"There is only one thing worse than being talked about and that is NOT being talked about" (Oscar Wilde). With the recent talks on a buyout or breakup, I would like to evaluate BlackBerry's business and potential (and why a buyout might not be the best option).

"There is only one thing worse than being talked about and that is NOT being talked about" (Oscar Wilde). With the recent talks on a buyout or breakup, I would like to evaluate BlackBerry's business and potential (and why a buyout might not be the best option).

Though BlackBerry's (BBRY) FY2014 Q1 earnings were very disappointing, and not what I was expecting (or hoping for), it can still be interpreted in several ways. In my previous article, I discussed BlackBerry's current position with consumers, and how it compares to its competitors. Though the new BB10 operating system is highly rated and well accepted by current consumers, it seems to have problems gaining traction.

After BlackBerry's FY2014 Q1 earnings short interest on June 28 was above 184 million shares, and is now hanging around 140 million shares, still making shares extremely volatile. While a high short interest implies high volatility and a bleak outlook, the opposite can be said about institutional ownership. Yahoo! Finance states that 62% of the float is held by institutions, which can help limit large declines.

With BlackBerry's current $3.1 Billion in short-term investments and cash, short sellers are betting on a chain of events to stop profitability and weaken the balance sheet. At the current point of time, I have compiled several weaknesses of BlackBerry as a company:

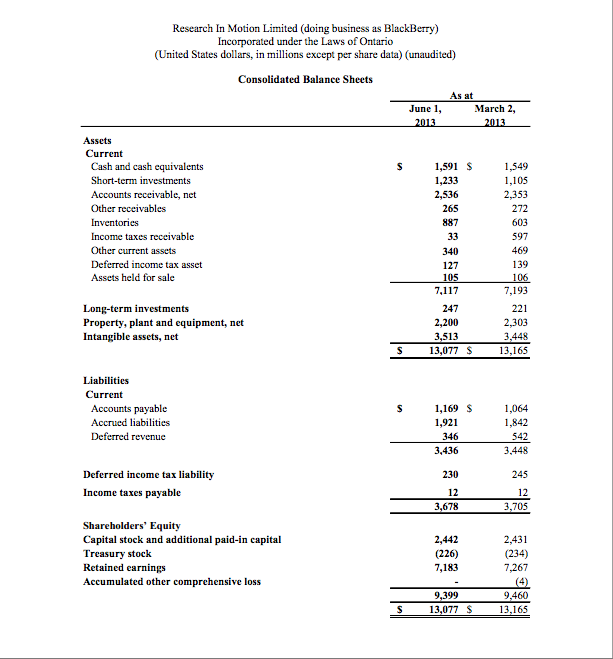

1) Weak(er) Balance Sheet -- Shorts cannot deny the strong shareholder equity, but might not believe that it is the 'current' $9.4 Billion ($17.93 a share). Accounts receivable continue to rise (now $2.54 Billion) as do accrued liabilities ($1.92 Billion) and accounts payable ($1.17 Billion). By stalling payment, BlackBerry is able to 'conserve' cash on its balance sheet. BlackBerry's intangibles might not be worth $3.5 Billion with new technologies as well as the risks and costs that come with patent trolling.

(click to enlarge)

2) Declining Sales -- Due to chaos in Egypt, an H1N1 outbreak in Venezuela, and high competition in emerging markets, much of BlackBerry's 'key' countries can experience a stall or a steep decrease in sales. With the uncertainty in the Middle East (possibly on the edge of another war), one of the last things they will be doing is buying new high-end cell phones.

3) Bad Management -- Thorsten Heins has predicted sales of "several tens of millions" for their new Q10 phone - it would be lucky if they broke 1.5 million Q10's in their major debut which was revealed in the most recent quarter. Heins has made some bold predictions like the death of the tablet in five years -- though the Playbook may be dead, the rest of the market seems to be thriving. It is time for Heins to reveal part of BlackBerry's playbook on how it plans to compete and expand. BlackBerry continues to post a loss and remain behind the competition, as well as keeping investors in the dark (they will no longer announce their subscriber base either).

4) Terrible BB10 Release -- Though the BB10 operating system may be superior to much of the competition, it was not released to the public in an effective manner. In the most recent quarter, they lost more subscribers than signed up for their new OS, showing both strong competition and BlackBerry's weakness.

