Oracle: Cheapest Pure Play On Cloud Computing Market

Oracle (ORCL) is the leading producer of enterprise software and a leading producer of computer hardware and products. On June 6, the company announced that it will be focusing its products and efforts on cloud computing namely through platform as a service (PAAS) via its operating systems and network setups, and software as a service (SAAS) via its fusion applications and other software. Oracle's main competitors have been SAP, Microsoft (MSFT), Google (GOOG) and Hewlett-Packard (HP). However, this group is somewhat late to the cloud computing market, so principal competitors will now include Salesforce (CRM) and Workday, and HP is now focusing on infrastructure as a service (IaaS). In brief, it appears that Oracle will have the ability to become a player in the promising market for cloud computing and is the least expensive way to gain exposure to this major trend.

Oracle operates in 3 distinct divisions: software, which includes new licenses and license renewals, hardware, which includes hardware systems and support, and services. Software has been both the fastest-growing segment and the highest-margin segment, with a growth rate of CAGR of over 10% and gross margin of 76%. It also makes up the majority (70%) of revenue. Hardware currently makes up approximately 17% of total revenue; however its growth rate has been negligible or negative over the past two years and should continue this way as companies move away from physical in-house servers. This business also had a relatively low gross margin of 40%. Services make up the rest of the revenue with a gross margin of around 66% and a growth rate around 5%. If this trend continues, Oracle will not only experience top line growth, but its bottom line will grow even faster in the future as software makes up a higher percentage of revenue. Given Oracle's stated focus on the cloud and SaaS, this appears quite likely.

Cloud computing is a fascinating market; I believe that it will become the standard because in comparison with physical servers in-house, cloud computing is cheaper in the short run through fewer upfront fixed costs and the long run through less over capacity, can be set up more quickly than a traditional server, and provides more flexibility, connectivity and efficiency. It also puts control of the networks in the hands of those who know them best: the companies that built them. There is still tremendous growth in the market as only 5% of IT professionals are currently on the cloud but 20% have plans to be on a cloud by the end of the year, and there are similar growth statistics into the future. According to Forbes, companies have upped their allocation to cloud computing in IT budgets to 34%. All of these provide the ingredients for a strong market. Additionally, this market may be so large and diverse due to IaaS, PaaS, and SaaS, that this market does not have to be a zero sum game. In other words, there can be multiple companies that will thrive due to the cloud computing market, and there will not be just one company that controls the market.

The growth of this market will come at the cost of the traditional server market. This is not a real loss to Oracle because it is no longer focusing on this area, and it provides lower margins. Although Oracle is late to the game to SaaS compared with Workday and Salesforce, Oracle's fusion apps appear to be a strong product and offer a wider range of services than these competitors. Even with Oracle's apps that compete directly with those of Workday and Salesforce, the breadth of the offerings provides distinct advantage: large companies that wish to have wide ranges of SaaS will not want to work through multiple companies to satisfy their demands but would prefer to keep all SaaS under one roof. This gives Oracle a distinct advantage. Oracle also offers simplicity to large customers because of its ability to integrate PaaS and SaaS. Salesforce and Workday do not offer this capability, SAP plays second fiddle to Oracle in this market, and the only company that has offerings that could match Oracle's would be Google, however Google's products are more directed at the consumers and enterprises.

Oracle in comparison with competitors has two major forces on its side: its sales team and inertia. Oracle's sales team has received criticism for being quite cutthroat; however it's difficult to argue with results and it has driven the growth of the company allowing it to lead the enterprise network solution market. More significantly, there are huge costs associated with switching hardware and software within a company. New networks are quite expensive while license renewals are much cheaper. The installation of a new network can take weeks or months causing a significant loss in productivity. Additionally, employees will have to deal with the unfamiliarity of the new system. This means that many of companies that will convert to the cloud will automatically default to Oracle because they currently have Oracle. This is especially true for many of Oracle's customers that are mostly large companies and government entities that are as technologically nimble as smaller companies. As cloud computing will have a heightened focus on software applications and not hardware, switching costs should continue to drive growth in Oracle's software segment, which will increase revenue and margins.

