Buy Nike: The Best Positioned Play On Global Consumer Growth

Executive Summary

Nike Inc. (NKE) has a history of beating the earnings estimates. We recommend a long position on the stock, mainly due to the following reasons:-

- Nike's earnings have grown at a CAGR of 20% since FY09. Moreover, earnings increased by 7% in 3Q2012, as an increase in revenues more than offset the slight decline in gross margins. The company has seen an increase in its profits in each of the last three quarters.

- NKE has consistently shown impressive revenue growth; growing by 15% in the third quarter as compared to 3Q2011. NKE experienced growth worldwide, driven by its brand strength and innovative products. Footwear remains the major contributor to revenue growth.

- Nike's biggest growth opportunity is in emerging markets, especially China, where it boosted a 25% YoY increase in revenues in the third quarter. The growth was driven by increased demand of its footwear.

- Strong Balance Sheet, with a debt to equity ratio of less than 4%.

The Company Description:

NIKE, together with its subsidiaries, engages in the design, development, marketing, and sale of footwear, apparels, equipment, and accessory products for men, women, and children worldwide. The company offers products in the categories of running, training, basketball, soccer, sport-inspired casual shoes, and children's shoes. The company sells its products through retail accounts, its own retail and online stores, independent distributors, and licensees.

Key drivers:

- Rising Consumer Awareness of Good Health: Rising consumer awareness of good health and increased participation in sports, coupled with an increase in the demand for NIKE footwear, have led to increased revenue growth for the company.

- Growth in Emerging Markets: NKE's biggest growth opportunity is in the East. Increasing middle-class populations in countries like China and India have swelled demand for Nike's attainable status symbols, making those countries its most appealing customers.

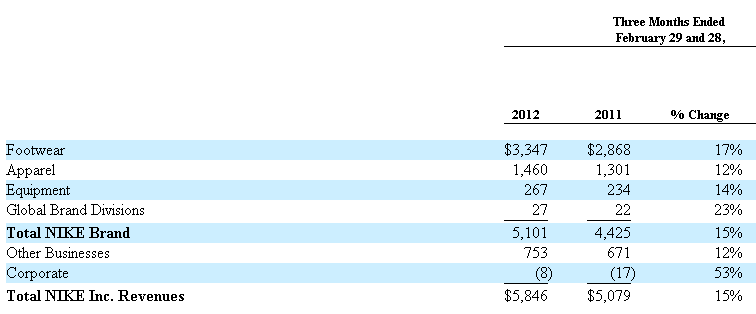

Growth in Revenue and Margins: The company has shown impressive consistent revenue growth, growing by 15% in the third quarter compared to 3Q2011. NKE experienced worldwide growth, driven by NKE's brand strength and innovative products. If we look at the company's annual results, NKE has been consistently posting high gross over the years (averaging 45% since FY09), ranking above Footlocker (FL) and Finish Line (FINL). The table below gives the breakup of NKE'S revenues from different segments, and shows high double-digit growth of 3Q2012.

Footwear was among NKE's major contributors to revenue growth, increasing by almost 20%, largely due to growth in running , sportswear and basketball products. Looking at the geographic-centric data, NKE's North American division provided the major chunk of revenues, with China outperforming all other regions in terms of growth. This growth was possible due to continued expansion in the number of NIKE branded stores, owned by its wholesale customers, and higher comparable store sales.

Earnings Announcement: NKE is to announce its earnings for 4Q2012 on June 28. Revenue is estimated to be at $6.52 billion for the quarter, which shows a 13.1% increase YoY. For the year, revenue is projected to come in at $24.11 billion, showing a growth of 16%, which is significantly higher than last year's 10%. The company has a history of beating the consensus estimates for revenues.

Earnings Analysis: NKE's earnings have grown at a CAGR of 20% since FY09. Moreover, earnings increased by 7% in 3Q2012, as an increase in revenues more than offset the slight decline in gross margins. The company has seen an increase in its profits in each of the last three quarters. It is clear from the table below that the company's diluted earnings per share grew faster than its earnings. This growth was due to a decline in the number of outstanding shares from the company's share repurchase program.

