Analysts estimate a FY2014 earnings of $1.37 per share, an almost 50% increase to current full year estimates. While we do not disagree with the average EPS forecast, we disagree with the current valuation and the earnings multiple investors assign the stock.

Three misconceptions about Bank of America

1. The stock had quite a run-up over the last year and it would be difficult to justify a further increase in valuation.

(Click to enlarge)

Though it is true that Bank of America has performed very well over the last year, it is up 89%, Bank of America was extraordinarily beaten down during the financial crisis. Compared to its peer group, BAC is still materially lagging in terms of price appreciation. Put into perspective, Bank of America is still the second worst performer of its peer group consisting of Citigroup (C), Goldman Sachs (GS) and Wells Fargo(WFC):

(Click to enlarge)

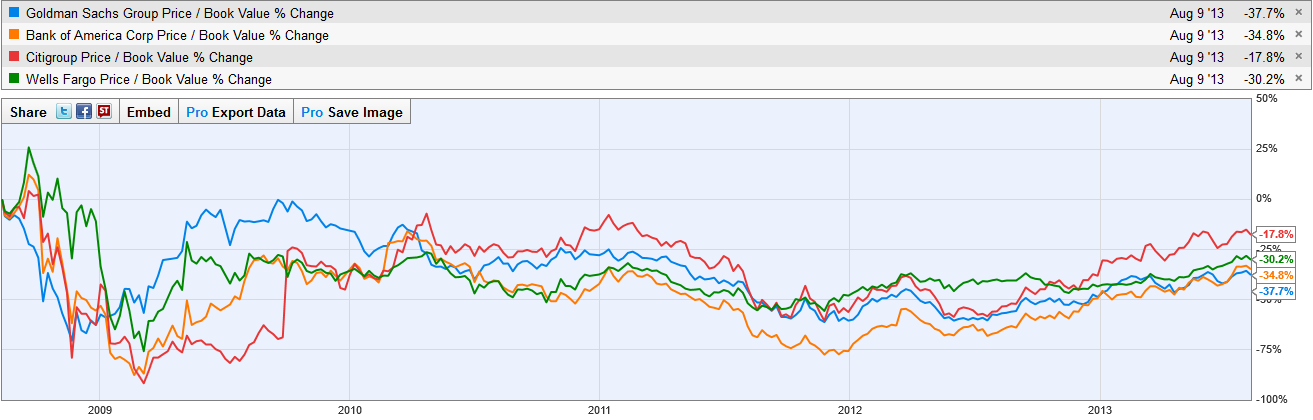

Because of the financial crisis and the corresponding mortgage legacy issues associated with mortgage lender Countrywide, investors have lost confidence in the quality of Bank of America's book value. The market has clearly punished the company for its heavy reliance on the mortgage business as indicated by its lagging price/book performance:

(Click to enlarge)

We believe, that after years of close market scrutiny and landmark mortgage-related settlements ($8.5 billion settlement reached in 2012, $1.7 billion in 2013), Bank of America's book value is stabilized.

We also assert that investors take a one-sided view with respect to Bank of America's mortgage business. It is true that bad mortgages from Countrywide were largely responsible for Bank of America's book value deterioration. However, underwriting discipline has materially increased over the last four years improving the overall quality of the mortgage pool held BAC's balance sheet. We are also confident that a strongly rebounding housing market in the U.S. will turn Bank of America's hated mortgage business soon into a loved one that materially drives earnings and cash flow.

2. Another issue that had a disproportionate effect on Bank of America's stock price was the ongoing legal battle with mortgage insurer MBIA (MBI) that dragged on for years. As Wall Street fears nothing more than uncertainty, the unresolved issue about mortgage-backed securities took a toll on both companies' stock prices. Consequently, investors were relieved as the final settlement was announced in May 2013 (as reported by dealbook):

Bank of America and MBIA, the troubled bond insurer, have reached a $1.7 billion agreement to settle a long-running legal dispute over mortgage-backed securities that became troubled when the financial crisis blossomed.

While the deal had a more meaningful impact on MBIA, Bank of America investors could be relieved that this long-lasting legal battle had finally been resolved for good.

Bank of America said the agreement would reduce its previously announced first quarter after-tax profits by $1.1 billion, or 10 cents a share, but would improve its capital position. MBIA indicated that the settlement would have little impact on its profits, but said its first-quarter results, scheduled to be released on Thursday, would be delayed.

With uncertainty out of the way, investors are likely to increase their confidence in the successful mitigation of legal risks and the earnings prospects of the company. A significant barrier to price appreciation has been broken down.

3. While the stock has clearly underperformed over the last years (compared to its close peers), Bank of America has made significant effort to resolve legal issues which clouded its intrinsic value. From a comparative point of view (see below), Bank of America trades at the largest discount to book value while Goldman Sachs and Wells Fargo already manage to trade at a premium.

(Click to enlarge)

Even though Bank of America had a great Q2 with an EPS estimate beat of 28%, its valuation continues to lack its peers. While the P/B industry average stands at 1.1, Bank of America is comparatively cheap with a near 30% discount from book value and a near 10% earnings yield providing investors with a significant margin of safety.

Conclusion

Bank of America's stock price and valuation lag its immediate peers. While reducing uncertainty with respect to book value credibility and legal risks, Bank of America's valuation remains low and attractive. We also estimate that Bank of America will step up its shareholder remuneration policy with an estimated annualized dividend yield of 2-3% in 2014/15.

As the economy improves, Bank of America should profit from higher consumer spending and an increased transaction business with a strong possibility to outperform EPS estimates.

No comments:

Post a Comment