Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Intelligent investors must recognize that REIT dividends are regarded as a "holy grail" of sorts, and unlike ordinary stocks, REITs must pay out at least 90% of taxable income in the form of dividends. That is especially important to recognize in uncertain times when a dividend is often regarded as more important than the market price of the shares.

I often argue that REITs should be a core asset class (as opposed to an alternative) simply because of the dramatic shortage of quality yield in the marketplace. My biased attraction is driven by the fact that REITs have a highly efficient structure of paying out consistent and reliable dividend income. In addition, real estate is one of the few gems that can protect your portfolio from the effects of inflation.

Another way investors can protect against market fluctuations is to select sound REIT securities that provide an adequate "margin of safety" (the difference between the real or intrinsic value of the business underlying the security and the price assigned to that security at the moment). In other words, investing in REITs can be an excellent way to diversify your portfolio, but if you don't buy the shares at a favorable price, you could be exposed to the danger of risking capital. The legendary investor Benjamin Graham said it best (The Intelligent Investor):

We all know that if we follow the speculative crowd we are going to lose money in the long run.STAG Has Had an Incredible Run

Back in November 2011 I wrote an article on STAG Industrial, Inc. (STAG) just a few months after the company had closed on its IPO. At the time of the IPO, STAG generated around $205 million (in gross proceeds) that was capitalized with 13,750,000 shares of common stock priced at $13 per share. I recommended shares in the new Industrial REIT at $10.04 per share.

Boy, I like it when I'm right! STAG has had an amazing run. Check out the chart below. Since my article (in November 2011) STAG shares have increased by a whopping 131.5%.

(click to enlarge)

More

extraordinarily, STAG has returned over 157% (since November 2011):

More

extraordinarily, STAG has returned over 157% (since November 2011):(click to enlarge)

STAG has been an amazing REIT (and I wish I would've owned it) and I admire the investors who took the chance to purchase the shares because that courageous act has now turned into a great reward. But maybe it's beginners' luck? Perhaps STAG is just riding the waves and soon Mr. Market will find out that STAG is just riding on air? It's time to re-evaluate STAG and determine if this REIT is sound… Ben Graham explained:

An investment operation is one which, upon thorough analysis, promises safety of principal and satisfactory return. Operations not meeting these requirements are speculative.

What is a STAG?

STAG (Single Tenant Acquisition Group) is an Industrial sector REIT that has built its differentiated model on investing in Class B properties that generate higher current returns relative to Class A properties. Unlike other REITs and Industrial buyers fighting to gain stakes in primary markets with trophy assets, STAG has built its competitive moat on acquiring properties in smaller markets where there is less competition and higher yield.

By focusing on smaller deal sizes (and small markets), STAG's competition is typically smaller and poorly capitalized. Consequently, having limited competition (from larger investors) has made STAG somewhat of a big fish in a small pond.

One of the benefits of being a "big fish in a small pond" is the fact that the properties that STAG acquires are risk-adjusted, meaning that there is a more substantial cap rate differentiation (or arbitrage) between pricing in primary and secondary markets. On average STAG acquires properties at cap rates of around 9% and that allows STAG to capture significantly attractive risk-adjusted returns.

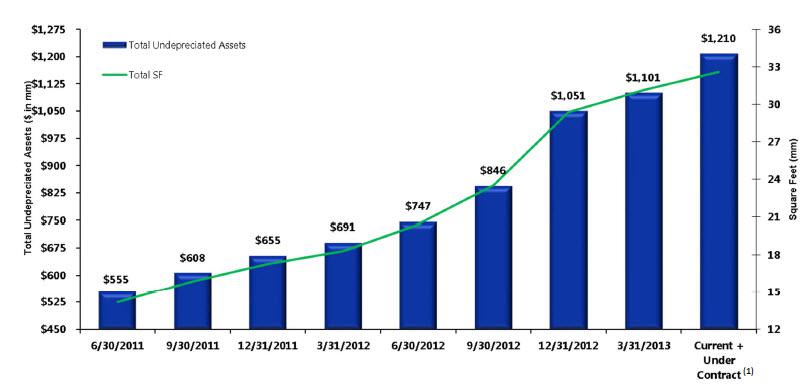

Since the IPO, STAG's assets have increased from around $555 million to around $1.2 billion and revenues have grown from around $47.1 million (2011) to around $85 million (2012).