Though there are many more negatives (as there are with any company), I feel I have covered much of the short's thesis. I do not agree with the current valuation, and will point out some flaws in the short's thesis:

1) Risk leads to Reward -- BlackBerry has been using accounts payable and accrued liabilities to help 'build' their cash pile. The actual risk of BlackBerry's balance sheet remains unknown, though can be estimated.

The $3.5 Billion in intangibles not only refers to BlackBerry's patent portfolio (conservatively valued at $2.25 Billion), but also their Subscriber Base, BlackBerry Enterprise Systems (BES), and BlackBerry Messenger (BBM). With the extension of BES and BBM to other platforms it is likely to greatly expand in size, and may eventually help BlackBerry grow its service revenue (which has been in freefall). Even though service revenue may be declining, it still was approximately $800 million (26% of revenue) in the most recent quarter.

I also estimate that BlackBerry spent approximately $150 million more on advertising than the previous quarter. SG&A increased to $673 million in Q1 compared to $523 million in Q4. If BlackBerry were to use their advertising money more effectively, they could begin to scale back the cost, increasing profitability.

2) Sales Continue to Grow -- Despite the H1N1 outbreak in Venezuela, BlackBerry still grew its revenue by 9% compared to the same quarter last year, as well as expanding its margins from 28% to 33.9%. Any outbreak affects not only BlackBerry, but also its competition. BlackBerry is still coming out with a new BB7 (as well as the Q5) phone to help gain traction in emerging markets.

3) Heins' Vision -- Though many investors (including myself) may question whether Heins is the best fit for BlackBerry, he is not the only one who affects the company. BlackBerry's lawyers, researchers, and marketing staff are helping to make BlackBerry a prominent force in the cell phone market.

4) Not Bad for the Price -- Though I agree that the BB10 launch could have been better, the current valuation does not even support a complete flop. Millions of units have been sold, while Q1 did not include the US launch of the Q10 or the Q5's launch. The important thing is that BlackBerry has invested Billions to create a new OS which is able to compete with Android, Windows, and iOS. Now that they have developed its skeleton, they can begin to fix its flaws (apps, bugs, etc.) and transpose it onto different hardware (Z15, R-Series, tablets, and even computers).

BlackBerry is beginning its transition from a value investment, to a safe and growing company with no debt (unaffected by US interest rate fluctuations) which will begin to appeal to a larger group of investors.

When the market valuates a company at less than 60% of its book value, there are some major risks, as there is when you invest in any company. In this scenario though, I believe that BlackBerry's current value outweighs the current risks, but the future has a lot in store.

BlackBerry currently owns several companies including QNX, the leader in automotive solutions, as well as a major player in defense, industrial, medical, and networking fields. QNX's reach and dominance can help it expand profitability and revenue in the near future (and could also be a key part in a break up of BlackBerry).

BlackBerry also owns hidden gems like Certicom:

the world-leading expert in public key infrastructure implementations, device security, anti-counterfeiting, product authentication, asset management, and fixed-mobile convergence, many of the largest companies and government agencies rely on Certicom technology to secure applications, communications, and mobile devices while protecting content and other critical assets.

Certicom is shipping nearly 1 Million Zigbee Certificates every month (as of May 2012), one of their many products. Since they cost around $500each, Certicom can be earning around $500 Million a month. Add in several other products and solutions, Certicom can be a huge entity on its own. Though Certicom itself has not had a press release in a few months, the Zigbee website is still active, as of July 24, 2013 (last press release).

BlackBerry has also scored a major deal with the DOD (on August 8) not for its 30,000 device order, but for the restored consumer confidence. If the US government uses BlackBerry as its cellular provider, then so should any business across the country (or world). BlackBerry is also expanding their enterprise system, BES 10, to other platforms including iOS and Android. By doing this, businesses can pay as little as $99 a year for Mobile Device Management, as well as BlackBerry Balance and BlackBerry Hub. This brings high margin revenue to BlackBerry for an extended period of time, while offering a great service to businesses.

