFO of NanoViricides, Inc. which trades on the NASDAQ under ticker symbol (NNVC).

The second member of management that will bring value for the company going forward is Krishna Menon. Krishna Menon is President, CSO, and Board of Directors of Cellceutix. He also co-founded Cellceutix back in 2007. He has had 30 years in the developmental biotech industry, and has had a very successful career thus far. Interesting note is that he is the Research Scientist at Dana-Farber Cancer Institute. Which is the same place where Kevetrin trials are currently being conducted at. This man has already achieved great success, because he was responsible for the development of Gemzar, and Alimta at Eli Lily (LLY).

Financials

Cellceutix is a small-cap biotech stock developing small molecules, and has to go through all clinical trials for regulatory approval. As such, there is no current revenue stream that the company will be able to receive to offset for all incurred expenses. As stated in the 10q-SEC filing the company has incurred debt along the way starting from June 20, 2007 all the way to now. The amount of debt incurred during this period has been a deficit of $20.8 million and working deficit capital of $4.77 million. As such the company will have to continue to make its progress in the pipeline for Kevetrin, Prurisol, and Brilacidin. These trials may be able to produce partnerships, which could possibly bring in finance by big pharmaceutical partners. These partnerships could then increase the funds that will be necessary to take the molecules to later stage trials. On October 28, 2013 Cellceutix had made an agreement for Aspire Capital to purchase $20 million dollars of its common stock. The catch though is that Aspire Capital will be buying these shares over the next three years. Still this is a great deal as Cellceutix can use the proceeds to fund all their clinical trials, and pay off some debt. One thing to note is that this isn't the first deal with Aspire capital for Cellceutix to receive cash. A closely similar deal went down back on December of 2012 in which Aspire agreed to purchase $10 million worth of Cellceutix shares. In the most recent deal though, Aspire is set to purchase the shares on the open market. This means that as the pipeline progresses with a rise in share price, Aspire Capital will be buying at higher prices. The buying of shares from Cellceutix at higher prices, should provide a higher cushion of funds for Cellceutix going forward. As an example of how praised the management team is, here is a quote from one of the Managing members of Aspire Capital:

"Cellceutix has continued to impress us with the strength of its pipeline and the savvy business sense of the management team," commented Steven G. Martin, Managing Member of Aspire Capital. "Cellceutix's acquisition of the assets of PolyMedix in September came at what we consider an incredibly low purchase price, one that we feel has yet to be fully factored into the Company's valuation. The timing was right for us to increase our commitment to and investment in Cellceutix as we believe 2014 will represent a transformational year for the Company."

As I mentioned above the management team is savvy and capable of creating excellent shareholder value. Aspire Capital itself even believes that 2014 will be a tansformational year for Cellceutix, and they were willing to put down more capital for the company to prove it. As of September 30, 2014 Cellceutix had $4.6 million dollars, but the deal with Aspire Capital has allowed Cellceutix an additional $9.9 million dollars. Unfortunately even with the Aspire deal, Cellceutix won't have sufficient cash reserves to fund the clinical trials for long. Matter in fact the company has enough funds to take its trials all the way up to June of 2014. Thus the company will have to sell more shares on the open market to keep clinical trials progressing, or it will have to form some partnership for its compounds to release the burden of huge expenses.

Risks

As we look at it there are a few risks that the company will have to deal with in the coming years, and beyond. Here are some of the risks that the company will have to deal with:

- Compounds currently show results in Preclinical and Phase 1 trials, which means later stage trials in bigger patient populations may not be sufficient enough in terms of efficacy

- Kevetrin is currently being evaluated to be tested at a 6th dose level, and management expect to be able to reach at least the 10th dosage level. The risk here is that there is a possibility that doses given above the 6th dose, may produce high levels of toxicity. This would force phase 2 trials to go the next step with a lower dose, and may not provide enough efficacy for kevetrin to move into later stage trials

- Prurisol has a short trial to conduct before it can being its phase 2 trial with the compound. The problem is that it has to see if safety can be met, and if the company's ISB board agrees to approve the phase 2 trial. As with other biotech companies safety is important, so the preliminary trial will determine Prurisol's future.

- Brilacidin has already shown greater efficacy than Cubicin from Cubist Pharmaceuticals, but it still has to conduct a large phase 2 trial to determine its efficacy in a large patient population. Even with Prurisol achieving its primary endpoints in the phase 2 study, it will have to conduct a larger phase 3 study then seek FDA approval

- As a small cap biotechnology company with limited resources of working capital, Cellceutix will have to continue to sell its shares of common stock on the open market to have enough funds to operate its clinical trials

- Stocks that trade on the OTC carry more risks, and as such investors should be cautioned

- Short Term trading may be sporadic, so considering investing with a long term frame of mind as the clinical trials progress to later stages

- FDA approval is dependent upon how the safety of the trials turn out, along with greater efficacy. There is no guarantee that the trials will produce sufficient clinical outcome in advanced trials

- Kevetrin is targeting a gene "p53" which many other biotechs have tried and failed in the past. Successful outcome of Kevetrin would be a breakthrough for patients, and the medical industry

- Not enough cash reserves. Cellceutix will have to dilute shareholders, or form partnerships to allow clinical trials to move forward before June 2014

Conclusion

Cellceutix is an undiscovered biotechnology company that we believe is currently undervalued for its potential. Significant catalysts in 2014, could lead the share price to rise higher as the clinical trials advance. One of the lead compounds Kevetrin is important for the company as achieving sufficient clinical activity in the p53 gene (known as the guardian angel gene) would be a first in medical history. Kevetrin showing positive results along with other catalysts in 2014 could lead Cellceutix to gain 100% in share price from its current level at $1.84 per share. This increase in share price would give the company a market cap of $400 million, which would be more in line for the true value of the company with its current pipeline.

Additional disclosure: I have no position in other stocks mentioned

By Long Term Bio

No comments:

Post a Comment