By stockRiters - Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Thoratec Corporation (THOR) is a market leader in developing mechanical circulatory support (MCS) for patients suffering from end-stage cardiac heart failure (CHF). The company uses rotary pump technology as a primary method to develop these support devices. This is a mechanical assistance technique for circulation that is used to support patients suffering from cardiac disease.

Historically, heart transplantation is one of the standard methods for approaching end-stage heart disease. But the market has significantly changed to alternative therapies such as the Left Ventricular Assist Device (LVAD) since the FDA approval of Thoratec's HeartMate II in 2008. HeartMate II is used primarily as a destination therapy and a bridge to transplants.

Market overview:

The incidence of heart failure continues to increase worldwide due to the limited treatment options available for end-stage heart failure. Currently, heart transplantation is the only therapeutic option available in the market as the survival of patients through oral medication is minimal. In addition, patients are facing problems while looking for transplantation, due to the continued imbalance between demand and supply, which results from a shortage of donor organs. Also, the increasingly aging population and the higher mortality rate force patients to look for alternative therapies such as Cardiac Assist Devices (CAD).

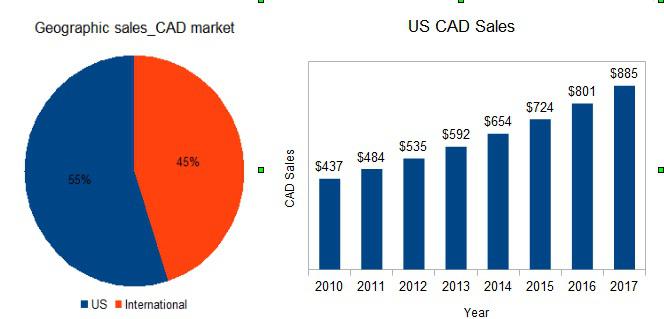

According to research from GBI, the global CAD market is likely to be $1.4 billion by 2017, with a CAGR of 8.6% from 2010-2017. The US alone comprised 55% of this market during 2010. It is expected to be $882.3 million at a CAGR of 10.6% by 2017.

(click to enlarge)

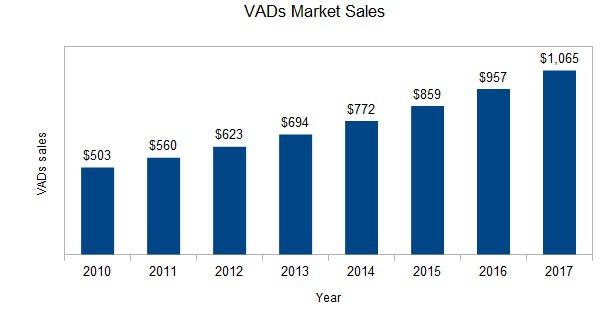

The global CAD market comprises of three segments: Ventricular Assist Devices (VAD), Intra-Aortic Balloon Pumps (IABP) and Total Artificial Heart (TAH). Besides transplantation, VADs are one of the emerging segments globally in the devices market for heart failure patients. This segment comprises 63% of the global CAD market, with a value of $503.2 million in 2010. It is expected to be $1.0 billion in 2017, growing at a CAGR of 11.3% during 2010-2017. This segment continues to be the largest in the MCS market because of its clinically proven, effective and safe approach to treating cardiac patients.

(click to enlarge)

The LVAD has changed the therapy significantly in the end-stage heart failure segment, despite higher costs compared to standard transplantation. However, the positive outcome from VADs implants and an alternative option due to organ shortage will create an opportunity for these devices. According to The American Association for Thoracic Surgery, the mortality rate reduced significantly due to the LVAD therapy. Furthermore, the increasing adoption of technologically advanced devices by physicians will drive demand for LVADs in the future.

Product lines:

Thoratec designs, develops and distributes products worldwide in two categories.

Chronic circulatory systems: The key products include the HeartMate LVAS (Left Ventricular Assist System) and the Thoratec VAD (Ventricular Assist Device). HeartMate is an implantable, electrically powered, continuous flow LVAD. It is designed to improve the survival and quality of life of advanced heart failure patients. Thoratec Paracorporeal Ventricular Assist Devices (PVAD) are external devices whereas Thoratec Implantable Ventricular Assist Devices (IVAD) are implantable devices mainly used to help patients recover after heart surgery.

