Why Invest In Dividend Stocks? A Review Of Recent Research

Disclosure: I am long COP, INTC.

Over the last two years, I have come to embrace dividend growth investing [DGI], based on academic research showing superior returns from a DGI strategy and my own experiences with my model and personal portfolios. It has been a while since I searched for new research on DGI, so I went to Google and was surprised with what I found - several reports on the benefits of dividend stocks and DGI, supported by research and authored by asset management firms. I wasn't sure whether to congratulate them on finally "seeing the light" or to be worried that even asset management firms were now joining the DGI crowd. Of course, this doesn't change the concepts of asset allocation for them; it just influences the equity component.

Anyway, there was a lot of really good information and supporting data, which I will attempt to highlight and summarize in two articles. I strongly recommend downloading the reports from the provided links and reading through them, as I can't cover everything nor give the level of detail that is in the reports. This article focuses on the historical data and trends that support investing in dividend growth stocks, based on reports from BlackRock, Columbia Management, and Eagle Asset Management.

Benefits of Dividends

Let's start with what most investors in this forum already know. Dividend stocks are typically more mature, stable businesses that can afford to share profits with shareholders. Dividends serve as an important component of total return, accounting for approximately 40% of U.S. stock market returns since 1930. Sustainable and growing dividends help to hedge the income stream against inflation, to provide growing income to investors without the need to sell shares, and to signal strength to investors. These firms generally exhibit lower stock price volatility, while delivering attractive and even superior returns. Now let's get into more detail on a few of these benefits.

Inflation Hedge

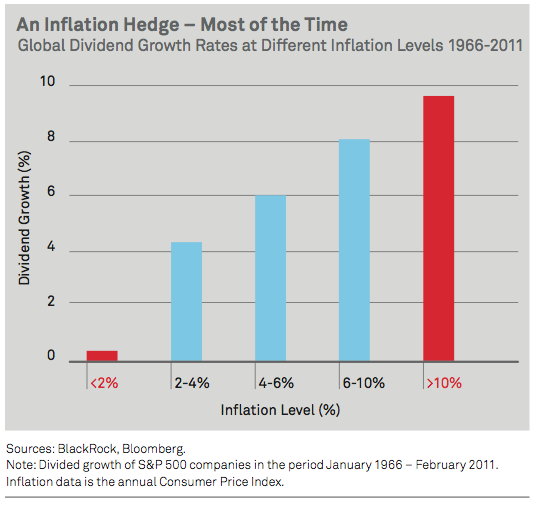

(click to enlarge)

Eagle Asset Management [EAM] found that dividend-paying equities have historically generated income that kept pace with inflation, but what happens in high inflation environments? BlackRock examined the dividend growth of S&P 500 companies for a 35-year period and found that on average, firms were able to pass on inflationary costs to maintain earnings and raise dividends. As observed in the graph above, when inflation was between 2% to 10%, dividend growth kept pace. It lagged when inflation was very low or very high, but in the latter case, the average increase was still pretty close. Many dividend growth investors prefer stocks with higher dividend growth rates [DGRs], and I would expect these firms to raise their dividend more than the 0.5% in the graph for low-inflation periods. Firms such as Target (TGT), Conoco (COP), and Teva Pharmaceuticals (TEVA) come to mind, which have had double-digit DGRs over the last decade.

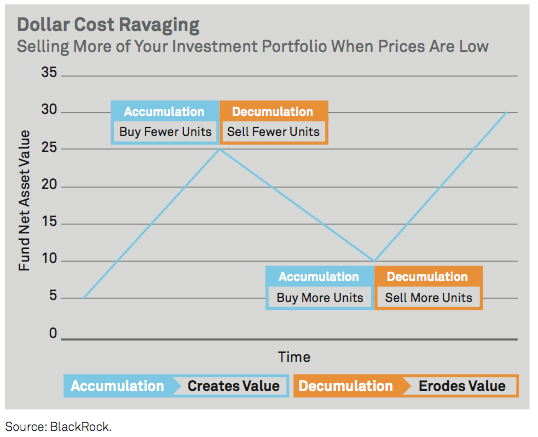

Avoid "Dollar Cost Ravaging"

(click to enlarge)

Dividend investors frequently mention the benefit of automatically receiving income without having to sell shares of their stocks, avoiding so called "homemade dividends." I chuckled when I saw the term "dollar cost ravaging" in the BlackRock report, which is a play on dollar cost averaging. With the latter, an investor investing a fixed amount each period purchases more shares when the price is lower and fewer shares when the price is higher. This helps to give the investor a lower average cost per share over time. "Dollar cost ravaging" is the opposite. An investor sells shares to receive a fixed, or more likely increasing, amount of cash each period. He will sell fewer shares when prices are high, but more shares when prices are low which erodes value. By providing an income stream, dividend stocks avoid the need to sell shares in a down market; assuming the dividend is not cut. For both cases, long-term results are dependent on earnings, but the dividend stockholder can ride out short-term price fluctuations without selling off shares.

