Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I took a trip down memory lane: the last article I wrote about BlackBerry (BBRY) was on April 16, 2012. Back then, the company was featured in a report about Nokia (NOK). Basically, I wrote that BlackBerry smartphones serve a purpose and that Nokia was making a strategic blunder by partnering with Microsoft to develop smartphones. I'm not trying to blow my own French horn, but one year later, Northland Securities was wrong as Nokia didn't outperform. The share price is at the same level, if not lower, than it was one year ago. That said, I still believe that BlackBerry smartphones serve a purpose, but they don't serve enough of a purpose, as Samsung has developed the Galaxy Note II, which is probably the best business phone on the planet.

BlackBerry is the focus of this report that will try to help you (investors) improve your risk-adjusted returns or alpha. Hopefully, at the end of this report, you will have a deeper understanding of the communication equipment industry.

The industry, in this report, will be analyzed using the peer group Nokia, Apple (AAPL) and BlackBerry. We'll discuss BlackBerry's strategy, we'll do some equity and credit analysis. Finally, we'll finish with the relative valuations, technicals, and an investment recommendation. That should give us a pretty good idea of how we should be positioned with regard to common equity shares of BlackBerry.

The broader market has been rising and valuations have been increasing as the common equity share price of BlackBerry remains in a consolidation formation. That said, investors should accumulate common equity shares of BlackBerry as the shares remain undervalued. Next, we'll discuss BlackBerry's strategy.

Strategy

Getting the strategy right is critical for BlackBerry over the next few years. There are several parts to the strategy; we'll focus on the product refresh cycle, the QNX platform, the strategic alliances, the apps ecosystem, and the operational metrics. In my opinion, the strategic alliances and operational metrics are the most important parts of the strategy.

The launch of the BlackBerry 10 platform is a transition from the BlackBerry 7 platform. Thus, BlackBerry is refreshing its products over the next two or three years. The product refresh cycle should boost revenue as the BlackBerry 7 operating system became stale and weighed on the growth of the firm and market share of the firm. The BlackBerry 10 platform is built on the popular and powerful QNX software that could enable BlackBerry devices to perform tasks its competitors' devices can't perform.

BlackBerry is attempting to strengthen its strategic alliances and relationships. The areas of focus are software application developers and companies, global telecommunications carriers, intranet and Internet applications and portal companies, Internet social networking providers, multimedia content providers, gaming platform vendors, consumer electronic retailers, microchip and other manufacturers, and global systems integrators. The company is trying to improve the product it produces in several ways.

The BlackBerry strategy is also focused on the app ecosystem and developer community. The key decision was to allow developers for the Android platform to easily convert the programs to the BlackBerry platform. That should increase the amount and quality of apps available via BlackBerry World.

The Company is working on its efficiency. The BlackBerry marker is right-sizing the company. Also, it is trying to improve execution of product development and launches. The focus on operational metrics is key to the longevity of the enterprise.

The move to allow developers to convert apps from the Android platform to the BlackBerry platform should increase demand for the company's devices. That is a good move, but I would like to see the firm develop devices for the Android platform and the Windows platform. The problem with BlackBerry isn't the devices; at this point, the problem is the operating system. Developing devices for the competing platforms would go a long way toward reviving demand for the firm's devices.

Finally, the cost-cutting measure and product refresh cycle should be a positive surprise in calendar 2013. The product refresh cycle in calendar 2012 was weak: BlackBerry didn't produce anything interesting. Thus, the 2013 numbers should reflect the improvement in products launched and cost-cutting measures. Next, we'll do some credit analysis.

Credit Analysis

We'll compare the liquidity and solvency positions of the firms. Investors already know the strength of Apple's financial position because of its market dominance. BlackBerry's liquidity position and solvency are key metrics for the firm as it struggles to regain traction in the smartphone market. We'll use the current ratio, cash ratio, long-term debt-to-equity ratio, and financial leverage ratio to examine the firms' financial positions. We'll begin with BlackBerry.

Since fiscal 2011, BlackBerry's liquidity position improved: the cash ratio increased from 0.58 to 0.77 at the end of fiscal 2013. The long-term debt-to-equity ratio is zero. BlackBerry's solvency position improved: the financial leverage ratio declined from 1.44 at the end of fiscal 2011 to 1.39 at the end of fiscal 2013. Additionally, retained earnings represented 55 percent of total assets at the end of fiscal 2013.

Apple's liquidity position improved and the solvency position remained the same. The current ratio declined from 1.58 to 1.54 from the end of fiscal2011 to the end of fiscal 2012. The cash ratio declined from 0.87 to 0.85 during the same period. The financial leverage ratio remained at 1.54. Long-term debt-to-equity is zero.

Nokia is in the worst financial condition of the three firms. The liquidity position improved between the end of 2011 and the end of 2012: the cash ratio increased from 0.53 to 0.61. The solvency position deteriorated during the same period: the long-term debt-to-equity ratio increased from 0.44 to 1.11 and the financial leverage ratio increased from 2.60 to 3.17.

BlackBerry has a solid financial position: insolvency is not an issue in the foreseeable future. Apple has a lot of its cash in long-term securities; in terms of what I would consider cash-on-hand, BlackBerry's liquidity position is about the same as Apple's. Also, BlackBerry's financial leverage ratio is lower than Apple's financial leverage ratio: BlackBerry, by this metric, is more solvent than Apple.

Equity Analysis

In this section, we'll take a look at the operating margins of the firms. Where possible, we'll examine the smartphone segments of the firms. Also, we'll discuss the firms on a consolidated basis. Margin analysis is a key part of equity analysis.

