TiVo Is On The Path To Replicate Virgin Media's Success In The U.S. And The Rest Of Europe

TiVo (TIVO) remains a significantly misunderstood stock that presents a greater than 50% potential upside for investors with a 12- to 18-month time horizon. Virgin Media's (VMED) Q2 earnings and conference call on July 24 revealed an unanticipated acceleration in growth of TiVo subscriptions from Q1. The improvement in subscription metrics is likely due to a shift in strategy at Virgin to bundle TiVo in most of its packages to middle and higher tier customers.

By the time TiVo reports Q2 earnings on Aug. 29, Virgin Media will contribute well over one million subscribers to TiVo's subscription base.

By the time TiVo reports Q2 earnings on Aug. 29, Virgin Media will contribute well over one million subscribers to TiVo's subscription base.To date, TiVo has been unable to clone Virgin's success with other operators both internationally and in the U.S. Many analysts and investors believed that Charter Communications (CHTR) was going to be the possible catalyst for subscriber growth in the U.S., but a recent change in the CEO position at Charter has led to uncertainty as to the precise path forward Charter will take with respect to TiVo. At the current stock price, TiVo presents a compelling longer-term value for patient investors.

Background

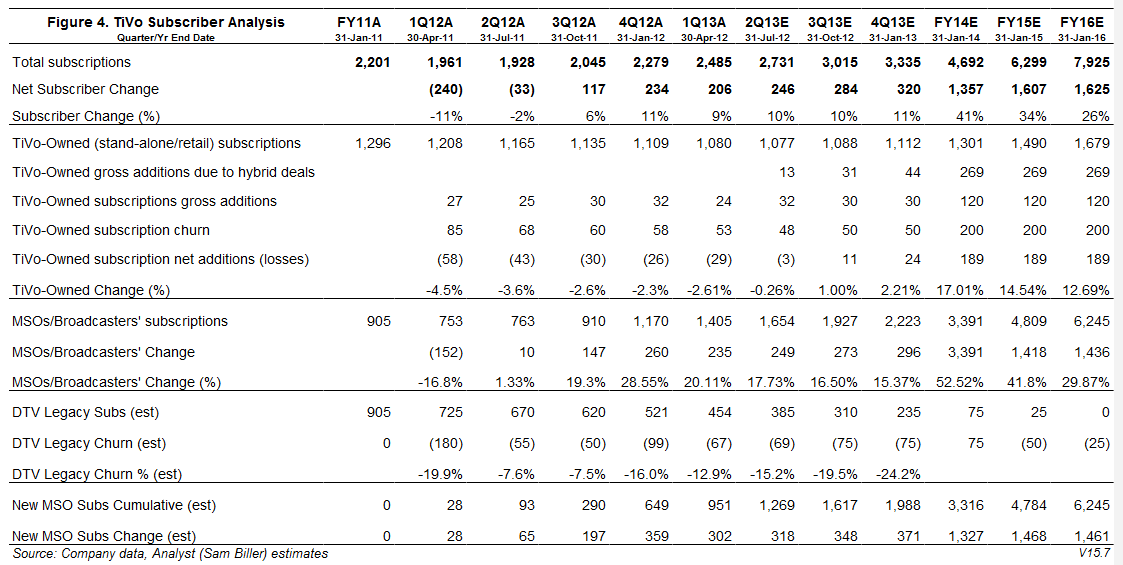

In February 2012, prior to its fourth-quarter report, TiVo was trading at levels 30% higher than today. An article I wrote back then suggested that TiVo presented a compelling earnings play not reflected in the stock price. The projected subscriber gain of 435,100 turned out to be significantly higher than the 233,000 net adds that were reported in Q4. DirecTV (DTV) legacy churn coupled with tepid growth outside of Virgin Media have required a closer examination of the fidelity of the subscriber growth model. The current model presents a more conservative and realistic forecast going forward for subscriber growth. TiVo's Q1 report released in May presented another opportunity for confirmation that a revised model more accurately reflects TiVo's subscriber growth prospects.

