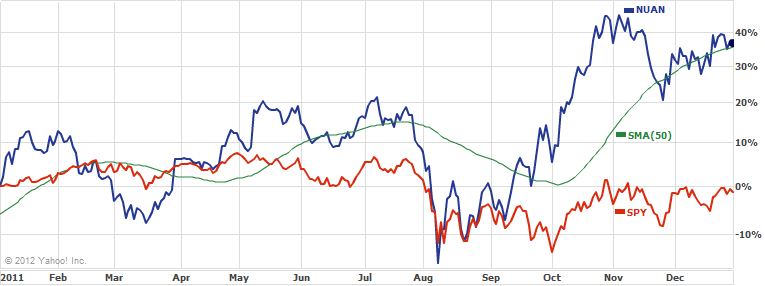

Nuance: The Best Stock To Own For 2012

Nuance (NUAN) is the leading provider of voice and language solutions, with offerings including the Dragon voice recognition line of software and other similar products. Nuance is even rumored to be the company behind Apple's (AAPL) Siri. Neither Apple nor Nuance is saying definitively, but Nuance's official line is that "Apple licenses Nuance's voice technology for use in some of its products." Companies that work with Apple are notoriously required to be furtive about their business dealings, so it is difficult to glean more information.

The popularity of the iPhone 4S and Microsoft's (MSFT) Kinect are shining the spotlight on voice recognition technology; although the core technology is not new, it is finally ready for primetime. Google's (GOOG) Android has similar voice recognition offerings that compare favorably to Apple's offering but do lag behind. The consumerization of technology is spurring the demand for more simple technologies and user interfaces that are more operable for the mainstream.

The three main product lines targeting end-users are individuals, business, and healthcare. Importantly, this is in addition to Nuance providing its underlying solutions to third parties, such as Apple, via licensing agreements. Some facts about Nuance that highlight the depth of its research and development ("R&D"):

Nuance has recorded positive EBIT in the past three years, but only logged net income in 2011.

Ordinarily I do not recommend companies that have losses in two of the last three years, but Nuance is a unique case because it is still essentially a developmental company, and is minimally exhibiting a positive trend. Upon first glance, the balance sheet appears strong, but upon closer inspection the majority of Nuance's assets are intangible. Out of the 4.1B in total assets, 3.1B are intangible (goodwill and intangibles), or 76%. This is slightly alarming, but the current ratio is still 1.8, indicating sufficient liquidity.

Total cash flows from operating activities have been positive and are growing at an approximate 15% rate per year. As a development company, the key focuses are liquidity and solvency, as your objective is to ensure that the company can stay viable while it finances its R&D. Nuance fits this criteria with its current ratio and positive cash flows from ops.

Nuance is not the next Apple. Apple was a once-in-a-lifetime investing opportunity because it was the perfect storm of both external (rise of PCs) and internal (Steve Jobs' brilliance) factors. I dislike when people call a stock "the next Apple," but it is true that few other companies have the dedication to innovation and solutions that Nuance have.

The company is dedicating to developing or acquiring the underlying technology for advanced input methods. This is embodied by Nuance's $102.5M acquisition of Swype, Inc. Initially it appeared strange for a company known for voice input technology to be acquiring a company specializing in tactile input, but CEO Mike McSherry clarified his vision in an interview with TechCrunch:

Nuance also recently acquired Vlingo, a competitor with a similar voice service offering. This is another acquisition that is ideal because it strengthens a competitive advantage. It certainly appears that Nuance's management team "gets it," and has a laser-focused strategy that it is continuing to execute.

How To Play It

While trailing PE is a staggering 220, the forward PE is a more digestible 14 (FYE 2013). I recommending going long NUAN 30 Jan 2013 calls, currently trading at $3.10. If you are less confident you could substitute in the 27 Jan 2013 Calls currently trading at $4.30, which have the largest open interest.