(click to enlarge)

Compared

with its peer group, STAG has acquired more assets (on a net basis) since going

public in Q2-11. Here is a snapshot of STAG's acquisitions from Q3-11 through

Q1-13 ($ in min):

Compared

with its peer group, STAG has acquired more assets (on a net basis) since going

public in Q2-11. Here is a snapshot of STAG's acquisitions from Q3-11 through

Q1-13 ($ in min):

Here is a snapshot of STAG's acquisitions as a % of Total Assets:

STAG Has Become Much More Diversified

STAG's portfolio has grown considerably since the IPO and so has increased its geographic diversification:

Here is a map illustrating STAG's increased nationwide footprint - now in 33 states:

In addition, STAG's revenue has become more diverse based upon the increased number of tenant categories.

STAG's largest tenant, International Paper (IP) now represents less than 2.6% of the annual base revenue and STAG's second largest tenant, Bank of America (BAC), has less than 2.1% of ABR.

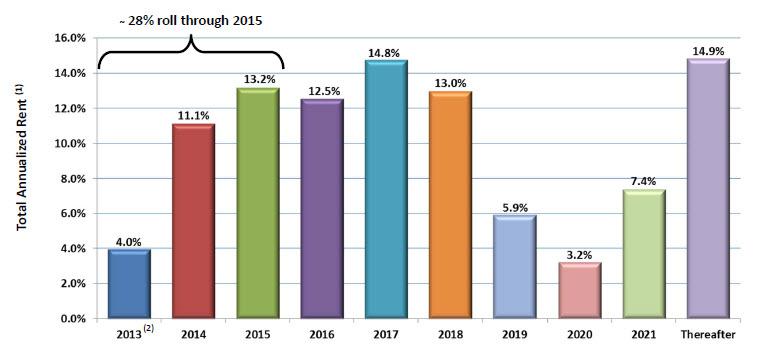

STAG's diversified tenant portfolio has created a very predictable cash flow model driven by low rollover leases with high tenant retention. As illustrated by the snapshot below, STAG has around 28% rollover through 2015 (as compared to peer average rollover of approximately 46%). Also, STAG had a 100% tenant retention rate in Q1-13.

(click to enlarge)

STAG Is Moving Away From Its Small-Cap Pond

STAG continues to operate a conservative capital structure that consists of common shares ($1.03 billion), mortgage debt ($229 million), unsecured term loans ($175 million), and preferred issues. With a total capitalization of around $1.53 billion, STAG is gaining favor with many more institutional investors.

STAG has a manageable debt maturity schedule with no debt maturities until 2016.

STAG has an attractive, fully-covered dividend (increased by 11% in Q1-13) and the AFFO (in Q1-13) payout ratio was 94%. Also, STAG's debt to annualized adjusted EBITDA is 4.7x (as of Q1-13).

STAG has considerably improved its debt profile as evidenced by its modest secured debt of 23%. Also, STAG's fixed charge coverage of 3.1x and total debt to total capitalization of 28% are evidence that STAG has become a true player in the REIT sector.

During STAG's recent earnings call, Michael Salinsky with RBC Capital Markets asked the following:

What are you hearing from the rating agencies and what size do you need to get to get on that investment grade rating?Greg Sullivan, CFO of STAG, replied:

We've had some preliminary discussions with one of the agencies. They seem pretty positive in terms of our various credit statistics. The size often can be an issue, I know that typically Moody's and S&P size of a couple of billion dollars in book value of assets is pretty important as well your tenure as a public company. Fitch, I think is probably a little more focused on the quality and strength of your credit metrics. So I think it varies a bit agency to agency. But if you sort of look at our credit stats in the vacuum, it would certainly look like they were reasonably consistent with the lower end of an investment grade rating, although they are other factor that the agencies review as well.Also, Ben Butcher, STAG's CEO, responded:

So we've got a lot of pressure on us currently to have an investment grade rating, we have any rating for that matter. But it's something we certainly are looking at and are working on. And as we go through the coming months, we will definitely focus on.STAG has shown us over the past few quarters that it can manage its balance sheet, and with a healthy debt to enterprise value of 28%, STAG is in excellent position to get rating agency favor. In terms of liquidity, at the end of the quarter, STAG had about $13 million of cash, about $225 million of debt capacity under its revolving credit facility that provides about $400 million of purchasing power running at about 40% leverage.