In the past six months, there have been a number of significant events enabling further adjustments to subscriber estimates, revenue forecasts, expense forecasts, and ultimately the future opportunities and risks for TiVo.

Subscriber Estimate Revisions

The subscriber revision table below (Figure 1) reflects disappointing roll-outs at Charter Communications, ONO, Suddenlink, and DirecTV contributing to a significant reduction in FY 2013 subscriber estimates.

Clearer Direction at Charter

During Charter Communications' Q1 2012 conference call, CEO Tom Rutledge was clearly evasive on questions related to TiVo. When Raymond James analyst Alexander Sklar asked Charter's CEO the following question:

Follow-up on the TiVo question, given what you were saying earlier on finding ways to improve existing boxes rather than spend on new equipment, does TiVo -- is TiVo still going to fit into the long-term plan or can you go all IP without it?Rutledge responded:

And your question about going all IP in terms of set-top boxes, there are TVs that are coming on market that are all IP or can take an IP feed, I guess, is a better way of saying it because they can take the regular feed as well. It creates an opportunity to have with cable system that both feeds IPTV and MPEG TV. And there are multiple variations of MPEG as well, which actually, from a technical perspective, are more efficient than IP from a total data throughput perspective. And our network, because of the server-based architecture that we've constructed, can serve multiple kinds of devices. So we can serve legacy set-top boxes with MPEG-2. We can create new hybrid boxes that are IP and MPEG using more efficient MPEG standards for server-based programming. And we can mix and match all of that in the same cable system, and there's enough channel capacity to serve all of those functions. So as I look forward, I think our Consumer Premises Equipment (CPE) evolution will result in a world where our incremental cost of CPE per customer will go down as we buy world-class CPE -- world vendor class CPE, and buy that in multiple formats. And so how that'll all evolve, I'm not sure, but the architecture that we've constructed allows us to follow the marketplace to its most efficient place.The key element of Rutledge's comments was related to hybrid boxes that are IP and MPEG. This foreshadows that Charter is moving away from the TiVo-provided Premiere set-top box to something else. In early June, Charter's shift away from the TiVo Premiere platform became even clearer when TiVo CEO Tom Rodgers revealed the following at a Sanford Bernstein conference:

Charter is the biggest relationship we have among U.S. operators. Charter relationship is good. We are in a good position to do something quite significant there. I sighted on the earnings call yesterday, Tom Rutledge, the new CEOs comments on the value of TiVo as an interface, our value proposition as something that can evolve going forward with future generations of implementation that they are looking at. The fact of the matter is that Tom Rutledge came to Charter with a very clear point of view that he wants to enhance the perception of the video offering of Charter and to do that is one of his top priorities. We've done a lot of work to be in a position with Charter to do just that and I think it will become apparent that we are playing that role.The bottom line for Charter is that it is not abandoning TiVo. It is just changing to TiVo software on MSO hardware that is more in line with its long-term strategy to reduce Consumer Premises Equipment and Capital Expenditures (capex) in the home. From a subscriber growth penetration perspective, this delays Charter adds until calendar year 2013 (TiVo's FY 2014), but we should see healthy adds in that time frame when Charter begins to roll out next generation solutions with MSO hardware running TiVo software. Charter has a very low penetration for video subscribers, so the upside is significant. There are risks to this roll out from a timing perspective since it relies on TiVo continuing to evolve its platform to run on a myriad of hardware platforms.

We look at the Charter relationship where we are all about the UI. Far less important about the hardware. Separate the role of user experience and UI with hardware. We provide hardware as a vehicle for operators to do that but its important as a faster way to move. We are very comfortable playing the role of building into other hardware. At the Cable Show last week we had a very positive reaction as people went from our booth to see the user experience and went next door to the Pace booth to see the user experience built into the Pace hardware and saw that you could combine what is perceived as best-in-class in user experience with what is viewed as the most efficient capex implementation in the Pace hardware and the combination of those really do hit a sweet spot that operators are focused on. That provides us a great way to move forward broadly with the cable industry.

