Summary

- WhiteWave Foods’ products, including its Silk-branded soy milk, its Horizon Organic milk, and its other well-known brands, have made a splash in the natural and organic foods industries.

- With its acquisitions of Earthbound Farms and So Delicious in fiscal year 2014, the company is even more prepared to take advantage of shifting consumer preferences.

- The company is well-positioned to capture growth within emerging markets from its Chinese joint venture.

- Significant overvaluation may be justified by strong fundamentals and strong growth prospects.

- A share price drop in the range of 10%-20% to account for this overvaluation may warrant opening a position.

Introduction

With the recent trends in consumer tastes, it's hard to ignore the telltale signs that consumers are leaning more and more toward including natural and organic foods in their diets. Every corner of society, from religion, to film, tocars (Tesla Motors, Inc. (NASDAQ: TSLA)), to pop culture, has felt the shockwave from these changing consumer tastes, and many major players, such as Whole Foods Market, Inc. (NASDAQ: WFM), Kroger Co. (NYSE: KR), United Natural Foods, Inc. (NASDAQ: UNFI), Costco Wholesale Corporation (NASDAQ: COST), and Wal-Mart Stores, Inc. (NYSE: WMT), are adapting to meet demand and have profited handsomely.

You don't need studies or statistics to tell you this. A single trip to your local grocery store, and your eyes will be met with an exploding number of brands catering to the health-conscious shopper. Recently, I took a trip to my local Giant and Safeway and saw the following:

(click to enlarge)

Source: Local Giant Grocery Store

(click to enlarge)

Source: Local Target

After investigating some of the above spotted brands, including Silk, So Delicious, International Delight, LAND O LAKES, Horizon Organic, and Earthbound Farm, I discovered that they all belonged to WhiteWave Foods Co. (NYSE: WWAV), a company recently spun off from Dean Foods Co. (NYSE: DF) in 2012. Operating principally in the natural and organic food industries, WhiteWave specializes in developing, manufacturing, and producing plant-based foods and beverages, including coffee creamers, dairy products, and organic produce. With its portfolio of well-known brands mentioned above, its focus on the natural and organics industries, its healthy European operations, and its penetration into the Chinese markets, I believe WhiteWave is well-positioned for future rapid, long-term growth.

(click to enlarge)

Source: Stockcharts.com

And investor sentiment agrees. Since its IPO in late 2012, WWAV has risen non-stop: The stock's 50-day moving average has never fallen below the 200-day moving average. Despite being an overvalued investment, with a P/E TTM ratio (62.5) that is nearly double that of the industry average (32.4 from Morningstar.com), strong fundamentals, which are discussed below, indicate that the expensive valuation is most likely justified. Given a base case scenario implied share price in the range of $60.00-$85.00, a price drop in the range of 10%-20% to account for the overvaluation may warrant initiating a position.

Fundamentals

Split into three different segments, WhiteWave's operating structure consists of its Americas Foods & Beverages, Americas Fresh Foods, and Europe Foods & Beverages. The company's full portfolio of brands include the ones mentioned above, Alpro and Provamel from its European operations, and Silk ZhiPuMoFang from its Chinese joint venture. For the past few years since its IPO, growth among all three segments was strong, with overall sales increasing 11.0% and 35.2% (removing the organic salads, fruits and vegetables segment, which was recently formed from the Earthbound Farm acquisition, yields a sales increase of 12.6%) year-on-year for fiscal years 2013 and 2014, respectively. The chart below details the year-on-year increase in sales growth for each of WhiteWave's product segments. As you can see, the plant-based foods and beverages segment tends to generate the highest increase in sales growth, due mainly to the popular Silk brand.

(click to enlarge)

Source: WWAV Past Company Filings

By operating segment, it appears from the most recent 10-Q that sales growth has begun to slow down. For the three months ended March 31st for fiscal year 2015, sales growth was 14.7%, (4.4)%, and 4.1%, respectively, for Americas Foods & Beverages, Americas Fresh Foods, and Europe Foods & Beverages. Combined, this gives a cumulative net sales growth rate of just 9.7%, a decrease from the cumulative net sales growth rate of 12.5% from the same quarter last year (after adjusting for the Earthbound Farm acquisition). However, the 4.1% increase in net sales from the Europe Foods & Beverages segment is misleading. Looking at the consolidated statements of income from the most recent 10-Q, we can see a foreign currency translation adjustment of a whopping negative $43.7M, driving net income into the red zone. This is a result of the strengthening Dollar in relation to the Euro, thelatter's value having plummeted as a result of Greece's troubles.

