3 Offshore Drilling Companies Poised To Deliver Strong Growth With New Rigs

Seadrill is the largest offshore drilling company in the world when measured by either market cap or enterprise value. As I discussed in a previous article, Seadrill has a history of delivering strong growth. In 2005, Seadrill had a modest fleet of five rigs. From those humble beginnings, it has grown into the industry-leading force that it is today. Seadrill operates a fleet of 67 modern offshore rigs that cover all of the different market segments in the industry, including the ultra-deepwater, shallow-water, and tender rig environments.

Seadrill has 48 rigs currently in operation around the world. The remaining nineteen rigs make up Seadrill's newbuild program and it is these rigs that will serve as the driver of Seadrill's revenue and profit growth going forward. These nineteen rigs make up a sizable percentage (28.4%) of Seadrill's total fleet. What is even more telling than this is the composition of this newbuild program. This newbuild program is made up of:

- Seven drillships. This is 63% of Seadrill's total number of drillships. The company has four drillships currently in operation.

- Two harsh-environment ultra-deepwater semi-submersibles. This is 14% of Seadrill's total number of semi-submersible units. Eight of Seadrill's twelve operating semi-submersibles are harsh environment units.

- Five jack-ups. This represents 23.8% of Seadrill's jack-up fleet. The company has 16 jack-ups currently deployed and generating revenue.

- Five tender rigs. This represents 23.8% of Seadrill's tender rig fleet. The company has sixteen tender barges and semi-tenders currently in operation.

Seadrill expects that its newbuild program will lead to powerful growth in the company's EBITDA. Seadrill's Board of Directors is confident that the company can achieve an annualized EBITDA of $4 billion once the company's new units are in operation. Seadrill's EBITDA in the second quarter was $634 million. Therefore, growing this to $4 billion annualized would represent a 57.7% increase by the middle of 2015. This estimate was made prior to the company's recent order of another drillship which has been considered in the above analysis. This could push EBITDA slightly higher, but one drillship will have a negligible impact on this $4 billion EBITDA figure.

Pacific Drilling S.A. (PACD)

Pacific Drilling S.A. is the successor company to a joint venture between Transocean (RIG) and Pacific Drilling Ltd. which was established in 2007 to own and operate two ultra-deepwater drillships. Eventually, the company realized that it could capture greater value by running its own rigs. As a result, Pacific Drilling is a very young company with a very modern fleet. When Pacific Drilling had its IPO in 2011, the company stated that it intends to remain focused solely on the ultra-deepwater environment and the company's fleet reflects this focus. Focusing on ultra-deepwater exclusively does have some advantages. In particular, ultra-deepwater drilling is perhaps the fastest growing segment of the industry; it is also a segment that has seen surging dayrates throughout the current upcycle. The company can also leverage this focus into securing better contracts due to its expertise in that environment.

Due to the time needed to build a drillship and Pacific Drilling's own youth, a large portion of the company's fleet is still under construction. This fact will allow Pacific Drilling to deliver strong growth over the next few years. Pacific Drilling currently has four rigs in operation and another three under construction. Thus, approximately 42.9% of the company's fleet is still being built! Additionally, Pacific Drilling announced last week that it has extended an option to begin construction on an eighth drillship. The company has until December 15, 2012 to exercise this option. Should it do so, the eighth rig in Pacific Drilling's fleet is expected to be delivered during the first quarter of 2015. This would double the size of Pacific Drilling's fleet. It would also have a similar effect on both revenue and profit, assuming a static environment for drilling rigs (which is not likely). Thus, fleet growth alone could potentially double Pacific Drilling's profit by 2015. Even if the company does not exercise this option, it still looks quite well positioned to see growing revenue and profit over the next two years.

Pacific Drilling has one of its three newbuilds already under contract at a dayrate of $555,000. The full contract rate is $590,000 per day, or approximately $215,350,000 per year. As discussed earlier, it is unlikely that Pacific Drilling will actually bring in the total amount of potential revenue. The company will more likely bring in 90% to 95% of it, or approximately $194,000,000 to $204,000,000 per year. If we assume that just one of these newbuilds receives a similar contract then this alone would represent a 32% increase over the revenue brought in during the latest quarter and that is just from one rig! Pacific Drilling has three (potentially four) of these rigs under construction. The growth potential here is clearly quite good.

Sevan Drilling ASA (SDRNF.OB)

Sevan Drilling was established in 2006 for the purpose of building ultra-deepwater rigs based on Sevan Marine's (SVMRF.PK) Sevan 650 rig design. Originally founded as a unit of Sevan Marine, the two companies ultimately parted ways with Seadrill buying Sevan Marine's stake in the drilling company. Sevan Drilling could offer the best growth prospects of any of these three companies. It is also the smallest firm that I am covering in this article, which adds its own set of risks.