STAG also did another follow-on equity offering in January that raised $115 million of gross proceeds. Subsequent to quarter end, STAG sold $70 million of 6.625 perpetual preferred shares that was used to fully repay the outstanding balance on the revolving credit facility and to fund acquisitions.

STAG Has a Well-Defined Model Aimed at Repeatability

STAG has around 28% of its leases expiring through 2015, and during the latest quarter, the company's occupancy rate was around 95.4% (it was 95.1% in 2012 and 93.2% in 2011).

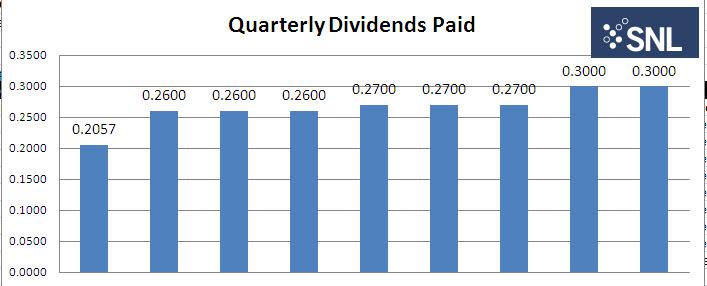

Since going public STAG has announced 9 quarterly dividends with the latest to be paid on July 15th ($0.3000 per share). STAG has demonstrated a track record of increasing dividends every year.

(click to enlarge)

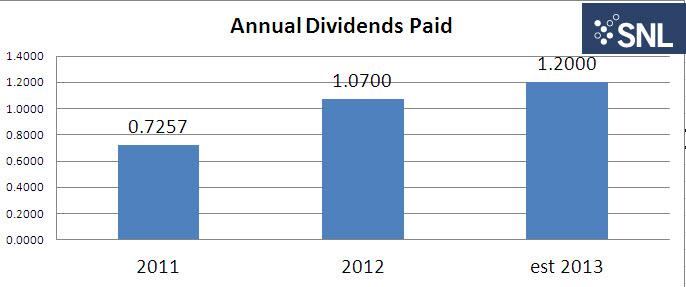

STAG's annual dividend has increased, and in the first quarter of this year (2013) the company increased its dividend by 11%.

(click to enlarge)

Driven

by strong cash NOI growth of over 69% (over the first quarter of 2012), STAG has

proven that it has considerable capacity to grow externally. This growth was

driven primarily by STAG's healthy acquisition activity as evidenced by core FFO

growth of 118% over first quarter of 2012.

Driven

by strong cash NOI growth of over 69% (over the first quarter of 2012), STAG has

proven that it has considerable capacity to grow externally. This growth was

driven primarily by STAG's healthy acquisition activity as evidenced by core FFO

growth of 118% over first quarter of 2012.STAG's current dividend yield is 5.09%, and as mentioned above, STAG increased its dividend by 11% in the first quarter. Because of STAG's ongoing high positive spreads between its growing cap rates and its financing rates, the existing portfolio was able to generate a dividend yield that is roughly twice the average REIT dividend. Here is a snapshot that illustrates that differentiation (note: I also included several Triple-Net REITs for comparison):

(click to enlarge)

