Driving Awareness of Soltamox

DARA Bio launched its leading product, Soltamox, in October 2012. Soltamox is a U.S. FDA approved (in 2006) oral liquid formulation of tamoxifen citrate primarily used to treat breast cancer. Soltamox is the only FDA approved oral liquid formulation of tamoxifen available for sale in the U.S. According to data from the American Cancer Society, some 230,000 women were diagnosed with breast cancer in 2011. An estimated 40,000 died from the disease. Tamoxifen is an antagonist of the estrogen receptor in breast tissue, and used as part of the standard of care for hormone receptor-positive breast cancer in pre-menopausal women.

Over the past several months, DARA has been conducting market research to identify the market opportunity for Soltamox; which is used when the patient either prefers or requires a liquid formulation due to difficulty swallowing (dysphagia). Dysphagia may be caused by oral mucositis, a common side effect of chemotherapy and radiation treatment. Data shows the liquid formulation provides ease of administration and convenience of dose. Post-menopausal women with hormone positive breast cancer may be on a number of oral medications. Soltamox provides differentiation from solid dose medications, and thus may lead to improved compliance.

And the data clearly shows that compliance is the key to survival. Current clinical practice guidelines from the American Society of Clinical Oncology recommend women with estrogen receptor positive (ER+) breast cancer stay on tamoxifen for five years. In November 2013, at the San Antonio Breast Cancer Symposium, data from the ATLAS (n=12,894) study, recently published in The Lancet, show that women taking tamoxifen for 10 years cut their risk of mortality by 29% when compared to women stopping treatment after five years. Unfortunately, compliance for even five years of tamoxifen therapy is low. We can only guess as to the reason why, but point to the fact that oral liquid formulations of cold and cough medications are preferred nearly 2:1 over tablets. We believe as high as 10% of female tamoxifen patients may prefer Soltamox over the generic tablet.

DARA's goal over the next few quarters will be to drive awareness of Soltamox. To do this, the company is enrolling patients in a registry called CAPTURE (Compliance and Preference for Tamoxifen Registry) with three key goals: 1) To identify the rate of dysphagia in hormone receptor-positive breast cancer women, 2) To quantify the percent of women that prefer a liquid formulation versus a tablet formulation, and 3) To better understand the compliance of women on tamoxifen. CAPTURE will seek to enroll 600 women at 25 leading cancer-treatment centers around the U.S., with the ultimate plan to publish the data in a medical journal in 2014. However, CAPTURE is a brilliant strategy in our opinion - it's both market research and marketing. Through CAPTURE, DARA will have the opportunity to introduce Soltamox directly to patients, and hopefully pull through prescriptions at the clinic.

DARA is also targeting high-prescribing tamoxifen oncologists and oncology nurses. The company recently published an educational brochure in the Oncology Nurse Society (ONS) journal, and will distribute marketing information to oncologists and nurses at both ASCO and ONS-Congress in the next few months. A high-prescribing oncologist may write as many as 2,000 prescriptions for tamoxifen a year. DARA's goal is to educate doctors and nurses on the rate of dysphagia and preference for liquid medications, and introduce Soltamox as the solution.

Soltamox's reported sales in the fourth quarter 2012 totaled roughly $54,000. However, we note the company deferred recognition of an additional $150,000 in revenues shipped to wholesalers. We expect the ramp to be slow in the first and second quarter of 2013, then gaining steam later in the year following key educational events and market research publications at both ASCO and ONS. DARA officially made Soltamox available in October 2012 to correspond with breast cancer awareness month; however, promotional activity really did not kick off until December, following the San Antonio Breast Cancer Symposium.

Soltamox has approximately 1.5% of the tamoxifen market in the UK and Ireland. We see the opportunity as similar, perhaps a tad bigger, in the U.S. With an estimated 2% share of the U.S. tamoxifen market, we see peak sales of Soltamox at roughly $20 million. We forecast sales in 2013 at $1.65 million, growing to nearly $20 million by the time of the patent expiration in 2018. The benefit to DARA is that patients starting on Soltamox will most likely continue on the drug for up to five years. We think sales will build slowly, but as awareness grows each patient turns into an annuity stream for the company, eventually leading to a highly profitable venture for DARA.