Historical Performance

Through its analysis, BlackRock concluded that dividend growth stocks historically outperformed most other asset classes in periods of low or no economic growth, which reflects our current environment. EAM noted the superior performance in the U.S. of dividend payers over non-payers in both bull and bear markets. There is likely some bias in these results, as a stock that starts paying a dividend would shift to the dividend-payer category, but this still speaks very well of dividend paying stocks. Some other highlights from the EAM research:

- From 1980 to 2005, S&P 500 dividend payers outperformed non-payers by more than 2.6 percentage points per year.

- S&P 500 Dividend Aristocrats beat the S&P 500 Index over the last 1, 3, 5, 10, 15, and 20-year periods as of March 31, 2012, with lower volatility as measured by standard deviation.

- Dividend payers have been shown to outperform non-payers in a range of different interest rate environments. I found this item reassuring, as we are in a historically low-rate environment now, and eventually rates will tick upward.

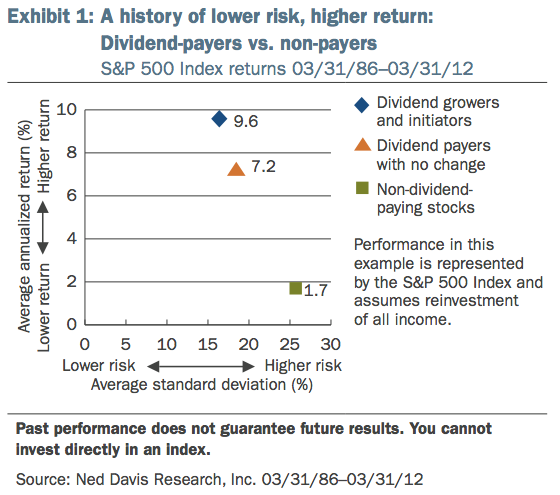

Columbia Management cited Ned Davis Research (see graph above) showing that from 1986 to 2012, dividend payers and growers outperformed non-payers by an even larger margin and with lower volatility. Again, there's probably some bias due to stocks shifting from the non-payer to dividend categories, but I'll take a 7.2% to 9.6% long-term average return!

Dividend Growth

A Societe Generale study, cited by BlackRock, found that dividend growth was the single largest contributor to nominal returns in key developed markets over the past 40 years. Growth in dividends appears to be a long-term trend.

- The S&P 500 companies have collectively paid out a higher amount of dividends in 83 of the past 100 years.

- From 1950 to 2010, 18 of 19 countries sampled in a London Business School study recorded real dividend growth, averaging 2.3% annually as a group.

- From 1970 to 2002, when dividends were "out of favor," S&P 500 Index stock dividend payments increased around 8% annually, increasing every year except 2000-2001.

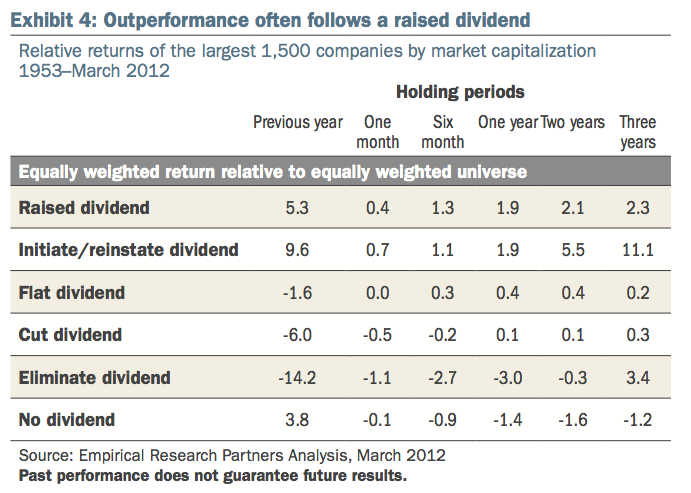

Consistent dividend growth helps the investor's income stream keep up with inflation, and allows for excess income to be reinvested at a comparable yield, unlike fixed income bonds, whose yields have declined. In addition, Columbia Management provided the table above showing that stocks that initiate or raise a dividend outperform those that cut, freeze, or raise a dividend that outperforms those that cut or freeze a dividend or that pay no dividend. The outperformance spanned the time from one-year before the raise to three years after, with the exception of the dividend elimination group in the third year. Assuming dividend growth investors held those stocks before the cut, they would likely still be underperforming over the entire timespan for the dividend elimination category. This is encouraging data for DG investors!

