Buy Hawaiian Airlines: Superior Hedging Practices And Recession Resistance Will Send Hawaiian Soaring

Whether or not to hedge fuel costs is a subject of great debate within the airline industry. And frankly, both sides of the argument have merit. U.S. Airways (LCC), for example, does not hedge its fuel costs, arguing that they are simply too expensive relative to the benefits they provide. And in low-price oil environments, that strategy makes sense. But should oil prices soar, U.S. Airways will be in trouble. Delta, on the other hand, uses elaborate swaps strategies to hedge its fuel costs, trading a potential for lower costs for certainty. But Delta's hedges come at a cost. The enemy of Delta's swaps is volatility. If oil prices fall too far, Delta will have to pay its counterparties, thus negating any benefits it would see from lower fuel prices. And mark-to-market hedging losses were responsible for Delta posting a GAAP loss in Q2 2012, even though it was cash flow positive (Delta also posted positive free cash flow) and had strong adjusted earnings. Hawaiian Airlines, however, takes a different approach to hedging. The vast majority of Hawaiian's hedges are in the form of call options on Brent or WTI crude, which give the airline a ceiling price, but not a floor. While it is true that call options are more expensive than swaps, they do allow airlines that utilize them to participate in a downward slide in fuel prices, something that airlines that utilize swaps cannot do.

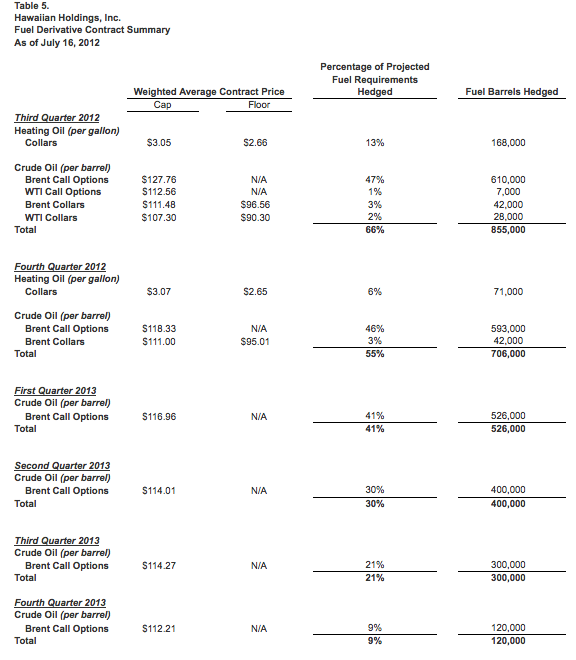

Currently, Hawaiian has 66% of its Q3 fuel needs hedged, and 55% of its Q4 fuel hedged. For Q3, 47% of the total is hedged via Brent call options, which have a ceiling price of $127.26 per barrel. As of this writing, Brent is trading at $116.37 per barrel. Hawaiian's hedging strategy works well because in a weak pricing environment for oil, the airline's hedging losses are more than offset by lower fuel prices. Once the call options are purchased, Hawaiian does not need to pay counterparties in the event of weakening oil prices. Delta, on the other hand, cannot take advantage of lower prices, as it has to pay counterparties when prices slide (on the converse, it is paid when prices rise). In Q2 2012, Hawaiian lost just over $14.823 million on its fuel hedges, but the company still posted a GAAP profit of 7 cents per share ($3.904 million). Listed below are Hawaiian's fuel hedges until Q4 2013.

(click to enlarge)

The proportion of fuel that is hedged for each quarter will rise as it draws nearer. While Hawaiian may not hedge all its fuel costs (doing so would be prohibitively expensive), the airline does hedge a majority of its costs, and that allows at least some certainty as to what kind of fuel prices the airline will pay (Delta's use of swaps provides more certainty, but locks the company into a specific price). Hawaiian's hedging practices allow it to have a level of certainty with regards to its fuel costs while still allowing the airline to benefit from lower fuel prices. And lower fuel prices are directly linked to the second element of our bullish thesis for Hawaiian Airlines: a measure of recession resistance.

The proportion of fuel that is hedged for each quarter will rise as it draws nearer. While Hawaiian may not hedge all its fuel costs (doing so would be prohibitively expensive), the airline does hedge a majority of its costs, and that allows at least some certainty as to what kind of fuel prices the airline will pay (Delta's use of swaps provides more certainty, but locks the company into a specific price). Hawaiian's hedging practices allow it to have a level of certainty with regards to its fuel costs while still allowing the airline to benefit from lower fuel prices. And lower fuel prices are directly linked to the second element of our bullish thesis for Hawaiian Airlines: a measure of recession resistance.Recession Resistance? At an Airline? It is in Fact Possible

On the surface, airlines are one of the most cyclical and economically dependent industry of them all. And for many airlines that is in fact the case. Business travel can fall of a cliff in a recession, which would impact many carriers, including Delta. Indeed, our bullish thesis on shares of Delta is based more on a structural strengthening of the company's financials than a solid, robust economic recovery. While we do not expect things to fall apart, either in the United States or abroad, it is difficult to have unbridled optimism about the global economy based on current fundamentals. We expect any recovery to be gradual (for Delta, that is all that is needed).