Launching Gelclair Soon

DARA plans to launch Gelclair in April 2013. We see a meaningful opportunity for Gelclair, as the product is an excellent complement to Soltamox. Gelclair is a hyaluronate sodium FDA approved for the treatment of oral mucositis. Oral mucositis is a common side effect of most cancer treatments. We have seen estimates ranging from 10% to as high as 30% of all cancer patients develop mucositis, nearly half of which may be grade 3 or 4. In grade 3 oral mucositis, the patient is unable to eat solid food, and in grade 4, the patient is unable to consume liquids as well. A recent study (Elting et al. Cancer 2008; 113:2704-13) reported that 87% of patients with severe mucositis used analgesics regularly during radiotherapy, 70% of which required opioid treatment. Over 400,000 patients per year will develop oral mucositis, representing a very large market opportunity for Gelclair.

Mucositis is most common in patients receiving radiotherapy for head and neck cancer. Data published in the Annals of Oncology in 2009 (20(supp4):174-7) cited almost 100% incidence for these patients, over 50% grade 3-4. Data published in the Journal of Supportive Oncology in 2007 (2(2 Suppl 1):13-21) cited a similar near 100% incidence for patients undergoing high-dose chemotherapy with hematopoietic stem cell transplant (HSCT). Oral mucositis is particularly profound and prolonged among HSCT recipients who receive total-body irradiation.

The idea of DARA distributing Gelclair marries well with the concept of Soltamox and Bionect, DARA's low-molecular weight hyaluronic acid for radiation burns. We see Gelclair as a potential $5 million opportunity in the U.S. The product has somewhat of a rocky past. Gelclair was approved by the U.S. FDA in January 2002 at UK-based Sinclair Pharmaceuticals. Sinclair licensed the product to Cell Pathways, and the product was launched in June 2002. In October 2002, Cell Pathways signed a co-promotion agreement with Celgene for the U.S. marketing and distribution of Gelclair. At that time, management at Cell Pathways stated that Gelclair was a potential $25 million product in the U.S., and the backing of Celgene seemed to validate that estimate. However, Cell Pathways, Inc. was acquired by OSI Pharmaceuticals in June 2003, and OSI Pharma terminated their co-promotion agreement with Celgene shortly after the deal closed. Meanwhile, Sinclair sold the global rights to Gelclair to Helsinn Group in August 2003. Gelclair struggled at OSI Pharmaceuticals, as OSI focused on the launch of Tarceva at Genentech and the later failed merger with Eyetech Pharmaceuticals. Gelclair posted U.S. sales of only $1.2 million in 2004, down from $1.6 million in 2003.

Following the merger with Eyetech Pharmaceuticals, OSI Pharma returned the U.S. rights of Gelclair to Helsinn in 2006. Helsinn licensed the rights to EKR Therapeutics in October 2006. EKR brought in ProStrakan Group to co-promote the product in April 2009. In 2009, we estimate Gelclair sales were around $4 million. However, EKR Therapeutics shifted focus in 2009 to the cardiovascular market and rights were returned to Helsinn. The product has been off the market since that time.

Despite being off the market since 2009, awareness of Gelclair remains high. DARA has been conducting market research over the past several months in anticipation of the launch domestically in April 2013. Management found that both awareness and interest in using the product is high. We suspect there may even be some pent-up demand for the product from high Gelclair prescribers back in 2009 excited to see the product return to the market. For 2013, we see Gelclair sales at $0.5 million, growing to $6.0 million by 2018.

Bionect Slow Going

In June 2012, DARA announced that it has launched Bionect for the treatment of skin irritation and burns associated with radiation therapy. There are an estimated 4,300 radiation oncologists in the U.S. DARA is targeting the top decile with its small dedicated specialty oncology and oncology supportive care sales team. Skin irritation is a common side effect associated with chemotherapy and radiation. Roughly two-thirds of cancer patients receive radiation therapy. Nearly all (87% according to DARA) will develop moderate to severe radio-dermatitis. Skin irritation is one of the primary side effects of radiation therapy, and a chief reason why patients discontinue treatment before a full cycle completes.

There is evidence (Radiotherapy and Oncology Vol.42(1997)155-161) that prophylactic use of hyaluronic acid cream during radiation treatment reduces the incidence of high grade radio-epithelitis, and may be used as a supportive treatment to improve compliance and quality of life in patients undergoing radiation therapy.