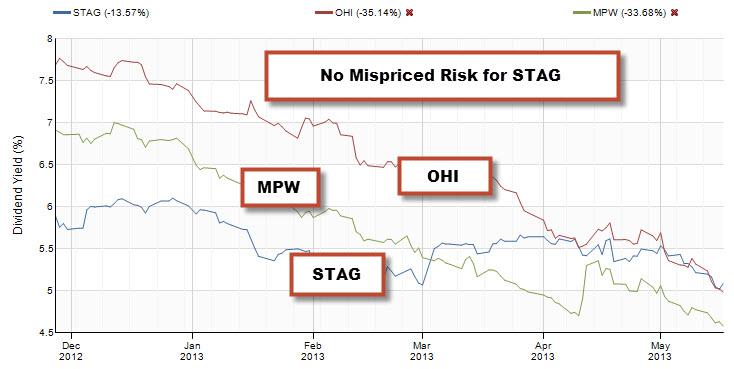

In

In a previous article, I wrote about several healthcare REITs with mispriced

risk. Essentially, my argument was based on the notion that several equity REITs

are experiencing significantly higher dividend compression when cap rates aren't

compressing at the same pace. That really applies more to properties that are

lower in credit quality or assets that are located in secondary markets. To

illustrate that concept I decided to compare STAG with Omega Healthcare

Investors (OHI) and

Medical Property Trust (MPW). Like

STAG, these two REITs invest in secondary markets with cap rates in the 8% to 9%

range.

In

In a previous article, I wrote about several healthcare REITs with mispriced

risk. Essentially, my argument was based on the notion that several equity REITs

are experiencing significantly higher dividend compression when cap rates aren't

compressing at the same pace. That really applies more to properties that are

lower in credit quality or assets that are located in secondary markets. To

illustrate that concept I decided to compare STAG with Omega Healthcare

Investors (OHI) and

Medical Property Trust (MPW). Like

STAG, these two REITs invest in secondary markets with cap rates in the 8% to 9%

range.(click to enlarge)

Clearly, you can see that STAG's dividend yield (since November 2012) is less compressed (13.57%) than the others mentioned (OHI compressed 35.14% and MPW compressed 33.68%). That tells me that STAG does not suffer from the same mispriced risk relative to its dividend performance.

Is STAG Worth Buying Today?

STAG's primary investment strategy focuses on what is perceived to be efficiencies in the pricing of its target properties. In other words, STAG looks for an adequate "margin of safety" when it acquires Class B assets in secondary markets.

So, that same theory applies to REIT investors. Can we buy STAG today at a moderate price and hope to continue to earn outsized returns?

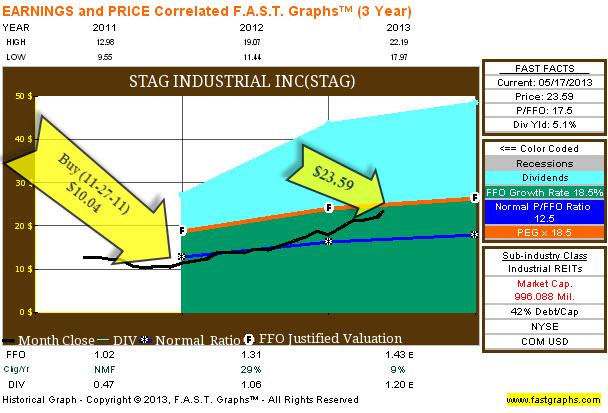

First off, STAG common shares are trading at $23.59 per share with a P/FFO multiple of 20.3x (note FAST Graphs P/FFO is more closely aligned with AFFO).

(click to enlarge)

The above FAST Graph clearly illustrates STAG's trending dividend performance (the shaded aqua area) as well as its impressive stock growth (the shaded dark green area). Also, the price (the black line) is still below the intrinsic value (or FFO) line (orange line with "F"). That's a good indicator that STAG is trading at fair value levels.

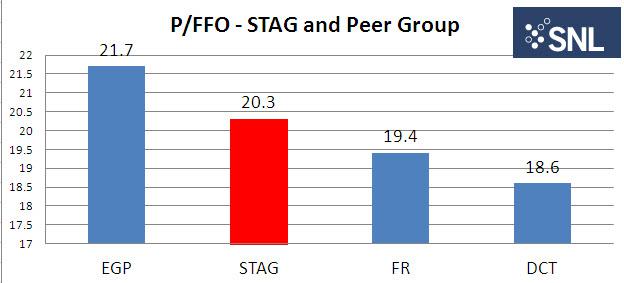

Now let's compare STAG's P/FFO valuation with the peer group. As illustrated below, STAG is not as cheap as it was last year; however, the dividend yield (5.09%) is still attractive compared with the alternatives.