Sevan currently has four ultra-deepwater drilling rigs in its fleet. Of these, two are deployed and operational and the remaining two are under construction. Thus, Sevan has the highest proportion of its total fleet under construction of any of these companies. The story goes beyond this, however. Sevan Drilling also has options to construct another two ultra-deepwater rigs. If these options are exercised, Sevan would have a fleet of six rigs with four under construction. Thus, Sevan is going to double the size of its fleet by Q3 2014. The company could triple its fleet size should the options be exercised. Sevan Drilling does not need to exercise these options to deliver a good return at these levels, however.

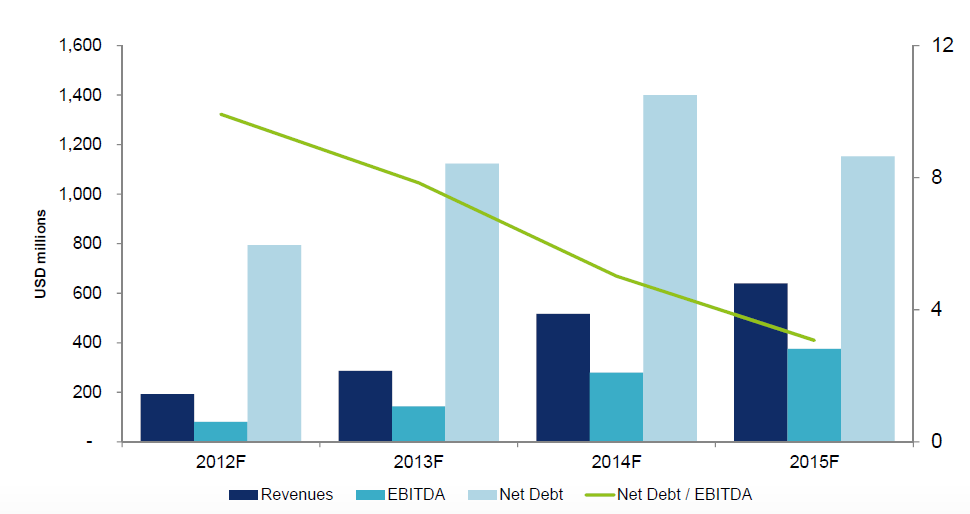

Sevan itself has provided very optimistic projects of its growth trajectory between now and 2015. Here is how the company projects its growth:

Source: Sevan Drilling

These are not overly optimistic or pie-in-the-sky projections either. Sevan Drilling actually looks like it can achieve this! Please note that this assumes that the company will not exercise those construction options that it holds. If it does, then revenues will be even higher, particularly in 2016. Perhaps even more impressive is the company's projected earnings growth. Sevan projected back in June that its annualized EBITDA would be around $280 million in 2014 and over $400 million in 2015. This assumes dayrates of $500,000 for the company's two newbuilds and rig operating expenses of $170,000 per day on each rig. Both of these numbers are quite reasonable, possibly even conservative.

Click to enlarge

Source: Sevan Drilling Investor Day 2012 Presentation

According to Yahoo Finance, Sevan Drilling had a market cap of $264 million as of market close on September 26. Thus, the company's market cap today is less than the firm's projected EBITDA in 2014, let alone 2015. This could be a sign that the stock is undervalued, particularly when we consider that less rapidly growing and larger offshore drillers are trading at much higher multiples to their projected forward EBITDA growth.

The graphic above illustrates one of the biggest risks with Sevan Drilling: The company has a very high level of debt relative to EBITDA, both current and projected. The company took on this debt to finance the construction of its fleet and so it is very similar to Seadrill in this regard. The company expects to begin to reduce its net debt once the fourth rig is delivered and it expects the total net debt to fall beginning in 2015. The company appears to be capable of carrying out this plan; however, potential investors would be well-advised to remain aware of the company's leverage.

Another risk is Sevan Drilling's exposure to Brazil. I discussed these risks in two articles recently:

- Transocean Barred From Operating in Brazil: Looking at the Potential Impact

- Did The Brazilian Courts Just Shoot The Country's Oil Industry in Both Feet?

A third risk is actually caused by the company's relatively small fleet size itself. An incident on one rig will have a large impact on the company's overall results. This very thing happened in April when repairs to Sevan Driller's BOP control line resulted in poor technical uptime during the second quarter of 2012. This would have had a much less sizable impact if the company had more rigs due to the presence of other rigs which assist in keeping the average up.

Additional disclosure: I am long shares of Sevan Drilling (SEVDR) on the Oslo Børs exchange in Norway.

No comments:

Post a Comment