initiate any positions within the next 72 hours.

Return on Invested Capital

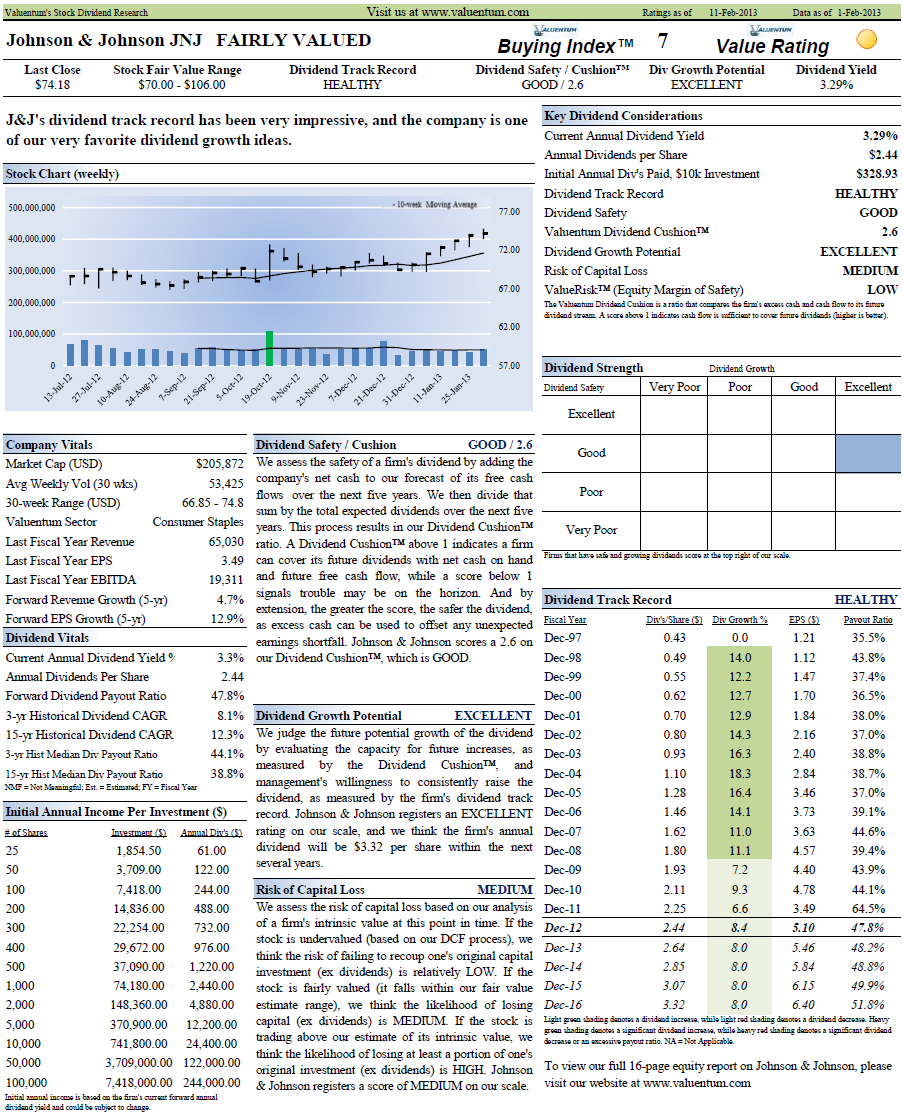

Johnson & Johnson's Dividend

(click to enlarge)

Johnson & Johnson's dividend yield is excellent, offering just under a 3% annual payout at recent price levels. We think the safety of Johnson & Johnson's dividend is good (please see our definitions at the bottom of this article). We measure the safety of the dividend in a unique but very straightforward fashion. As many know, earnings can fluctuate in any given year, so using the payout ratio in any given year has some limitations. Plus, companies can often encounter unforeseen charges, which makes earnings an even less-than-predictable measure of the safety of the dividend in any given year. We know that companies won't cut the dividend just because earnings have declined or they had a restructuring charge that put them in the red for the quarter (year). As such, we think that assessing the cash flows of a business allows us to determine whether it has the capacity to continue paying these cash outlays well into the future. Remember, earnings are accounting-based, while cash is...well...cash.

That has led us to develop the forward-looking Valuentum Dividend Cushion™. The measure is a ratio that sums the existing cash a company has on hand plus its expected future free cash flows over the next five years and divides that sum by future expected dividends over the same time period. Basically, if the score is above 1, the company has the capacity to pay out its expected future dividends. As income investors, however, we'd like to see a score much larger than 1 for a couple of reasons: 1) the higher the ratio, the more "cushion" the company has against unexpected earnings shortfalls, and 2) the higher the ratio, the greater capacity a dividend-payer has in boosting the dividend in the future. We do this for all companies.

For Johnson & Johnson, this score is 2.6, revealing that on its current path the firm can cover its future dividends with net cash on hand and future free cash flow almost 3 times. We also use our dividend cushion as a key decision component in choosing companies for addition to the portfolio of our Dividend Growth Newsletter.

Now on to the potential growth of Johnson & Johnson's dividend. As we mentioned above, we think the larger the "cushion" the larger capacity it has to raise the dividend. However, such dividend growth analysis is not complete until after considering management's willingness to increase the dividend. To do so, we evaluate the company's historical dividend track record. If there have been no dividend cuts in 10 years, the company has a nice growth rate, and a nice dividend cushion, its future potential dividend growth would be excellent, which is the case for Johnson & Johnson.

And because capital preservation is also an important consideration, we assess the risk associated with the potential for capital loss (offering investors a complete picture). In Johnson & Johnson's case, we currently think the shares are fairly valued, so the risk of capital loss medium. If we thought the shares were undervalued, the risk of capital loss would be low. All things considered, we like the potential growth and safety of Johnson & Johnson's dividend.

No comments:

Post a Comment