High-Yield, High DGR Sub-Group

The current CCC lists from SA contributor David Fish contains 470 dividend growth stocks that have raised dividends at least 5 consecutive years. The research identified two sub-groups of DG stocks that delivered higher returns compared to other sub-groups. The CCC list can easily be filtered to identify these stocks and to focus due diligence efforts.

(click to enlarge)

BlackRock highlighted high-yield, high-dividend growth stocks as a sub-group that provided superior returns over the 1988 to 2011 time period. This research used a world index, not just U.S. stocks. This supports previous research that I used to create my high-yield, low-payout model portfolio. The dividend growth rate is one of the variables factored into the screening and selection process for all of my models. The current DG-HYLP portfolio has average DGRs ranging from 15% to 20% for the last 1, 3, 5, and 10-year periods. Firms such as Hasbro (HAS), Lockheed Martin (LMT), and Intel (INTC), which yield over 4% and have double-digit DGRs over the last decade, are part of this group.

High-Yield, High-Quality Sub-Group

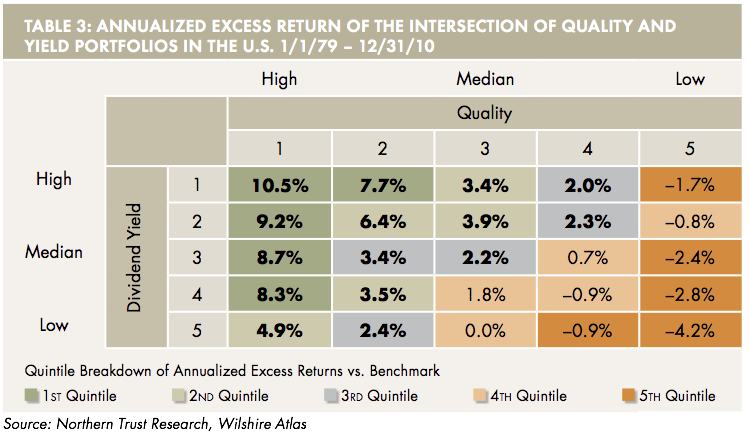

Northern Trust published a very thorough white paper describing their process and rationale, sans some key details, for developing a high-yield, high-quality portfolio. They began by looking at these two characteristics in isolation, dividing stocks into quintiles and analyzing the excess return in each group. They then created an intersection of these two traits; the results are in the table below.

(click to enlarge)

We can observe a clear jump in excess return in the darker green boxes, and choosing a top quality stock appears to be the more important factor. Northern Trust defined quality as "a function of various fundamental attributes that measure a company's ability to sustain and grow its earnings and cash flow." They created their own scoring metric to gauge quality, looking at management, profitability, and cash aspects of the business, and proceed to give some description of what they considered. While we don't know their exact system, I think investors can evaluate a firm's earnings and cash flow quality enough to stay away from the low end of the scale, and hopefully to identify firms closer to the top end. Northern Trust also backtested foreign stocks, and interestingly, high yield had more influence than quality, and these portfolios also had higher volatility.

Summary

To recap, the research cited in these asset management group articles provides a lot of supporting data for many of the reasons that investors have for following a dividend or dividend-growth strategy including: strong performance with lower volatility, protection of the income stream from inflation, and avoiding "homemade dividends" from the sale of shares, particularly during down markets. As a total return DGI investor, I really liked seeing the different studies showing dividend stocks outperforming non-payers and non-growers, and dividend growth as a key driver of outperformance. The high-yield, high-quality subgroup that delivered the highest returns at the lowest volatility drove home the need to remember the importance of investing in strong, high-quality firms, not just those with high dividend yields.

Sources:

BlackRock Investment Institute (March 2012). Means, Ends, and Dividends: Dividend Investing in a New World of Lower Yields and Longer Lives.

Eagle Asset Management (June 2012). Dividends Deliver: Dividend-oriented investments can offer much more than income.

Columbia Management (April 2012). The Tip of the Iceberg for Dividend Stocks.

Northern Trust (August 2012). Quality, Dividends, and Portfolio Application.

No comments:

Post a Comment