Source: Google.com

According to management, unfavorable foreign currency translation resulted in an 18.8% reduction in the Europe Foods & Beverages segment. Adjusting for this translation results in a normalized sales growth rate of 22.9%, which boosts the cumulative net sales growth rate to 12.6%, in line with historical growth rates.

WhiteWave's sales mix is well-diversified and has remained relatively stable among its different divisions. With the acquisition of Earthbound Farms in fiscal year 2014, the company added organic salads, fruits, and vegetables to its product portfolio.

(click to enlarge)

Source: WWAV Past Company Filings

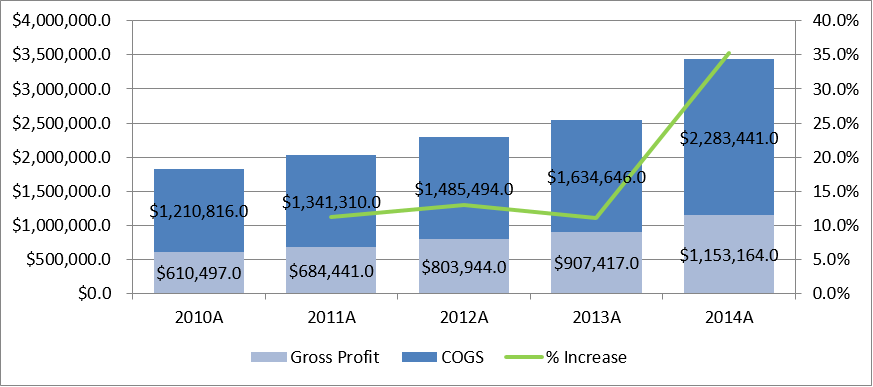

In the chart below, you can see that overall year-on-year sales growth has generally been steady, hovering around the 10%-15% range for the past few fiscal years. Gross margins have been constant as well in around the 33%-35% range.

(click to enlarge)

Source: WWAV Past Company Filings

Balance sheet-wise, WhiteWave is mostly healthy, but there is some cause for concern. Cash has fluctuated a lot since the company's IPO, and a current ratio of 1.1 is nothing to boast about. Retained earnings continue to steadily increase. Of particular note is the company's substantial indebtedness: The company has a debt-to-equity ratio of 1.4, as opposed to the industry average of 0.9 (taken from Morningstar.com). The company has several debt facilities in place, which it has used to fund certain of its acquisitions, including a revolving credit facility for $1B, aggregate term loans for $1B, and senior unsecured notes for $500M. This high amount of debt may impede WhiteWave from obtaining future debt funding in the future. With an ROIC of only around 7% for the past few years, one wonders if taking on the enormous amount of debt was justified. However, an obvious counterargument would be that WhiteWave is positioning itself for future growth and that this growth has not yet been realized.

Concentrating its focus on specializing in particular niches within the natural and organic foods industries, the company has used its debt to fund its long string of acquisitions while strategically divesting unnecessary and unprofitable business segments. 2014 was an intensive year for WhiteWave, which completed several business ventures during this time. One of its most prominent acquisitions was in fiscal year 2014 when, for $600M, it acquired Earthbound Farms, one of the largest producers of organic produce in the industry. Later in the same year, WhiteWave acquired So Delicious Dairy Free, which caters to the vegan crowd, for $200M. Most recently, the company announced its intentions to further expand its reach in the plant-based nutrition market with its acquisition of Vega Foods, which produces vegan shakes and snack bars, for $550M.

With these acquisitions and the organic growth achieved through them, WhiteWave has managed to propel its brands to among the most recognized in its markets. In fiscal year 2014, WhiteWave held the #1 position in terms of market share for its plant-based foods and beverages segment as well as the #2 position in coffee creamers and beverages, with Nestlé's (VTX: NESN)COFFEE-MATE taking the lead. Furthermore, in its European segment, WhiteWave is also #1 in plant-based foods and beverages.

(click to enlarge)

Source: 2014 CEO Letter from Investor Relations Website

Complementing its increased penetration into its specialized markets, WhiteWave has also shaved off unprofitable business segments, including its SoFine soy-based meat alternatives business as well an Idaho dairy farm.