The company's balance sheet is solid. Net debt is around $1B, a paltry sum for a company this size. Yet it is not hoarding cash but rather reinvesting it into the company with large R&D ($4.5B) and Capex ($650MM). The company's cash flow situation is solid, as it has had cash flow growth each of the past 3 years, and 2 out of 3 periods had FCF growth of over 20%. FCF yield currently sits around 8.8% It has announced a $10B stock repurchase plan and pays a dividend of almost 1%. There is still plenty of money to reinvest in the business.

The relative valuation looks promising as seen by the chart below:

This is a good mix of companies: SAP is a principal competitor, Salesforce is an up and comer, and IBM is the stalwart. ORCL compares favorably with all. I really believe it is better to invest in a solidified force like Oracle as opposed to Salesforce. I will illustrate this with a thought experiment. For the company to double in 5 years it much achieve a 14%/year price appreciation. Were its P/FCF multiple not to compress it would have to grow its FCF by only 14% per year, which it has. However, as growth slows, its multiple would contract. Say it contracts by half, but still double that of ORCL. This means FCF must grow annually by 28% just to justify a 14% increase in price per year. This seems risky to me.

ORCL is also relatively cheap itself historically. Within the past 5 years its P/E ratio has ranged between 13.5 and 24.

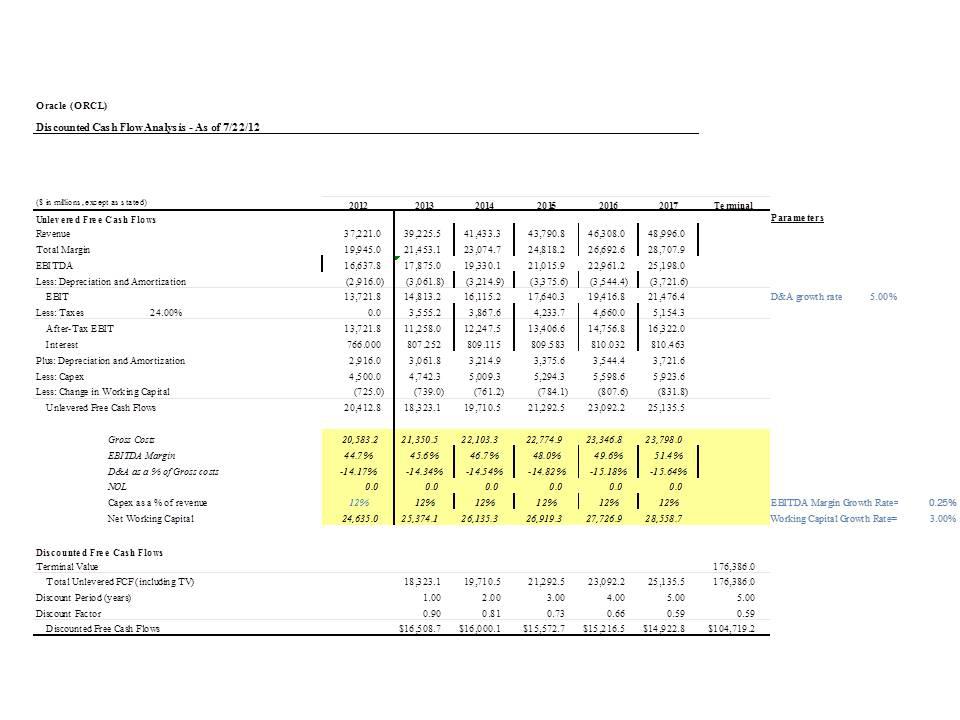

I also made a DCF to supplement this and the results are promising. Just for a base case my assumptions were as follows:

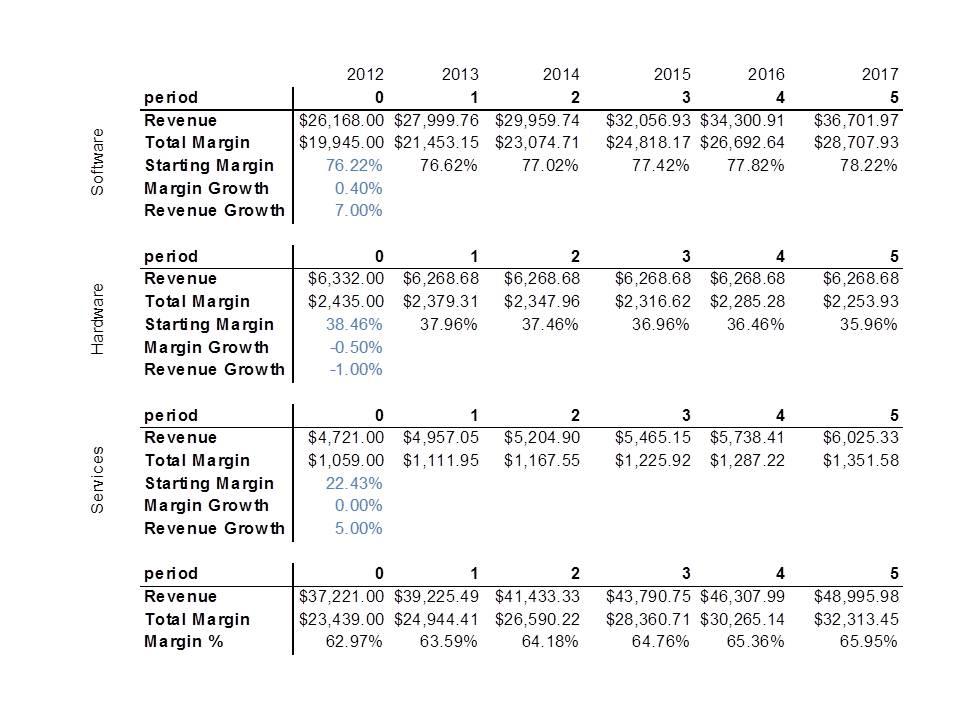

For software revenue:

For hardware revenue

For services revenue

I assumed EBITDA margin would grow slightly year over year because the company has shown a great ability to reduce SG&A expenses. However, EBITDA grows also because gross margin increases. This however depends more upon the revenue growth model. I incorporated this increase by adding the difference between gross margin yoy to the EBITDA margin. Using these assumptions, I backed out a share price of $43.93 and it is currently trading at $30.11. I believe my key assumptions for growth are conservative. Services revenue should rise as the number of subscribers grows but I grew it as less than software revenue growth. I included a contraction of hardware margin and negative growth here as this is a contracting industry. I particularly believe I am conservative with the software revenue growth as the industry is expected to grow faster than 7%, and Oracle has grown revenue faster than this. Also, as revenue switches to cloud based, margins should increase, and then increase more as revenue comes from license renewal as opposed to initial licenses.

In short, Oracle is a strong company well positioned to take advantage of the cloud market. It is not perfect as shown by the success of its competitors. But its size and history provide it with unique advantages. More importantly, ORCL appears to be trading at a discount absolutely and relatively. This makes ORCL a great opportunity to gain exposure to this market.

The results of my DCF can be seen below including a 5-year revenue model.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

By Christopher Bayliss

Source: seekingalpha.com

Oracle operates in 3 distinct divisions: software, which includes new licenses and license renewals, hardware, which includes hardware systems and support, and services. Software has been both the fastest-growing segment and the highest-margin segment, with a growth rate of CAGR of over 10% and gross margin of 76%. It also makes up the majority (70%) of revenue. Hardware currently makes up approximately 17% of total revenue; however its growth rate has been negligible or negative over the past two years and should continue this way as companies move away from physical in-house servers. This business also had a relatively low gross margin of 40%. Services make up the rest of the revenue with a gross margin of around 66% and a growth rate around 5%. If this trend continues, Oracle will not only experience top line growth, but its bottom line will grow even faster in the future as software makes up a higher percentage of revenue. Given Oracle's stated focus on the cloud and SaaS, this appears quite likely.

Cloud computing is a fascinating market; I believe that it will become the standard because in comparison with physical servers in-house, cloud computing is cheaper in the short run through fewer upfront fixed costs and the long run through less over capacity, can be set up more quickly than a traditional server, and provides more flexibility, connectivity and efficiency. It also puts control of the networks in the hands of those who know them best: the companies that built them. There is still tremendous growth in the market as only 5% of IT professionals are currently on the cloud but 20% have plans to be on a cloud by the end of the year, and there are similar growth statistics into the future. According to Forbes, companies have upped their allocation to cloud computing in IT budgets to 34%. All of these provide the ingredients for a strong market. Additionally, this market may be so large and diverse due to IaaS, PaaS, and SaaS, that this market does not have to be a zero sum game. In other words, there can be multiple companies that will thrive due to the cloud computing market, and there will not be just one company that controls the market.