The largest future potential for BlackBerry in my opinion is BlackBerry Messenger (BBM). BBM is not only a text messaging service, but a social tool too. BlackBerry has unveiled multiple unique features including BBM Video, BBM Voice, and BBM Connected Apps -- all of which can be used by consumers and businesses alike. BBM's unique features are sure to attract customers and advertisers. By tracking user's shared apps, location, and conversations, BlackBerry can offer advertisers unique data on consumers, leading to an increase in software revenue. For contrast,WhatsApp currently has 300 Million active users, paying .99 a year - if BlackBerry could attract 200 Million consumers with a FREE enhanced service they could generate millions:

Taking into account that the average Cost per Thousand Impressions (CPM) on mobile devices is .75, we can calculate BBM's potential revenue. Consider 200 Million users view 20 advertisements (20 impressions) a day (4 Billion) -- that would generate $3 Million in revenue a day, or around $1.1 Billion a year.

As BlackBerry's software revenue is currently in freefall, the additional BES 10 and BBM revenue can help restore BlackBerry's prominence and stock price.

Just recently BlackBerry announced that they were willing to go private, so what would be the advantage? BlackBerry could keep its technology and software hidden until its release, unlike with BBM. Because of their website, press releases, and conference calls, other competitors like Apple (AAPL) have caught wind and even filed for a patent. If BlackBerry goes private, it may be able to unlock more value on its balance sheet. Even if they sell only their software or hardware business, the value unlocked (plus their current assets) is worth well more than their current $5 Billion evaluation (closer to $10 Billion).

Even as more details come out about a possible sale or privatization, I am still against the idea. If a buyout does come, it would not come close to the $18 book value a share, as there would be no reason to make that offer at this point in time. Instead, I would prefer a sale or merger of either its software or hardware business. In fact, Silver Lake Partners have recently spoken to BlackBerry regarding a merger with Dell (DELL) - a match made in heaven for both parties.

I would like to cover BlackBerry's potential value, as well as calculated buyout price:

Evercore Partner's Mark McKechnie values a potential BlackBerry buyout at $10 ($1.9B patents, $1.2B BES, $2.2B Cash and $0 for everything else), while Jefferies believes the breakup value is closer to $15. Using everything I have listed above, I would like to create my own evaluation of BlackBerry:

| Cash | $2.9B |

| Patents | $2.25B |

| BBM | $1.7B |

| BES | $1.2B |

| Hardware | $2B - $3B |

| Everything Else | $0 |

| Total | $10B - $11B |

I value BlackBerry at roughly $19.50 to $21.50 a share. The main differences between Mark McKechnie's valuation and mine is that I value the patents at $2.25B (compared to $1.9B), I include the short-term investments in cash ($700 Million), value BBM at $1.7B (1.5x calculated sales), and the hardware business at $2B - $3B. The only real differences between our evaluations are BBM (which is discussed above) and the hardware business.

I am valuing the hardware business at $2B - $3B based on both sales and income. BlackBerry is running 30% margins on its new flagship devices, making it extremely profitable for BlackBerry even if they only sell a few million devices a year. If they sell just 5 Million devices a year at ASP of $300, they will generate $1.5B in revenue or $450M in gross profit a year, leaving them to trade at 5 - 7 times gross profit. In addition, they currently have more than $500M in inventory, giving them a stepping stone to profitability.

There are many ways in which BlackBerry can create shareholder value, but in order to maximize it, they should avoid a complete sale of the company. Instead, a sale of their patents for just $2B, as well as the sale of the BlackBerry Enterprise System (BES) for just $1.2B would leave the company with more than $6.1B in cash (they are currently trading at a market cap of $5.56B). There are many suitors for BlackBerry's extensive and well known enterprise system, including Dell, HP (HPQ), IBM (IBM), Cisco (CSCO), or even the US Government. As for their hardware business, a buyer can be harder to come by, limiting them in possibilities to competitors like Nokia (NOK), Samsung (SSNLF), Apple,ZTE, Huawei, Lenovo, Microsoft (MSFT), or maybe Amazon (AMZN).

BlackBerry has the opportunity to turn around their software business through both BES 10 and BBM, while increasing profitability and interest in their hardware. While a sale of the software business may leave BlackBerry without a growing entity, they have the power to create one through the high margin BB10 phones and emerging BBM, as well as the cash that a sale would leave behind.

As more details emerge on BlackBerry, it is not the main reason to own the stock: the interest in the purchase or merger in BlackBerry just shows its true value. With BlackBerry sitting on a pile of cash, they can invest in multiple measures to increase profitability and restore its place in the enterprise and consumer worlds. With BlackBerry now on the investor's side, it will be interesting when they reveal their new playbook on creating shareholder equity.

No comments:

Post a Comment