Historically Beaten Earnings Estimates: The company has historically beaten analysts' earnings estimates, and provided healthy earnings surprises (earnings surprise of 12% in 1Q2011). NKE is expected to report earnings of $1.37, an increase of almost 10% from the previous year's $1.24, on June 28, 2012. For the current financial year, analysts agree on an EPS of 4.93%, which if reported, would be an increase of 12% from the previous year.

Stock Performance: Even though the stock lost almost 10% of its value between April and June this year, it has outperformed its peers over a period of one year, as seen in the graph below.

Growth in the Future: Nike's biggest growth opportunity is in emerging markets, especially China, where it boosted a 25% increase in revenues in the third quarter YoY. This increase was largely driven by an increase in demand for its footwear. Moreover, the future orders for NKE's footwear scheduled for delivery from March through July 2012 are 25% higher in China than the orders reported for the comparable prior year period, which also ranks above its demand from North America.

Balance Sheet Analysis: The company has a cash balance of almost $3 billion as of the most recent quarter, and cash flows from operations have largely been consistent year on year. The level of debt is reasonable, with debt-to-equity of 4% and a very healthy looking interest coverage ratio. NKE's current ratio is 3.21, which is considerably higher than the industry average of 0.80.

Valuation: The company's P/E of 16x is trading at a premium to the industry as well as its 5-yr historic average; however, the growth prospects are strong enough to justify a premium valuation.

Recommendation: NKE has performed well in terms of revenue and earnings growth, and has historically beaten the earnings estimates. It has a strong balance sheet and with growth prospects in countries like China, the company is likely to do well going forward. Therefore, we recommend a long position on the stock.

Investors can short sell the Consumer Retail ETF (XLY) to hedge against the long position in NKE.

Competitors:

Foot Locker, Inc.

FL is a retailer of athletic footwear and apparel. The company operates in two segments, Athletic Stores and Direct-to-Customers. The Athletic Stores segment retails athletic footwear, apparels, accessories, and equipment under various formats. The company has shown impressive growth in margins, both on a quarterly and an annual basis. In the recent quarter ended April, 2012, gross margins rose to 34% from 32% YoY. FL reported earnings per share of $0.83 in 1Q2012, 38% higher than the previous year's EPS. The company has a cash balance of almost $900 million, with not a significant amount of debt, currently at around $135 million, and a reasonable debt-to-equity ratio of 6%

Adidas AG (ADDYY)

Adidas AG engages in designing, developing, producing, and marketing a range of athletic and sports lifestyle products worldwide. It offers footwear, apparels, and hardware such as bags and balls, primarily under the Adidas and Reebok brands. The company operates in six segments: Wholesale, Retail, TaylorMade-Adidas Golf, Rockport, Reebok-CCM Hockey, and Other Centrally Managed Brands. The company has total cash of almost $2 billion as of the most recent quarter, and a relatively high debt-to-equity of 30%. Quarterly earnings growth of 38.30% for the company is impressive, however, the stock has underperformed when compared to NKE on a YTD basis.

Key Financials:

NKE

|

ADDYY

|

FL

|

FINL

| |

Market Cap:

|

44.67B

|

14.74B

|

4.33B

|

949.12M

|

Qtrly Rev Growth (yoy)

|

0.15

|

0.17

|

0.09

|

0.19

|

Revenue (TTM)

|

23.42B

|

17.47B

|

5.75B

|

1.37B

|

Gross Margin

|

0.44

|

0.47

|

0.44

|

0.41

|

EBITDA

|

3.46B

|

1.71B

|

605.00M

|

163.53M

|

Operating Margin

|

0.13

|

0.08

|

0.09

|

0.1

|

Net Income

|

2.27B

|

944.12M

|

312.00M

|

84.11M

|

EPS

|

4.79

|

2.25

|

2.03

|

1.59

|

P/E

|

20.33

|

15.65

|

14.08

|

11.49

|

PEG (5 yr expected)

|

1.52

|

2.87

|

0.85

|

0.77

|

P/S

|

1.91

|

0.85

|

0.75

|

0.69

|

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

By Quineqt

No comments:

Post a Comment