BlackBerry's hardware and other revenue's 50 percent decline led a decline in the firm's total revenue during fiscal 2013; part of the weakness in revenue is attributed to a less than stellar product refresh cycle. The gross margin declined from about 44 percent in fiscal 2011 to 31 percent in fiscal 2013. The operating loss in fiscal 2013 was $1.2 billion. In fiscal 2014, I'm forecasting revenue in the $10 billion to $14 billion range, and I expect net income to be between $0 and $1 billion.

Apple's iPhone continues to be a driver of the company's growth. In fiscal 2012, iPhone unit sales increased 73 percent and iPhone revenue increased 69 percent. I am forecasting at least 28 percent growth in unit sales and at least 26 percent growth in revenue during fiscal 2013. On a consolidated basis, revenue grew 45 percent and net income grew 61 percent; the net profit margin was 27 percent. I'm forecasting double digit consolidated growth to continue in fiscal 2013.

Nokia's smart device sales declined 50 percent in fiscal 2012 as volume declined 45 percent. The gross margin declined from 23.7 percent to 8.8 percent, and operating expenses increased from 27 percent to 37 percent as a percentage of net sales; the smart device segment is unprofitable.

Mobile device sales declined 21 percent as volume declined 12 percent. Gross margin declined from 26.1 percent to 23.4 percent, and operating expenses increased from 14 percent to 18 percent as a percentage of net sales; the mobile device segment is profitable. On a consolidated basis, I'm not forecasting Nokia to return to profitability this fiscal year. I think revenue will stabilize.

The price elasticity of Nokia devices is 7.38. Price elasticity assumes everything about the buyer's plans remains constant; clearly that isn't the case in this situation. That said, Nokia devices are probably selling at a price above the mid-point of the demand curve and/or the demand curve is elastic. The data suggests that Nokia could decrease prices and generate more revenue.

Based on the evidence, Apple stole market share from BlackBerry and Nokia. I think BlackBerry will regain market share in fiscal 2014. We'll have to see how the operating expenses are managed in fiscal 2014 as the firm could return to profitability. Also, we'll have to see if BlackBerry can get its profit margin closer to the level of Apple's profit margin. Next, we'll cover the valuations.

Valuation

Nokia, BlackBerry, and Apple declined substantially in value because of investors' perceptions about financial performance challenges. The current valuations reflect those challenges. We, as investors, are concerned with the future financial performances and valuations. BlackBerry and Apple could command higher valuations in the year to come.

BlackBerry's current share price was $15.14. The forward price-sales ratio is between 0.57 and 0.79; the current price-sales ratio is 0.72. The forward price-earnings ratio is between 0 and 7.93; the current price-earnings ratio is negative.

Using a current share price for Apple of $429.79, I have a forward price-sales ratio between 1.99 and 2.25; the current price-sales ratio is 2.44. The forward price-earnings ratio is between 7.20 and 8.10; the current price-earnings ratio is 9.78. Using a current share price for Nokia of $3.30, the forward price-sales ratio is between 0.38 and 0.44. The current price-sales ratio is 0.41.

BlackBerry and Apple are undervalued on a relative and absolute basis as the outlook for the firms is better than the valuations imply. Nokia's valuation is justified on a current and forward basis.

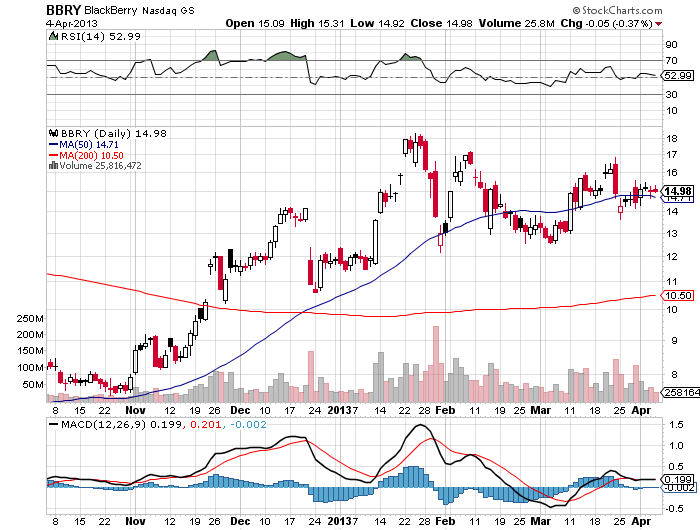

Technical Analysis

(click to enlarge)

All three firms are trading to the bear side of the market: there is excess selling and not enough demand for shares to boost the stock prices. The moving averages, momentum oscillators, and Dow theory will add more depth to the analysis.

All three firms are in intermediate-term bear markets: the 50-day simple moving averages are declining or flattening. Of the three, BlackBerry's share price is showing the most strength. The momentum indicators are suggesting that the share price of Apple could increase or at least consolidate. Momentum is confirming the decline in the share price of Nokia. We remain in a Dow theory defined bull market and throwbacks may be short lived.

Based solely on the technicals, investors should purchase shares of BlackBerry.

Conclusion

Investors should purchase shares of BlackBerry as the firm remains undervalued and the financial performance outlook is better than the valuations reflect. Further, the firm's liquidity and solvency positions are excellent.

Further research should add depth to the industry and companies.

By Christopher Grosvenor CMT

By Christopher Grosvenor CMT

Disclaimer: This article is not meant to establish or continue an investment advisory relationship. Before investing, readers should consult their financial advisor. Christopher Grosvenor does not know your financial situation and ability to bear risk and thus his opinions may not be suitable for all investors.

No comments:

Post a Comment