Seeking Alpha contributor Rocco Pendola points out:

Disclosure: Author is long AAPL and GOOG, and may open a long position in NUAN at any time.

The popularity of the iPhone 4S and Microsoft's (MSFT) Kinect are shining the spotlight on voice recognition technology; although the core technology is not new, it is finally ready for primetime. Google's (GOOG) Android has similar voice recognition offerings that compare favorably to Apple's offering but do lag behind. The consumerization of technology is spurring the demand for more simple technologies and user interfaces that are more operable for the mainstream.

The three main product lines targeting end-users are individuals, business, and healthcare. Importantly, this is in addition to Nuance providing its underlying solutions to third parties, such as Apple, via licensing agreements. Some facts about Nuance that highlight the depth of its research and development ("R&D"):

- Nuance holds more than 4,000 patents and patent applications

- A team of more than 200 speech scientists and researchers drive innovation

- Nearly two-thirds of Fortune 100 companies rely on Nuance solutions

- The 8 largest handset and 10 largest auto makers use Nuance solutions

Nuance has recorded positive EBIT in the past three years, but only logged net income in 2011.

Ordinarily I do not recommend companies that have losses in two of the last three years, but Nuance is a unique case because it is still essentially a developmental company, and is minimally exhibiting a positive trend. Upon first glance, the balance sheet appears strong, but upon closer inspection the majority of Nuance's assets are intangible. Out of the 4.1B in total assets, 3.1B are intangible (goodwill and intangibles), or 76%. This is slightly alarming, but the current ratio is still 1.8, indicating sufficient liquidity.

Total cash flows from operating activities have been positive and are growing at an approximate 15% rate per year. As a development company, the key focuses are liquidity and solvency, as your objective is to ensure that the company can stay viable while it finances its R&D. Nuance fits this criteria with its current ratio and positive cash flows from ops.

Nuance is not the next Apple. Apple was a once-in-a-lifetime investing opportunity because it was the perfect storm of both external (rise of PCs) and internal (Steve Jobs' brilliance) factors. I dislike when people call a stock "the next Apple," but it is true that few other companies have the dedication to innovation and solutions that Nuance have.

The company is dedicating to developing or acquiring the underlying technology for advanced input methods. This is embodied by Nuance's $102.5M acquisition of Swype, Inc. Initially it appeared strange for a company known for voice input technology to be acquiring a company specializing in tactile input, but CEO Mike McSherry clarified his vision in an interview with TechCrunch:

The broadest vision is we want to be the input for every single stream. You talk to your refrigerator and in-car navigation, you want your language models to follow you around.It is now apparent that Nuance's vision is not simply voice technology. Nuance's well defined vision is to be the leading communication company, a space that is becoming more and more valuable.

Nuance also recently acquired Vlingo, a competitor with a similar voice service offering. This is another acquisition that is ideal because it strengthens a competitive advantage. It certainly appears that Nuance's management team "gets it," and has a laser-focused strategy that it is continuing to execute.

How To Play It

While trailing PE is a staggering 220, the forward PE is a more digestible 14 (FYE 2013). I recommending going long NUAN 30 Jan 2013 calls, currently trading at $3.10. If you are less confident you could substitute in the 27 Jan 2013 Calls currently trading at $4.30, which have the largest open interest.

Seeking Alpha contributor Rocco Pendola points out:

Increasingly, you simply cannot use traditional quantitative data points to come to a valuation/price for a stock. Or you, at the very least, cannot calculate one that serves investors well or has any meaning in the real world.The most important question to ask when investing is "why." Why is the PE so high? Why is the forward PE so low? The answer is that investors are very optimistic about the company's future prospects. If you agree with the premises presented above and believe in Nuance's future prospects, then you do not have to fear the high PE. A high PE is only one of many potential warning signs, and does not automatically indicate a short candidate.

Disclosure: Author is long AAPL and GOOG, and may open a long position in NUAN at any time.

January 11, 2012

No comments:

Post a Comment