Finally, on Aug. 7, Charter reported Q2 earnings and the conference call confirmed that it is not abandoning TiVo:

David Carl Joyce (ISI Group, Research Division): I was wondering how the TiVo box fits into your capex plan? Are you still committed to TiVo there? And given the product strategy, what's the prospect of the EBITDA growth in the second half?All of this adds up to the conclusion that Charter still does have the potential to duplicate the success of Virgin Media with TiVo software running on third-party hardware for a subscriber base that is larger than Virgin Media, with more growth potential and less competition.

Thomas M. Rutledge: Well, our commitment to TiVo is a commitment to their software actually. And we have a license agreement with TiVo to use their user interface, and we are using their user interface currently on boxes they provide. But as we go forward, our strategy is to use the user interface, both in the cloud and on existing CPE and on a new CPE.

Progress at Spain's ONO

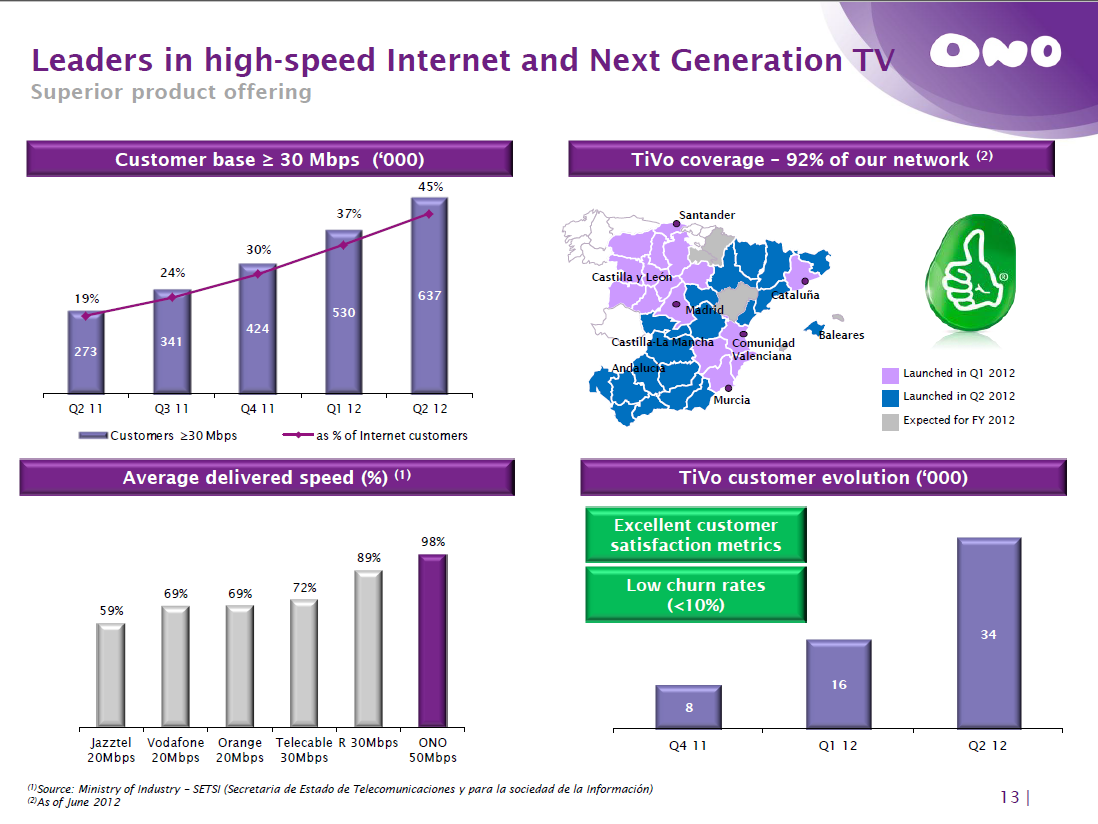

Spain's ONO quietly released Q2 2012 earnings on July 27 and revealed that TiVo subscribers have more than doubled to 34,000 even in an extremely challenging Spanish macroeconomic environment. More importantly, satisfaction and churn metrics associated with TiVo subscribers at ONO is significantly higher than for its other products. We expect growth at ONO to accelerate from this point forward since TiVo is now available to over 92% of ONO's customers, and a software upgrade has been released that brings the ONO platform in line with the offering to Virgin Media's customers in the U.K.

Click to enlarge images.

Significant Deal With Sweden's Com Hem

We believe that success at Virgin Media and ONO has led to a third significant deal in Western Europe for TiVo, which was announced in June: "Com Hem Creating Sweden's Smartest TV Service -- Signs Exclusive Agreement With TiVo."