Acute circulatory systems: Both CentriMag and PediMag/PediVAS are surgical support systems used in adult and pediatric patients respectively during cardiac surgery.

Competitive landscape:

Currently, Thoratec competes with MAQUET GmbH & Co, Teleflex Incorporated, HeartWare International, and Berlin Heart GmbH in the CADs market. It represented 48% of the global CAD market during 2010. In the VADs segment, Thoratec competes primarily with two major players, HeartWare and Berlin Heart respectively.

In 1Q13, HeartWare International (HTWR) reported sales of $49.2 million, which is an 87% rise compared to 1Q12. The significant increase in sales is due to the commercial launch of the HeartWare Ventricular Assist Device (HVAD) in November 2012 and continued rise in volume in both the U.S. and international markets.

Thoratec lost its market dominance with the launch of competitive products for bridge to transplant indication. This is evident from a decrease in sales of HeartMate and Thoratec during 1Q13.

The company reported sales of $117.1 million, an 8% decline compared to 1Q12, which is partly offset by the 20% increase in sales of the CentriMag product lines, which contributed $10.4 million.

During 1Q13, the company reported US sales of $92.3 million and $25.4 million in international sales. The growth in international sales was due to the rise in sales volume compared to domestic sales during the same period.

(click to enlarge)

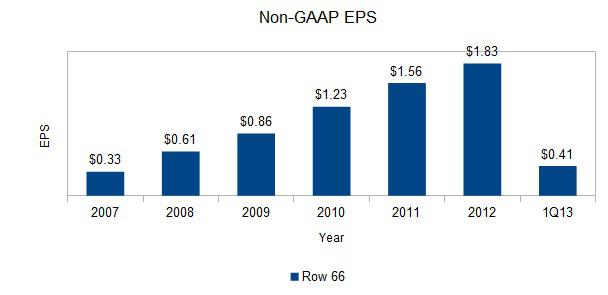

Thoratec reported a non-GAAP net income of $24.0 million in 1Q13 compared to $30.6 million in 1Q12; and GAAP net income of $18.2 million in 1Q13 compared to $25.5 million in 1Q12. The same is reflected in their non-GAAP EPS of $0.41 compared to $0.51 during 1Q12. This decline is due to a decline in top line growth. While looking at the company's historical trend, Thoratec has shown a significant growth (non-GAAP EPS CAGR of 41% from 2007-2012) in the last 5 years.

(click to enlarge)

Pipelines:

Currently, the company is focusing on developing products in HeartMate II and next generation pumps. In addition, Thoratec does have two pipeline studies for CentriMag® VAS and BeneMACS Long-Term LVAD.

CentriMag® VAS is a device that will support patients with cardiac dysfunction, and BeneMACS Long-Term LVAD study primarily aims to improve the survival in non-transplanted patients who are implanted with HeartMate II LVAD as destination therapy.

Recently, the FDA approved the HeartMate II Pocket Controller which is a compact version of HeartMate II LVAD. This device helps support patients with an active lifestyle.

Future outlook:

Thoratec had a disappointing performance in 1Q13 due to the decline in domestic sales, especially in destination therapy indication. Under a long term prospective, it continues its focus on product development and geographic expansion opportunities in the HeartMate II segment. This is evident from the recent FDA approval of the HeartMate II Pocket Controller, positive sales growth in the international market and a franchise approval in Japan for HeartMate II.

Furthermore, continued focus on next generation rotary pumps (HeartMate III & HeartMate PHP), and the introduction of new technologies to enhance MCS therapy is likely to provide growth potential in the future. I believe that the company will have an upside potential with a significant EPS growth trend in the long term.

Conclusion:

Thoratec has a strong portfolio with clinically differentiated products in rotary pump technology. The company continues to maintain its performance in both the domestic and international market despite a decline in sales in the current quarter. Furthermore, the positive clinical trial results for novel products with advanced technology, especially in the HeartMate II product line, will drive the demand for LVADs in the coming years.

No comments:

Post a Comment