(click to enlarge)

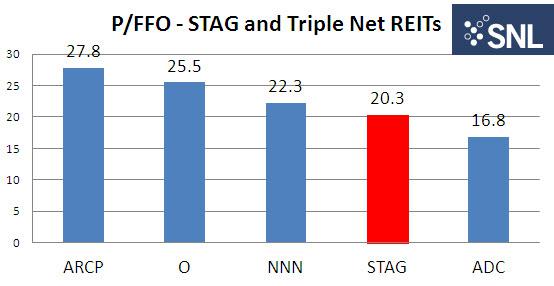

Now let's compare STAG's P/FFO multiple with the "kissing cousins" also known as the Triple Net REITs. As illustrated below, you can see that STAG does not have the higher valuations of the higher quality cousins; however, STAG also doesn't enjoy the same long-term lease safety that the Triple Net REITs enjoy. STAG's average lease term is five years while the average lease term for Realty Income is just under eleven years.

(click to enlarge)

Recognize that STAG owns larger buildings (average of 175,000 square feet) while Realty Income and National Retail are more diverse across industries, and because the majority of the facilities are smaller, these Triple Net REITs have a higher degree of safety with regard to re-tenanting or selling the vacant properties.

More importantly, STAG is just around two years old (as a public company) and the company does not have a credit rating (yet), while Realty Income and National Retail have an extraordinary track record for paying dividends and both have investment grade credit ratings.

It is also worth noting that STAG's value proposition is much different from most peers (as well as the Triple Net REITs) since STAG invests in facilities where rents are generally below market. That differentiated investment strategy is aimed to generate higher returns in second tier markets where there is decreased occupancy and rent volatility. In other words, STAG's risk-averse model is built on a market niche differentiation that has resulted in an increasingly consistent and highly profitable (accretive) growth strategy.

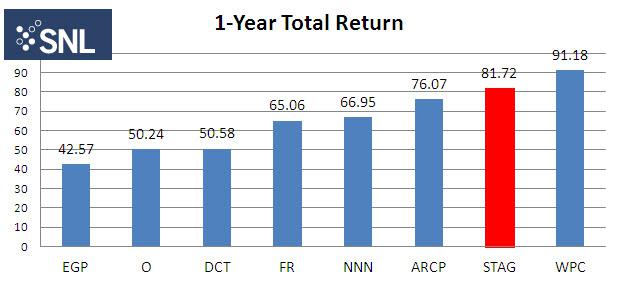

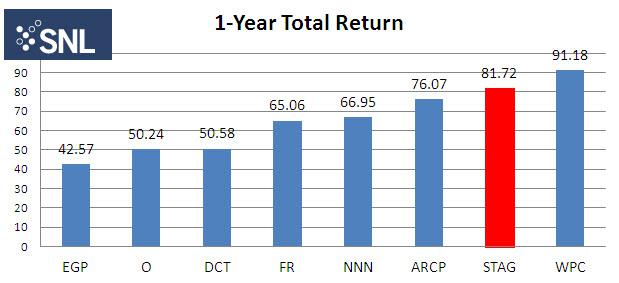

History is worth reviewing. Here is a snapshot of STAG's one year total return performance (Note: The S&P 500 returned 32.68% in the same time period).

(click to enlarge)

Here is a snapshot that compares STAG's one year performance with the peers (and select Triple Net REITs).

(click to enlarge)

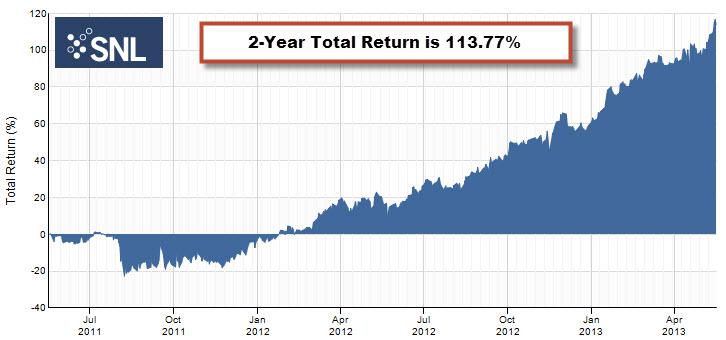

Now, here is a snapshot that illustrates STAG's two year total return performance:

(click to enlarge)

