What was the result of all of this fear? Two things, first, bond rates shot up - well kind of… As the chart below shows, 10 year Treasury bond rates rocketed upwards to their highest rates since May of 2012. Oh the horror! Now of course, the chart also shows that such moves haven't been unusual in the last few years, and that there is a fairly good chance the spike in rates will be reversed.

(click to enlarge)

In summary, investors in stocks from Duke Energy (DUK) to AT&T (T) are probably feeling nervous now given the rapid fall in prices over the last few weeks. And it's true that these stocks may face more pain in the near-term if investors continue to pile out at a breakneck pace. However, in the longer run, dividend stocks have tended to outperform growth stocks, and the recent sell-off provides an enormous opportunity for retail investors who missed the rally over the last few months. Stocks can't go up forever, but they can keep paying dividends to patient investors year in and year out who are willing to ignore the market's madness.

So all things considered, the bond markets are acting rationally. A small possibility of less Fed buying should lead to a small increase in rates. Fair enough. The stock market though seems to have utterly lost its mind over this - at least as it pertains to dividend stocks.

Here is the chart for one of the quintessential dividend paying sectors, mortgage REITs (MORT). Looking at chart, mREITs have fallen 15% since the start of May. The market seems to think that these stocks are in for a very difficult future almost immediately, all based on the supposition that there is a very small chance of slightly early action by the Fed.

(click to enlarge)

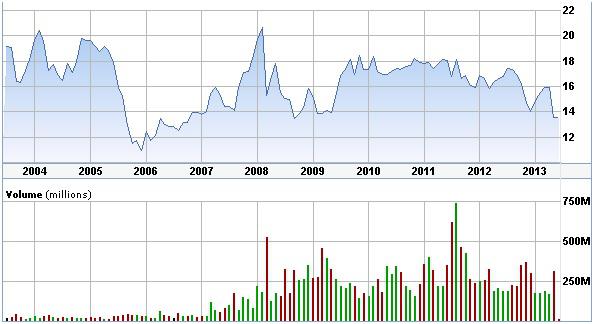

Now, bears in the mREIT space might say that mREITs are just getting back to normal - the way things were pre-2008. They say that mREITs have a dim future ahead and that the firms will make little to no money once rates start to rise. That theory is easy to test though. Let's look back at the historical stock price for one of the biggest and most prominent mREITs out there, Annaly (NLY). (Note: we can't look at MORT's chart because its history doesn't go back far enough.)

(click to enlarge)

The chart shows that NLY apparently did just fine during the mid-2000s, and there is no reason to think anything different would happen in the future as rates start to rise. With an 13.3% yield, NLY should look pretty good to investors willing to wait for the market to regain its sanity.

Yet mREITs aren't the only proverbial baby that the market has thrown out with the bathwater. The market has also gone crazy on high yield debt ETFs and CEFs. Take one of my favorite CEFs, the Nuveen Diversified Income Fund (JDD). In the last 30 days, the market has driven JDD down by about 12% in price. With a price decline like that, the market must be concerned that rates are about to rise and destroy the stock because JDD has probably bought junk bonds with yields that are too low, right? Of course, if this were true, then that would imply that JDD's yields must be very low right now. Yet, the CEF has a yield of 8.08%, and it has actually managed to increase its dividend since the recession began from $0.10-$0.12 per quarter before the recession to about $0.25 cent per quarter today.

So, perhaps the market is concerned that conditions will reverse and JDD and other CEFs will be forced to go back to paying lower dividends like they did in the mid-2000s? Yet if this were the case, shouldn't stocks like Credit Suisse Asset Management (CIK) which paid more in the mid-2000s than it does today, be rising? Instead, CIK has fallen 8% in roughly 2 weeks, so that it now yields a healthy 7.12%.

Yet, the madness doesn't end there. Business Development Companies which make most of their money lending cash to middle market companies and taking debt or equity from those companies have also seen their stocks decline. From American Capital (ACAS) and Prospect Capital (PSEC) to Blackrock Kelso (BKCC) and TICC Capital (TICC), the sector has been getting crushed of late such that most of these firms now sport yields anywhere from 10-15%. BKCC, for example, has recently seen its stock fall 8%. Yet if the economy gets better, and the Fed stops buying so many bonds, shouldn't that help these business development companies, which after all, are in the business of investing in small companies? Small companies do better during an economic expansion after all?

Now despite the temptation of these high yields and the price falls that have made them available to many investors, some will still say that there are issues with all of these companies. The assets are too risky, and the durations on the fixed income products they hold are too long, which will lead to severe price declines. Yet, if this were true, there should be one investment sector that is only marginally affected - municipal bonds. Muni bond funds carry super-safe assets since muni bonds rarely default (see my article here), and since they hold a variety of bond maturities, their durations are relatively short.

So how have muni funds been doing of late?

Terribly, as the chart below of one of my favorite muni CEFs shows. The Nuveen Municipal Opportunity Fund (NMO) has fallen 13% in the last couple of months, so that it now yields a tax-free 5.79% (equivalent to 8.64% before tax yield at the top statutory rate).

(click to enlarge)

Investments don't come much safer than this - even with a enormous 1% rise in interest rates - based on NMO's portfolio leveraged-adjusted duration of 12.2, NMO's bonds would only fall in value by 12.2%. Now a 1% rate hike would be an enormous change in rates, and even with this rate hike, assuming it took place over the next year, NMO's portfolio would only fall in value by 8.4%. Yet the stock has fallen by 13%. This is an insane move for a CEF which actually earned better yields in the mid-2000s than it does today.

NMO and other muni CEFs will ultimately benefit from a rise in rates, yet the market is crushing its stock like rates are about to rise tomorrow and annihilate the fund's portfolio.

Finally, perhaps nothing illustrates the fact that the stock market has lost its mind like the change in stock price on Eaton Vane closed end funds (EFR) and (EFT). These have both fallen by roughly 7-8% in the last two weeks leading to yields of about 6.3%. Why is this so crazy? EFR and EFT invest in floating rate debt, principally through floating rate bank loans to large companies. These two will both directly and immediately benefit from any increase in rates. Yet, just like all of the other investments I have mentioned above, the market has decided that it is time to sell anything that carries a dividend.

Source: www.seekingalpha.com

No comments:

Post a Comment