Buy Impax Labs Before The Rytary IPX066 Train Leaves The Station

October 1, 2012 | about: IPXL

I was amused this week when two financial firms with broad name recognition came out within days of each other and gave contradictory recommendations on Impax Labs (IPXL). First, Guggenheim, headquartered in New York and managing $160B in assets, arrived on September 18th and initiated coverage on Impax Labs with a "Buy" rating and a target price of $30 per share.

Then on September 25th, Think Equity, based in San Francisco and specializing in the managing of Initial Public Offerings including Angie's List and Zillow, downgraded Impax from "Buy" to "Hold" with a target price of $25. So, who's right?

Before we get to an answer, we need to understand a few important things about the biotechnology sector and pharmaceutical companies in particular.

There are very few profitable pharmas ,and Impax Labs is one of them. Perhaps this explains the predominance of institutional investors, which comprise 80.7% of the outstanding shares. Having said this, the sector is a bit of a quandary considered at once riskier than most and a safe haven as well. It's safer because regardless of how well the rest of the economy appears to be doing, the cost of medicine continues to rise. It's riskier because most pharmas are in a perpetual state of research and when they do develop marketable assets, they can never rest on their laurels. Newer and better drugs will always enter the marketplace, existing drugs will have unforeseen consequences with costly ramifications, and unless a company is focused on the future their progress will be overtaken by their past.

With so much in flux, evaluating the worth of any pharmaceutical company is problematic. To do so fairly, one must first ascertain if the company is in good financial health. And then, most importantly, one must be able to affirm that said business is growing in provable and pragmatic ways.

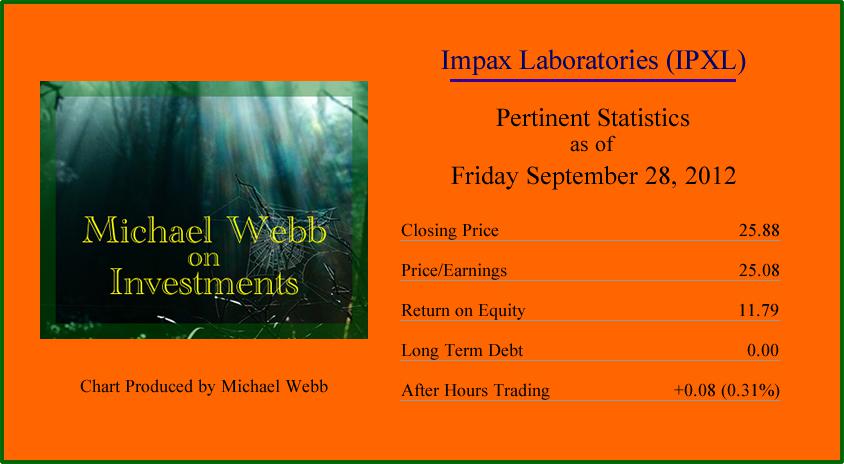

(click to enlarge)

Impax Labs is a specialty pharmaceutical company and is profitable is a very unique way. Headquartered in Hayward, CA, Impax differentiates itself from other pharmas through the application of its proprietary technology that allows it to produce controlled-release versions of brand named products without infringing upon the product-maker's patent - think Flomax, Wellbutrin XL and Aderal XR. The latter produced $70M of Impax's $166M in Q2 revenue this year. Impax has 118 of these generic formulations delivered world-wide through their Global Pharmaceutical Division and alliance partnerships. Impax has over a half billion dollars in yearly revenue, $354M cash on hand, and no short or long-term debt.

Impax has a very bright financial future with four catalysts for near and long-term growth.

- In February of this year, Impax entered into a licensing agreement with AstraZeneca for the exclusive U.S. commercial rights to Zomig in both tablet and nasal spray formulations. Quarterly payments this year totaling $130M and tiered royalties on future sales will have to be paid, but are more than offset by $163M of sales in 2011. Zomig patents expire in 2021.

- 46 Abbreviated New Drug Applications, of which 9 of these have first-to-file or first-to-market potential, along with 52 ANDAs under development position Impax for sustained long-term profitability. In total, these future opportunities in both branded and generic sales represent $36B in current annual U.S. sales.

- Recent settlements with brand name manufacturers have allowed Impax to develop and/or license to sell controlled-release versions of hugely popular drugs including Concerta, Renagle and Renvela. Revenue streams from these drugs will commence in the second half of 2013. If anything like the relative profit margins for Aderal XR, these could be as high as $250M annually.

- Most importantly, Impax has its own branded name division with two blockbuster products in the making - the most important of which is Rytary, with an FDA application name of IPX066

Hayward is one of two manufacturing facilities and remains part of the Rytary application. Dr. Hsu believes that the hiccup in Hayward will not effect Rytary approval in that the site can be removed from the application by negotiation if necessary. I'm not so sure I agree, however, and find that conclusion to be speculative. The other Impax production facility is located in Taiwan, and is presently being expanded to nearly double its current capacity. That construction is expected to be completed in mid-2013, and would be suitable for Rytary manufacturing.

So why is Rytary so important? It's key to Impax because it represents a blockbuster brand name product of their own creation. It's pivotal to investors because it's a near sure catalyst for stock appreciation leading up to its FDA approval date of October 21, 2012.

You see, thousands of investors are making double and triple digit profits a dozen or more times each year on a phenomenon know as the FDA Calendar Run-Up. What is it? The graphic below gives you a perfect example, but suffice it to say that every medicinal product on offer from every manufacturer must gain the approval of the federal government through the Food and Drug Administration. This multi-step process includes an application, three trial phases and the final approval deadline known as the PDUFA date - named after the regulatory law itself - the Prescription Drug User Fee Act. Almost on cue - two to four weeks before the approval, the candidates stock begins to climb. The ascent is generally more pronounced for smaller pharmas and more nuanced for larger ones. Impax, though substantial and profitable is still toward the smaller end of that spectrum.

(click to enlarge)

Impax has an October 21st PDUFA date for Rytary, which is a patented extended-release formulation of carbidopa-levidopa for the treatment of idiopathic Parkinson's disease. Phase III trials showed significant clinical benefits with fewer side-effects for Parkinson's patients.

Impax has wisely chosen to concentrate its branded name division on developing controlled-release solutions for unmet needs in the treatment of Central Nervous System disorders. This is the largest therapeutic category in terms of prescriptions and product sales in the U.S. health care field. Rytary is just the beginning. IPX059 is in Phase IIb trials for the treatment of Spasticity in patients with Multiple Sclerosis.

In conclusion, I can't hide the fact that I'm bullish on Impax Labs. With a broad range of profitable products, a proprietary way of manufacturing them; an extensive pipeline worth untold millions, an aggressive management and blockbuster near-term catalyst in Rytary, I'm left with little room to feel or choose otherwise. The unresolved warning letter from the FDA regarding the Hayward production facility allows me to understand Think Equity's position on valuation. Regardless, it would be foolish not to consider Impax Labs a long-term position because with more quantifiable catalysts going for it than a water balloon on the back porch of a college dormitory in the waning days of summer - Guggenheim has got to be right about this one. Plus, face it - you gotta love their name!

By Michael Webb

Disclosure: I am long IPXL.

No comments:

Post a Comment