Hawaiian Airlines, however, has a measure of recession resistance, a rarity in the airline industry. How can this be possible? The answer lies in the type of customers Hawaiian has. Hawaiian Airlines is a leisure airline, and for the most part, does little to cater to business customers. After all, the airline's business is centered around travel to, from, and between the Hawaiian islands, and Hawaii, while being a wonderful leisure destination, is not a center for major business dealings. And therein lies the key to Hawaiian Airline's recession resistance. In recessions, leisure travel declines much less than business travel. In 2009, business travel dropped by 15%, even though the total travel market shrank by 11%. Leisure travel holds up much better than business travel in weak environments. Many industry executives within the leisure industry, including the CEO of Wyndham Worldwide (WYN), have noted that in periods of economic stress, consumers tend to adjust their travel plans to spend less, not cancel them all together. And that is a primary reason why Hawaiian can weather the effects of a recession better than other airlines. A recession will almost certainly lead to lower passenger yields, a key metric of profitability for airlines. But, a recession will also push down fuel prices, and because of the way that Hawaiian Airlines hedges its fuel costs, it will be able to capture the savings from lower fuel prices, likely neutralizing most of the yield pressure that a recession would bring. Are we saying that Hawaiian is immune to economic weakness? No. Consumers would most likely start to cancel their flights and travel plans if the global economy deteriorated a great deal. But unless the economic situation becomes dire, we think that Hawaiian can weather economic stress better than many other airlines.

Financial & Valuation Overview

As mentioned above, Hawaiian Airlines is profitable on a GAAP basis. In Q2 2012, revenues grew by 22.67% to $484.551 million. The gains were driven by growth in service routes, including new routes between Japan & Hawaii, as well as New York & Hawaii. Hawaiian Airlines posted operating cash flow of $90.28 million in Q2 2012 (Hawaiian did not break out its Q2 cash flows in its 10-Q for the quarter, so investors need to subtract the sum reported for Q1 from the 6 months of cash flow included in the airline's 10-Q filing for the latest quarter). Hawaiian has $686.844 million in total debt & capital lease obligations. But, Hawaiian also holds $446.557 million in cash & equivalents on its balance sheet, and the airline has $65.6 million in borrowing ability under its revolving credit facility. Hawaiian's liquidity profile is solid, and we do not expect that to change. In Q2 2012, Hawaiian's PRASM (passenger revenue per available seat mile) rose 6.1% from a year ago to 12.59 cents. Hawaiian's CASM (cost per available seat mile) inched up by 0.5% to 8.74 cents, but they should moderate in Q3. Q2 costs were impacted by expenses associated with starting new routes, as well as an necessary expansion of inter-island capacity. We expect Hawaiian to report better results on the cost front in Q3. Q3 results may also benefit from continued strength in the yen relative to the dollar. Hawaiian's new routes between Japan and Hawaii may appeal to budget-conscious Japanese travelers, which could boost the PRASM of Hawaiian's Asian routes, as well as its overall PRASM.

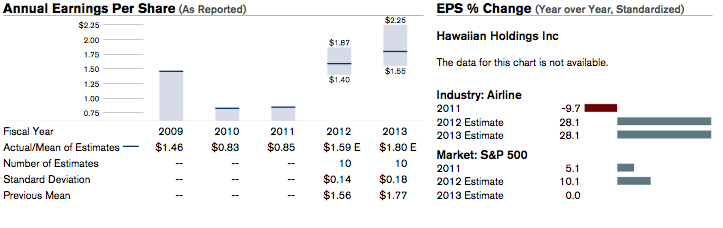

Hawaiian's valuation, in our view, does not reflect the company's growth prospects or its superior recession resistance relative to other airlines. Hawaiian is expected to earn $1.59 in EPS in 2012, and $1.80 in 2013 (data is sourced from Reuters).

(click to enlarge)

At its current price of $6.32 (as of this writing), Hawaiian trades at 3.97x 2012 earnings, and 3.51x 2013 earnings. We do not think that such a low valuation is warranted, for Hawaiian has more recession resistance than most airlines, and as such, we believe that Hawaiian deserves a richer valuation.

At its current price of $6.32 (as of this writing), Hawaiian trades at 3.97x 2012 earnings, and 3.51x 2013 earnings. We do not think that such a low valuation is warranted, for Hawaiian has more recession resistance than most airlines, and as such, we believe that Hawaiian deserves a richer valuation.Conclusions

Hawaiian Airlines is expanding its presence across all its markets. The airline dominates the Hawaiian inter-island market, and is growing in both Asia and the continental United States. Furthermore, Hawaiian's hedging practices give it some protection from high oil prices, while also allowing it to realize savings from lower oil prices. That along, with its exposure to the leisure travel market, makes Hawaiian much stronger than many airlines. And we believe that investors who choose to add to or initiate positions in Hawaiian Airlines will, in time, be rewarded for their convictions.

Disclosure: I am long DAL. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We may initiate a position in Hawaiian Holdings within the next several days.

By Helix Investment Management

No comments:

Post a Comment