Com Hem is significant for a number of reasons in addition to its 1.74 million subscribers. Com Hem is the first time TiVo will be deployed on an IPTV network similar to AT&T's U-Verse network in the U.S. This will be another foundational software upgrade that opens up the TiVo platform to more MSOs. Com Hem's goals sound very similar to Rutledge's goals at Charter -- offer the video service to their customers on many different devices while reducing CPE costs. Its worth noting what TiVo is joining with Com Hem in Sweden to be deployed in Spring 2013: from the PR:

Com Hem and TiVo will also enable this vast world of content choice for consumption beyond the traditional set top box through TiVo's tablet, smartphone, and browser-based experiences.Note the reference to "browser-based experiences." Tomas Franzen, CEO of Com Hem, stated:

We reviewed a number of alternatives to find the best way to offer our customers the absolute best television experience by providing a full suite of linear television services, VOD, and broadband delivered content (including OTT/pay services) to every room and device in and out of our customers' homes.This, in fact, is the direction that Charter is heading as well. They are shifting to an "all-digital" TV everywhere experience to every room and device. Finally, Com Hem is expected to launch next spring and will begin to add material TiVo subscriptions in late FY 2014.

Retail Trends Improving, Potential Turnaround on TiVo-Owned/Standalone Subscribers

One of the biggest challenges TiVo has that continues to trouble investors, analysts, and TiVo management is the trends in retail TiVo subscriptions. TiVo continues to invest in technology relevant to retail subscribers, but the availability of lower-cost OTT devices like Roku and Apple TV without a subscription and with better support for OTT services, coupled with the challenges of competing with generic cable operator DVRs, has resulted in continued losses of TiVo-Owned/Standalone subscribers quarter after quarter.

On a positive note, TiVo management revealed in the Q1 conference call that:

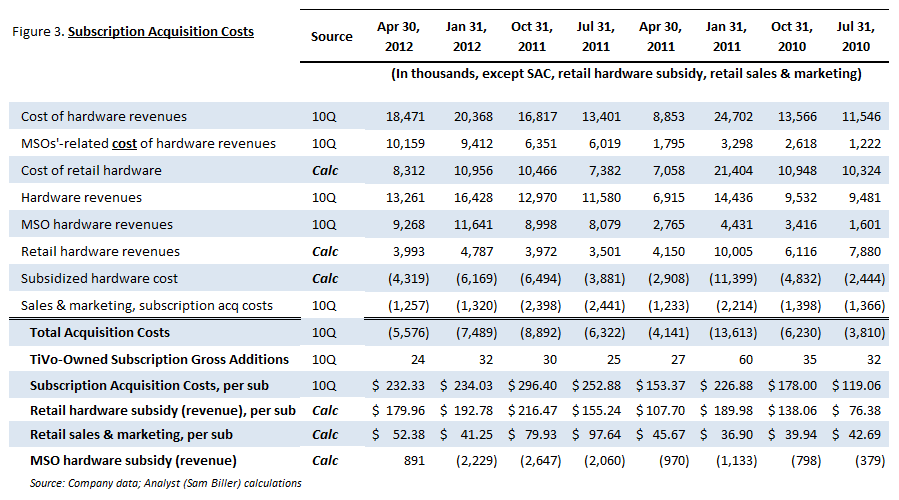

[I]n our TiVo-Owned business, we saw the lowest level of churn in well over six years. Retail gross additions for TiVo's Q1 ending 30 April 2012 were a disappointing 24,000 and retail hardware subsidy per subscriber was a significant $180 per subscriber. SAC costs per subscriber remains in the low $200 range meaning that it takes more than two years, assuming approximately $8 ARPU per retail subscriber, to recover the costs for each retail subscriber addition.Of note in table below is that TiVo actually subsidized the MSO cost of hardware in Q1, most likely due to pricing obligations with its MSO hardware partners and increased costs related to hard drive price increases. We expect those trends to once again reverse in Q2 and MSO hardware revenue to be a positive/neutral contributor to earnings.

TiVo also revealed that it was going to significantly increase marketing spend in Q2 in conjunction with support for Comcast (CMCSA) Xfinity On Demand in the San Francisco Bay Area and Boston/New England markets.

[W]e expect to see increased sales and marketing expense this quarter relating to promotion of our Comcast offering, which we believe has the potential to drive increased TiVo gross adds for fiscal year 2013 vs. 2012.So what does this mean for TiVo's retail subscription market in Q2 forward? We expect TiVo gross adds for Q2 to increase from the paltry 24,000 in Q1 to approximately 45,000 in Q2. With churn remaining relatively flat at 48,000 losses in Q2, we expect Q2 to be a close to break-even quarter for TiVo with respect to retail subscriptions. There are some risks associated with this prediction since TiVo has been silent regarding the success or failure of retail efforts in the San Francisco and Boston areas.

We do know that there has been a significant mass media marketing campaigns, including television, radio, billboards, and newspapers. These retail efforts may also have been improved by significant discounting on TiVo hardware including sales on TiVo's top-of-the-line Elite/XL4 model. Finally, going forward TiVo continues to hone its retail lineup to improve SAC and desirability to retail customers.

Bottom Line on TiVo Subscription Metrics

So what does this lengthy discussion mean from a TiVo MSO and retail subscription perspective? Our significantly revised estimates predict that TiVo subscriptions will grow a healthy 10% (246,000) in Q2, which is a significant improvement over the addition of 206,000 subscribers in Q1. We expect total subscriptions to be at 3.3 million at the end of FY 2013 (January) and 4.7 million at the end of FY 2014. This is very much in line with consensus analyst estimates for those analysts that have published subscriber projections for TiVo.

It's very difficult to estimate the impact of legacy DirecTV standard definition subscribers. We expect that the churn of legacy DTV subscribers continues to drag on total subscription adds. In fact, in TiVo's Q1 conference call management remarked that:

In terms of additions, our mass distribution deals contributed nicely during the quarter although it is worth pointing out that DirecTV standard definition churn still materially outpaced adds from the new HD platform.DirecTV continues to advertise its own superior receiver(s) over TiVo's crippled DTV receiver, so we don't expect this trend to improve for DTV. What's unclear and an estimate, since TiVo management doesn't reveal statistics related to individual MSO subscribers, is how much longer the drag of DTV will hamper TiVo growth. For Q2, we are estimating that DTV legacy churn as a loss of 69,000 subscribers, while DTV gross additions are in the range of 20,000 subscribers (i.e., net loss of 49,000).

Finally, the model now includes additional fidelity associated with TiVo retail additions due to hybrid deals like Comcast and retail subscription churn, which has been rather consistent for the past three quarters.