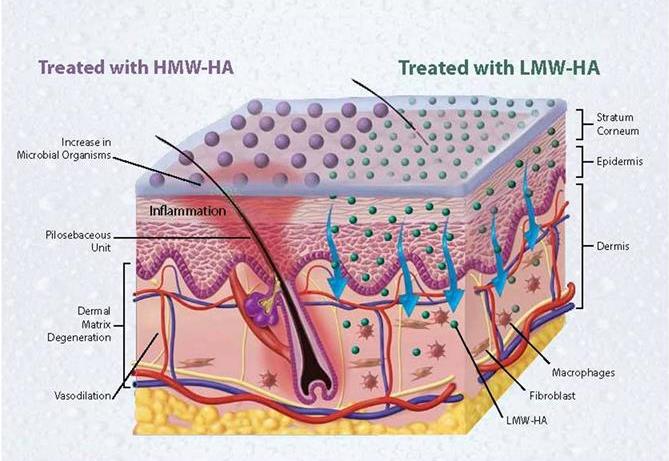

According to industry prescription tracking, there are an estimated 150,000 prescriptions for radiation dermatitis annually in the U.S. Remedy includes everything from A&D ointment, to aloe vera gel, to both low and high molecular weight hyaluronic acid. Studies show that high molecular weight hyaluronic acid does not penetrate into the dermis, and thus is ineffective in relieving symptoms of severe skin irritation caused by radiation. There is little active promotion of any pharmaceutical product for radiation-induced dermatitis. We believe that DARA could capture 5% to 10% market share with effective promotion.

Thus, sales reported to date have been negligible. DARA licensed the oncology rights to Bionect from privately-held Inncoutis Holdings, LLC. Inncoutis promotes the product into the dermatology market. Being a private company, we do not have a sales history on Bionect, but our best guess is that the product does around $3 million in revenues per year. Ultimately we see the sales potential into the oncology and radiation oncology market as a similar opportunity. We note that DARA will collect a tiered royalty (co-promotion payment) on each Bionect prescription it sells. Unfortunately, reimbursement around Bionect is poor and the product is primarily cash-pay. We suspect that DARA will spend the next few quarters ironing out the reimbursement issue with Bionect. By 2014 we believe the company will be able to start recording these co-promotion payments on the product. To DARA, we see Bionect as a $500,000 to $1.0 million revenue opportunity.

KRN5500 Remains the Key Wild Card

In November 2012, DARA Bio announced it has submitted an application to the U.S. FDA requesting Orphan Drug Status (ODS) for KRN5500 for the treatment of chronic chemotherapy-induced peripheral neuropathy (CCIPN). The U.S. FDA established the Orphan Drug Act in January 1983, with the ultimate goal of encouraging pharmaceutical and biotechnology companies to develop drugs for rare diseases that may have a small market. Under the law, companies that develop such a drug (a drug for a disorder affecting fewer than 200,000 people in the United States) may sell it without competition for seven years, as well as receiving waivers for regulatory fees and obtaining certain clinical trial tax incentives.

CCIPN is a type of pain that results from nerve damage and is characterized by an abnormal hypersensitivity to innocuous, as well as noxious stimuli. This type of pain is extremely difficult to manage, fails to respond to standard analgesic interventions including opioids, and often worsens over time. There are currently no FDA approved treatments for CCIPN. We remind investors that the U.S. FDA has previously granted DARA "Fast Track" status for KRN5500 in this indication.

We see the CCIPN market as highly attractive to DARA. There are an estimated 12 million Americans living with active cancer and some 1.6 million new cases each year. We found during our research that neuropathic pain occurs in 30% of cancer patients, with up to 90% in patients with advanced cancer. The incidence and severity of CCIPN vary considerably for each neurotoxic agent, administered alone or in combination, but for vincristine, cisplatin, oxaliplatin, and paclitaxel, estimates are as high as 70% to 90%. As many as 60% of patients treated with docetaxel and 40% treated with carboplatin develop CCIPN.

