- Revenue growth accelerated dramatically on both a sequential and year-over-year basis.

- Q2 Mobile advertising revenues posted a dramatic acceleration in sequential growth over Q1.

- Underlying profitability also accelerated, with the company posting non-GAAP operating margins of 44%, along with much improved cash-flows.

Facebook's dramatic inflection point now makes it a must-own stock for many levels of investors. Prop traders will provide a near-term boost, as they add to positions in next week's expected month-end mark-up by mutual fund and pension owners. With re-allocations of large long-term holders winding down next week, new aggressive growth-oriented institutional investors will have to raise their bids aggressively to get the positions they desire.

We see $36-$37 by the end of August, $40-$45 by year-end, and then $50 by next spring.

Revenue Growth Accelerates Two Quarters in a Row

Here is how Facebook's financials looked through the end of 2012:

(click to enlarge)

Top-line growth began to accelerate in the back half of the year, with mobile advertising revenues improving strongly from Q3 to Q4.

Mobile Advertising Revenue Acceleration Poised to Continue

Facebook's momentum in mobile accelerated even further during the first two quarters of 2013. In particular, note the dramatic acceleration between Q1 and Q2:

Mobile's percentage of total ad revenues/total mobile spend

Q3, '12: 14%, $150 million

Q4, '12: 23%, $305 million

Q1, '13: 30%/$375 million

Q2, '14: 41%/$656 million

Think about that. In four quarters, Facebook's mobile advertising revenues have mushroomed from nothing to an annualized run-rate of $2.5 billion exiting Q2.

Q3 will be the first quarter of year-over-year comparisons. We expect mobile ad revenues to grow 200-400% year-over year for the next three quarters.

Facebook will exit 2013 with its mobile ad revenues at a $4 billion annualized run-rate, logging 300% year-over-year growth in Q4. These accelerating growth rates support an expanding P/E and a much higher price to sales multiple.

They also support two other conclusions. One, Facebook has figured out how to monetize mobile. Two, Mark Zuckerberg was right - mobile is the company's biggest engine for growth.

Mark Zuckerberg was Right: Mobile Is the Engine for Growth

Since last fall, Facebook has made a very strong case that it has figured out how to monetize mobile. We have highlighted selected excerpts from the company's last four earnings calls that detail the company's progress which led to its inflection point moment last week.

Mark Zuckerberg made the following comments during the company's Q3, 2012 earnings call:

"Let's start with mobile. I think our opportunity on mobile is the most misunderstood aspect of Facebook today. Most people underestimate how fundamentally good the trend towards mobile can be for Facebook. This is because there are three trends that are kind of compounding together. First, mobile will give us the opportunity to reach way more people than desktop. Second, people on mobile use Facebook more often. And, third, long term, I think we're going to monetize better per amount of time spent on mobile than desktop. All of these combined together make mobile a much larger opportunity for us than I think most people realize."

From the Q4 call, a more upbeat Zuckerberg provided investors with a more bullish assessment of the company's mobile strategy and progress:

"Let's start with mobile. I think more people are starting to understand that mobile is a great opportunity for us. Mobile is the perfect device for Facebook. Mobile enables many new experiences, and its growing overall sharing across all apps. This creates a very dynamic ecosystem, and one where there's a lot of room for us to create even more sharing through Facebook. In December, we released a completely rewritten version of Facebook for Android. By improving speed and stability, we've made a much better user experience enabling people to share even more."

From Sheryl Sandberg during the Q1 call:

"Marketers are realizing more and more that Facebook is one of the best places to reach their customers on mobile because of our unique ability to reach specific target audiences at scale."

Last Week's Q2 Call:

"When it comes to mobile, I'm very pleased with the results. We now have more daily actives on mobile than on desktop. Nearly half a billion people use Facebook on their phones every day and soon we'll have more revenue on mobile than on desktop as well."

From being misunderstood four quarters ago, to becoming the biggest growth driver for the company, Mark Zuckerberg and his management team have figured out what most other companies have not: it has begun to successfully monetize mobile in a very big way. This should prove to be a boon for all shareholders.

Forward Estimates and Price Targets Will Trend Higher During the Next 2-3 Quarters

Currently, the mean target on Facebook is $37. Goldman has the highest target on the Street, however, at $46. Goldman's street-high price target will spur aggressive institutional interest in the mid-$30s.

Looking further out, we expect these price targets to move higher as the company's mobile advertising revenues surprise to the upside in both Q3 and particularly in Q4.

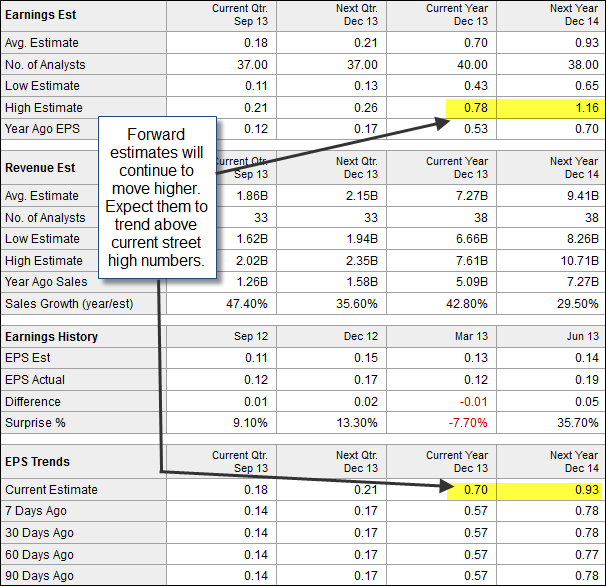

We therefore view consensus estimates for the next six quarters as too low. We expect current estimates to move up to the street high estimates, which call for almost 50% revenue growth to $7.61 billion in revenues, along with earnings of $0.78, or 50% year-over-year.

FB Consensus Estimates

(click to enlarge)

2014 numbers should eventually trend higher also. To this end, we expect FB to post $11-$12 billion in revenues, along with $1.25 in earnings in 2014. As forward estimates trend higher, institutional interest will swell.

Risks

While the next three quarters map out very well for Facebook, there are risks investors should also be mindful of. The most obvious one is that mobile experiences some speed bumps. Considered not cool anymore by teenagers, Facebook's mobile growth could slow down if advertisers pause on increasing spend due to concerns that teenagers are spending more time on other sites.

Facebook also runs the risk of monetizing mobile too aggressively, perhaps causing some subscribers to not engage with mobile ads like they did since being introduced.

Final Thoughts

Having noted these risks, at current levels, we believe that Facebook's shares represent a wonderful asymmetric trade for the next 3-9 months.

After seeing its stock advance 30% in one day on a 1,100% explosion in its volume on Thursday, we see minimal downside risk in Facebook's stock. With its stock a must own for many new levels of institutional shareholders, its shares should see impressive support in the $32.50-$34 zone in the next few weeks.

An immediate follow-through move to $36-$37 should be at hand by the end of next month as new institutional holders have to raise their bids to get the stake they are looking for in FB's shares.

After an expected above $40 into year-end, an explosive beat in Q4 early in 2014 should propel Facebook's shares to all-time highs by next spring.

As a testament for our high level of conviction in this trade idea, as of the close on Friday, Facebook was our largest position for the accounts we oversee.

No comments:

Post a Comment