Improving Financial Trends

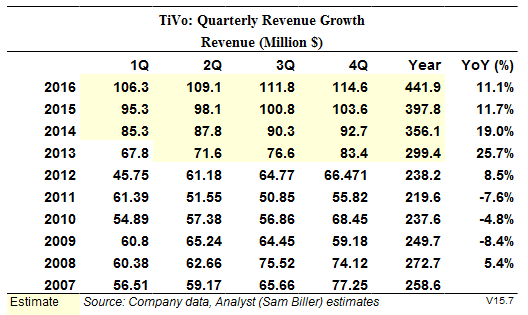

From a revenue growth perspective, we continue to expect double-digit growth even with the more conservative subscriber growth estimates and reduces MSO ARPU revenue expectations. The revenue model does factor in the possibility of a settlement in the Verizon litigation that goes to trial in approximately seven weeks.

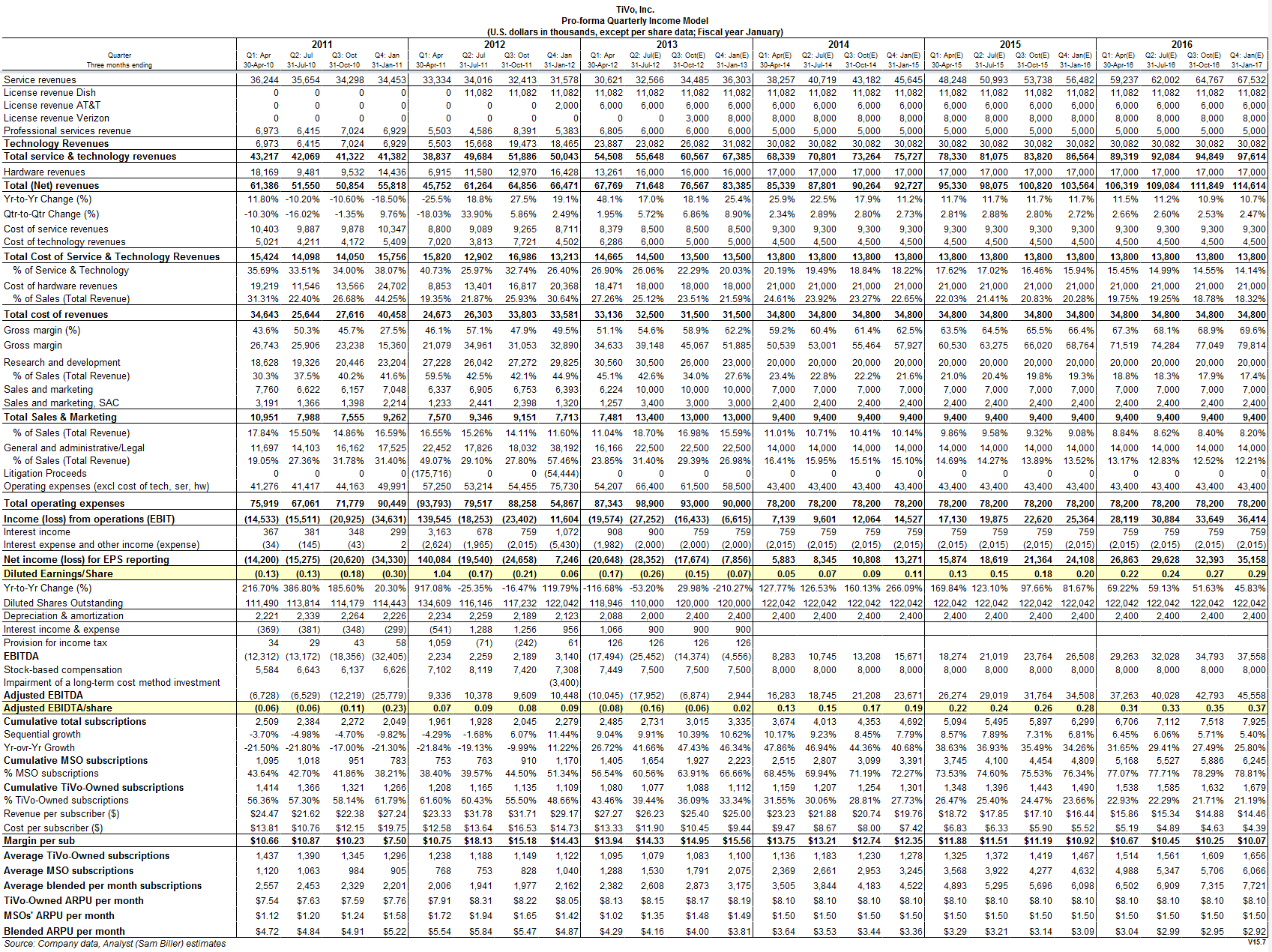

Another factor reflecting an improving financial picture for the company is operating margins. The detailed income model continues to present improving gross margins quarter over quarter driven by income increasingly received from MSO deals. Of note from the detailed income model is that EBIDTA profitability is achievable this year, but is dependent on a settlement in the Verizon case.

The overall EPS model continues to factor in the drag on earnings of continued litigation spend and high levels of research and development spending. With a Verizon (VZ) settlement, we do believe that TiVo will be EPS positive for FY 2014 even with continued litigation cases outside of Verizon.

All of these detailed models lead to a very simple conclusion -- TiVo is extremely undervalued at current levels and a price target of $15 within the next 12 to 18 months is very likely.

Risks and Opportunities

TiVo's standalone subscribers continue to shrink and retail deals with Comcast and Cox may not result in the subscriber gains anticipated. The Comcast deal has successfully launched in the San Francisco and Boston areas and additional markets are expected to be launched later this year.

TiVo has an unfavorable legal ruling. TiVo is currently involved in IP litigation with Verizon, Motorola, Time Warner Cable (TWC), and Cisco (CSCO). The Verizon trial is just weeks away with jury selection on Oct. 1, 2012. Odds favor either a settlement or a favorably ruling from the jury in the November time frame, but there are obvious risks associated with the trial and continued legal expenses associated with Verizon and other litigation. Motorola and TWC are scheduled for trial next year, while Cisco is in the early stages with a trial likely in 2014.