The growth of this market will come at the cost of the traditional server market. This is not a real loss to Oracle because it is no longer focusing on this area, and it provides lower margins. Although Oracle is late to the game to SaaS compared with Workday and Salesforce, Oracle's fusion apps appear to be a strong product and offer a wider range of services than these competitors. Even with Oracle's apps that compete directly with those of Workday and Salesforce, the breadth of the offerings provides distinct advantage: large companies that wish to have wide ranges of SaaS will not want to work through multiple companies to satisfy their demands but would prefer to keep all SaaS under one roof. This gives Oracle a distinct advantage. Oracle also offers simplicity to large customers because of its ability to integrate PaaS and SaaS. Salesforce and Workday do not offer this capability, SAP plays second fiddle to Oracle in this market, and the only company that has offerings that could match Oracle's would be Google, however Google's products are more directed at the consumers and enterprises.

Oracle in comparison with competitors has two major forces on its side: its sales team and inertia. Oracle's sales team has received criticism for being quite cutthroat; however it's difficult to argue with results and it has driven the growth of the company allowing it to lead the enterprise network solution market. More significantly, there are huge costs associated with switching hardware and software within a company. New networks are quite expensive while license renewals are much cheaper. The installation of a new network can take weeks or months causing a significant loss in productivity. Additionally, employees will have to deal with the unfamiliarity of the new system. This means that many of companies that will convert to the cloud will automatically default to Oracle because they currently have Oracle. This is especially true for many of Oracle's customers that are mostly large companies and government entities that are as technologically nimble as smaller companies. As cloud computing will have a heightened focus on software applications and not hardware, switching costs should continue to drive growth in Oracle's software segment, which will increase revenue and margins.

The company's balance sheet is solid. Net debt is around $1B, a paltry sum for a company this size. Yet it is not hoarding cash but rather reinvesting it into the company with large R&D ($4.5B) and Capex ($650MM). The company's cash flow situation is solid, as it has had cash flow growth each of the past 3 years, and 2 out of 3 periods had FCF growth of over 20%. FCF yield currently sits around 8.8% It has announced a $10B stock repurchase plan and pays a dividend of almost 1%. There is still plenty of money to reinvest in the business.

The relative valuation looks promising as seen by the chart below:

| P/E | EV/EBITDA | P/FCF | |

| ORCL | 15.34 | 7.98 | 11.31 |

| SAP | 17.14 | 10.81 | 22.54 |

| CRM | NA | NA | 44.40 |

| IBM | 13.99 | 9.25 | 14.61 |

ORCL is also relatively cheap itself historically. Within the past 5 years its P/E ratio has ranged between 13.5 and 24.

I also made a DCF to supplement this and the results are promising. Just for a base case my assumptions were as follows:

For software revenue:

| Starting Margin | 76.22% |

| Margin Growth | 0.40% |

| Revenue Growth | 7.00% |

| Starting Margin | 38.46% |

| Margin Growth | -0.50% |

| Revenue Growth | -1.00% |

| Starting Margin | 22.43% |

| Margin Growth | 0.00% |

| Revenue Growth | 5.00% |

| EBITDA Margin Growth Rate | 0.25% |

| Working Capital Growth Rate | 3.00% |

| D&A Growth Rate | 5.00% |

| Capex (% of revenue) | 12.00% |

| Tax rate | 24.00% |

| Exit Multiple | 7.0X |

| WACC | 10.99% |

| Beginning EBITDA Margin | 44.7% |

In short, Oracle is a strong company well positioned to take advantage of the cloud market. It is not perfect as shown by the success of its competitors. But its size and history provide it with unique advantages. More importantly, ORCL appears to be trading at a discount absolutely and relatively. This makes ORCL a great opportunity to gain exposure to this market.

The results of my DCF can be seen below including a 5-year revenue model.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

By Christopher Bayliss

Source: seekingalpha.com

No comments:

Post a Comment