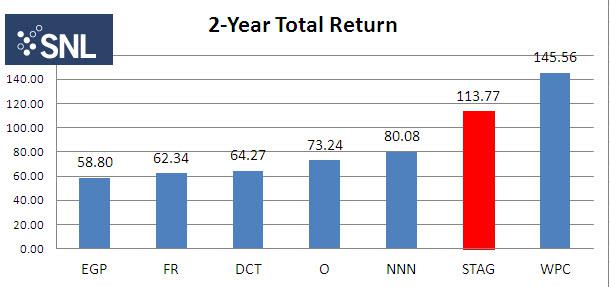

Here is a snapshot comparing STAG's two year total return history with the peers (and select Triple Net REITs):

(click to enlarge)

In early January 2013, I wrote an article on STAG (just four months ago) and I explained my bullish opinion on the differentiated Industrial REIT:

STAG's differentiated strategy is made up of three primary ingredients: yield (5.96%), diversification (172 properties), and growth (65.05% total return). I see plenty of runways remaining for STAG to keep growing its unique "secondary market" platform. In addition, STAG has an extraordinary value proposition in that the company is able to acquire assets at 8% to 9% cap rates utilizing conservative debt and with a weighted average interest rate of 4.2%.At the time I wrote that article STAG shares were trading at $18.12 per share with a P/FFO of 15.9. Now STAG shares have increased by over 30% to $23.59 and the P/FFO multiple is 17.8. Not quite the bargain I wrote about back in January when I said:

I'm not sure what (Ben) Graham would conclude, but I can sum up my course of action in one simple word: Wow!My view of STAG today is that the common shares are valued in the moderately expensive range and I would wait for a pullback and jump in closer at $21.00. Risk is risk and I would like to see STAG's dividend yield approach a more risk-adjusted high 5% handle. For current STAG owners, I would not sell unless you have a better alternative for growth and income. I believe that STAG has incredible growth potential, and although I don't believe returns will be as robust as 2012 (or Q1-13), I do believe that STAG will remain a hot REIT for the rest of 2013.

One final note, I like STAG's most recently opened Preferred Issue, STAG Industrial 6.625% Cumulative Preferred (STAG-B). The current price is $25.08 with a current yield of 6.61% (the earliest call date is 4-26-18). Fellow Seeking Alpha writer Doug K. Le Du recently wrote an article (17 New Preferred Stocks) and STAG was included. See chart below (provided by Doug K. Le Du):

I often recommend that investors implement a blended strategy of buying both REIT common stock and preferred stock. By taking advantage of this "hedged" strategy, investors can enjoy dividend growth and stock appreciation from common stock, while also profiting from the higher dividend yields from preferred stock. STAG's preferred issue (STAG-B) could add more of a complimentary "bond-like" component to the fixed-income portion of your portfolio.

In closing, here are some remarks from Ben Butcher, CEO of STAG, from the company's most recent (Q1-13) earnings call:

A busy and successful first quarter has set the tone for what we expect will be a great 2013 for STAG. We will continue to move forward with our low-levered strategy for the execution of our differentiated investment thesis. I continue to be proud of our team and the solid performance in executing our strategy in the public markets.(click to enlarge)

STAG continues to benefit from the combination of factors that provide a significant volume of quality and accretive opportunities for acquisitions, both on a relative value and a spread investment basis.

We believe that the ongoing improvement in the general economy, combined with the continued strength in the manufacturing sector, will positively impact our own portfolio in terms of occupancy levels and rental rates. The continued relative lack of speculative development generally across the country and specifically in our markets will enhance our performance of these important metrics.

Thus, we continue to be optimistic about the future of our company, for our owned assets and for our investment thesis. We believe that our business plan to aggregate and operate a large portfolio of granular and diversified industrial assets will produce strong and predictable returns for our shareholders.

Our first quarter operational results provide continued validation for this contention. We will continue our disciplined focus and shareholder returns. We thank you for your continued support.

Here is great way to access all REIT preferred shares: The Yield Hunter.

Source: SNL Financial, STAG Investor Presentation, FAST Graphs

REITs included: (O), (NNN), (WPC), (ARCP), (DCT), (EGP), and (FR).

Source:www.seekingalpha.com

No comments:

Post a Comment