Chinese Joint Venture

One of the most exciting things about WhiteWave is its untapped growth potential. Although sales growth across all segments has exploded, the company still perseveres to explore untapped, emerging markets, such as China. With China's growing middle class, you can expect people to consume more and begin to be able to afford the health-conscious attitude that those in developed countries have been adopting.

WhiteWave has realized this trend, and in reaction, the company formed a joint venture with a Chinese dairy company known as Mengniu Dairy Company. To ride the wave of consumer trends within China, the company expects to manufacturer its almond and walnut beverages under the brand name, Silk ZhiPuMoFang.

Given that the Chinese have always been long-time consumers of soy milk, WhiteWave, in its Q1 earnings call, believes that there is significant growth to be realized in the Chinese market. However, it also stated that 2015 will be a test year to determine pricing and the type of product portfolio it wants to deploy within China (e.g. to include or not to include soy). Management commented on its commitment to the Chinese market, so investors can expect the Chinese market to be an additional catalyst to drive sales in the long term.

Valuation

As WhiteWave is relatively young, I decided to project a DCF model for ten years. Given the enormous growth potential for the company, I assumed an initial sales growth of 12.0% starting fiscal year 2016, which is in line with historical values. I determined that the sales growth rate would increase year-on-year by 75 basis points to 15.0% for my base case, upon which it would increase by half that rate throughout fiscal year 2025. Management case and worst case scenarios were higher and lower variations of my base case projections, respectively.

Gross margin was set to improve by 72 basis points year-on-year throughout fiscal year 2020, whereupon improvement would increase by half that rate throughout fiscal year 2025. SG&A was modeled using a similar trend. D&A and taxes were held constant at 3.2% and 35.0%, respectively, which are in line with historical values. I expected the company to increase its capex rapidly until fiscal year 2020 to 8.3%, when it would stabilize; this expectation was assumed as a result of the investments management plans to make in its Chinese joint venture as well as its massive growth rates in Europe. Changes in working capital were expected to change linearly in an immaterial manner.

To calculate my WACC, I took a bottom-up approach and determined my equity risk premium by region weighted by sales. Combined with a relatively high beta and a risk-free rate of 2.4% (10-year US treasury), this calculation yielded a cost of equity of 13.0%. Cost of debt was determined by a weighted average approach using interest rates provided by WhiteWave's most recent 10-K.

(click to enlarge)

Assuming an exit multiple of 18.0x, taken from an average of WhiteWave's competitors, I calculated a base case implied share price of $70.00. Varying the exit multiple and WACC by 1.0x and 1.0%, respectively, yielded a base case implied share price range of $60.00-$85.00.

Source: Yahoo Finance and Company Filings

(click to enlarge)

Management case estimates, assuming higher sales growth rates and more robust margins, yielded an intrinsic share price range from $70.00-$95.00.

(click to enlarge)

In terms of downside risk, my worst case scenario yielded an implied share price that was roughly in line with the market price.

(click to enlarge) Risks

Risks

Risks

Risks

Given the intensely competitive nature of the industries that WhiteWave operates in, it's hard to ignore the large TTM P/E ratio. WhiteWave possesses a TTM P/E ratio that is roughly double that of the industry average. As such, the company could be considered a GARP investment.

The large market share that WhiteWave possesses in many of its product categories could be considered a double-edged sword. The company's soy-based foods and beverages has largely matured and, these days, only sees growth in the mid-single digits. However, it is clearly evident that the company has taken the initiative to penetrate new geographic and product markets, and I am confident that WhiteWave will continue to impress its shareholders.

In any case, to mitigate risk, the prudent investor could consider taking a position in some of WhiteWave's competitors or purchasing protective put options. I would also recommend opening a position when the stock loses some of its momentum. Given WhiteWave's popular and diverse brand portfolio, any setbacks would most likely be temporary.

Conclusion

As one of the fastest growing food companies in America, WhiteWave is an excellent opportunity to invest in the growing consumer trends within the food industry. An investment in WhiteWave presents some excellent upside opportunities (~40% upside base case) with minimal to no downside. With its penetration into new product and geographic markets and the popularity of its brand portfolio, WhiteWave would be a lucrative addition to any portfolio.

No comments:

Post a Comment