TiVo strikes a deal(s) with another major international or domestic partner. There are a couple of larger US MSOs (e.g., Cablevision, CableOne, etc.) still absent from the deal or litigation roster. On the international front, the landscape is much cloudier, but the market is very open based on TiVo's success with Virgin Media, ONO, and the deal announcement with Com Hem. I'm expecting we may see additional international deals later this year. TiVo's recent deal with Pace that is expected to yield TiVo software running on Pace hardware later this year has the potential to open up a much wider market for the TiVo software. Pace has the bandwidth and international experience to easily distribute millions of set-top boxes running TiVo software to their customers.

Failure to execute with a partner. TiVo has a number of new technology products in the pipeline and has a number of challenging MSO engagements being currently worked. They've been fairly successful at meeting their engineering milestones for the past few years, but these software intensive projects certainly have risks schedule, technical, and cost risks that are difficult to quantify.

TiVo is acquired. With its small market cap, compelling patent portfolio, and healthy balance sheet I wouldn't be surprised if TiVo remains on the radar screen of a couple of big cap players. I believe Cisco, Microsoft or Google (GOOG) are still the likely acquirers for TiVo -- although it's possible that Apple (a long shot) could acquire TiVo.

Conclusion

TiVo's stock price today (~$9.00) reflects a company that remains oversold and misunderstood. The risk/reward reflects a company with approximately $2.00 in downside risk and $5.00-plus in upside opportunity. More importantly, TiVo continues to be one of a few independent companies that offers a best-in-class software ecosystem to its MSO partners. TiVo's balance sheet reflects quarter-over-quarter improvement in all key metrics -- gross adds, net adds, churn, ARPU, gross margin, and revenue.

By Samuel Biller

Disclosure: I am long TIVO, VMED, CMCSA.

Source:seekingalpha.com

No comments:

Post a Comment