Conservatively, if we assume that 30% of 12 million cancer patients develop neuropathic pain, the market stands at approximately 3.6 million patients. Of that 3.6 million patients, we estimate that one-third, or around 1.2 million patients have developed chronic pain - i.e. pain that persists for at least three months after all chemotherapy has been stopped or completed. Standard of care for these patients includes gabapentin, pregabalin, and opioids. DARA is seeking an orphan indication from the FDA for those patients that are refractory to standard of care. Given the maximum allowable population of 200,000, we believe that DARA has carved out a subset of the 1.2 million cancer patients with chronic neuropathic pain, or perhaps 10-15% of this group.

DARA is currently engaged in dialogue with the agency on ODS. At this point, it's difficult to say whether or not DARA receives ODS on KRN5500. The chronic neuropathic pain in cancer patient market is clearly larger than 200,000. We see KRN5500 as having a significant market opportunity clearly beyond the subset of a subset of patients identified for the application. Obtaining ODS might make KRN5500 an attractive asset for a larger pharmaceutical company given the seven year exclusivity and waiver or PDUFA fees. However, other partners may only be interested in developing KRN5500 if they can target the larger 1.2 million or entire 3.6 million population identified above. We believe the data on KRN5500 is impressive enough to warrant moving forward regardless of ODS or not, and we encourage investors to view our previous piece from November 2012 that highlights the data and market opportunity.

Financial Review

Net loss for the fourth quarter 2012 totaled $1.9 million, or $0.10 per share. Loss was driven by $2.1 million in SG&A and $1.5 million in R&D. R&D included an annual PDUFA fee of $650,000 for Soltamox. DARA is attempting to have the fee reimbursed by the FDA given that it is the company's first wholly-owned commercial product. For the full year 2012, DARA reported a net loss of $7.3 million, or $0.60 per share.

DARA exited 2012 with $6.5 million in cash and investments, with around $5.0 million in positive net working capital. In January 2013, the company received approximately $2.5 million in net proceeds from issuance of Series B-3 and B-4 convertible preferred stock. Also, during the first quarter 2013, DARA had investors in the B-2 preferred stock exercise roughly 1.2 million warrants at $0.80 per share for proceeds of approximately $971,000 and 250,000 warrants at $1.00 per share for proceeds of approximately $250,000. We model an operating burn of roughly $2.0 million in the first quarter 2013. Therefore, we suspect that DARA held over $7.5 million in cash as of March 31, 2013. We find this to be sufficient to fund operations into 2014 given our modeled burn of around $2.0 million per quarter for the second, third, and fourth quarters of 2013.

Conclusion

Based on our DCF modeling, we see $2.00 per share as fair-value for the company. We see the company as well financed, with enough cash to fund operations into 2014. We see potential sources for non-dilutive capital by partnering KRN5500.

An interesting specialty pharmaceutical story has emerged. DARA is focusing on oncology and oncology supportive care products with Soltamox, Bionect, and Gelclair. We expect many of the same patients will be users of DARA's three core products, and that marketing and promoting the suite to oncology centers can be achieved in an efficient and profitable manner.

There are just over 15,000 oncologists in the country. The three largest areas include medical oncology, hematology, and radiation oncology. DARA is focusing on the top decile of physicians with a small sales force. The company is also looking to supplement or partner with other small specialty pharmaceutical companies, as well as with wholesalers or specialty oncology providers.

For example, in early April 2013, the company entered into a distribution agreement with Prime Therapeutics Specialty Pharmacy, LLC for distribution of both Soltamox and Gelclair. Prime Therapeutics is a pharmacy benefit manager serving nearly 20 million lives with roots into the Blue Cross and Blue Shield network. It's a deal that makes excellent sense for DARA as they seek to build out the network and drive sales of Soltamox and Gelclair in 2013. We note the company already had a previous deal in place with Onco360 Specialty Pharmacy.

We have conducted a discounted cash flow (DCF) analysis of DARA, which incorporates Soltamox, Bionect, Gelclair, and KRN5500. Our model has factored in the dilution from the recent registered direct and public offerings of preferred stock. We find fair-value to be above $2.00 per share. We think DARA is starting to look very interesting for long-term investors. The company is well financed, and Soltamox and Gelclair should be posting meaningful revenues by the end of the year. The big wild card remains KRN5500, which could be worth many multiples of the current valuation once validated in a pivotal program. Nevertheless, we see the current market value as vastly undervaluing this opportunity. From here on, it's all execution.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

By Jason Napodano, CFA www.propthink.com

No comments:

Post a Comment