Many stocks (especially small caps) have been hit hard in the past few months by tax-loss selling and the subsequent market correction.

Even though the market has begun to rebound from recent lows, there are many undervalued stocks that are worth buying now.

Natuzzi has drifted lower in the past couple of months, and it was already very cheap to start with.

There are a number of big and very favorable macro trends that appear to be positioning Natuzzi for profits and a turnaround.

Natuzzi shares trade for just about $1.50, and appear to have significant upside when considering a $6.26 analyst price target, and industry valuations.

Shares of Natuzzi (NYSE:NTZ) have dropped from about $1.85 in early 2016, to just around $1.50 in recent days. That is a decline of roughly 20% which appears excessive especially since there has been no news from the company during this time frame and also because this stock was already a bargain when it was closer to $2. The stock market has begun to rebound and the fears that were hitting the market such as a plunge in oil and worries about China, etc., have been fading. Small cap stocks were hit the hardest in the recent correction and therefore could have more upside potential. Based on this, I have been taking a fresh look at some of my favorite small cap stocks from the past as well as some new ones that could offer rebound potential in the short-term, and even more significant upside in the long-term. With this in mind, let's take a closer look at Natuzzi which is a leading designer and manufacturer of home furnishings:

Natuzzi designs and manufactures the items shown above.

Photo credit: Natuzzi.com Website

As the chart above shows, Natuzzi shares spiked up to about $2.40 in September, but have since drifted down to around $1.50, even though there was no news or fundamental reason for this decline. The main reason was tax-loss selling at the end of last year, followed by a market correction in early 2016, that was accompanied by extremely negative investor sentiment. That negativity is starting to fade and investors are once again looking for opportunities. The chart shows a light blue uptrend line as well as a purple downtrend line, both of which are now forming a wedge, which I believe will be resolved with this stock breaking out and rebounding back towards the 200-day moving average of $1.85 per share.

Natuzzi was once priced at much higher levels. It was trading for over $9 per share just before the 2008 Financial Crisis and in 1998, it even traded for about $29 per share. Obviously, Natuzzi was hit hard during the Financial Crisis that started in 2008, as well as by the ensuing recession in the Euro zone. However, the economy in Europe is beginning to heal and the sales trends and profit margins at Natuzzi are confirming that a significant turnaround is finally underway. Natuzzi announced financial results for the third quarter of 2015, which showed continued progress in both sales growth and profit margin expansion. The third quarter of 2015 is now the fifth straight quarter in a row to show significant sales gains and it just reported positive EBITDA (1.5 million Euros). Please also note the reduction in the cost of goods sold or "COGS" which shows this company is growing profit margins. All of this can be viewed in the table provided by Natuzzi below:

The continuous improvement of the key indicators over the last six quarters is highlighted below:

| 1Q 2014 | 2Q 2014 | 3Q 2014 | 4Q 2014 | 1Q 2015 | 2Q 2015 | 3Q2015 | ||||||||

| Total Net Sales* | -11.2% | -1.2% | +8.2% | +12.6% | +24.6% | +5,7% | +3.1% | |||||||

| COGS** | -71.5% | -74.2% | -72.1% | -71.2% | -70.6% | -69.0% | -67.3% | |||||||

| Other SG&A** | -21.8% | -20.9% | -18.2% | -17.7% | -17.3% | -18% | -17.3% | |||||||

| EBITDA** | -6.0% | -7.1% | -3.3% | -3.7% | -1.2% | -0.8% |

+1.3%

|

* change in quarterly sales on corresponding quarters of the previous years

** percentage of net sales

If you consider that Natuzzi was trading for about $9 per share in 2007, and then the company was hit by the Financial Crisis (globally) as well as by the ensuing plunge in housing prices in the United States, it is easy to see why this stock went down and why the company had big challenges with revenues and profitability. The response to the crisis from the United States was to lower interest rates to nearly zero, but this caused another problem for many European exporters like Natuzzi. Extremely low interest rates and loose money policies in the U.S. led to a significant amount of weakness in the U.S. Dollar. Meanwhile, the Euro zone kept a much tougher stance and decided for a tougher position on interest rates and called for countries to implement austerity, rather than massive stimulus that the U.S. employed. This caused the Euro currency to soar and that made everything from Europe much more expensive. I remember being in Europe a few years ago when I had to pay $1.50 just to buy a Euro, but now it is around $1.10 to buy a Euro. That means the huge headwind from currency exchange for European exporters has improved dramatically.

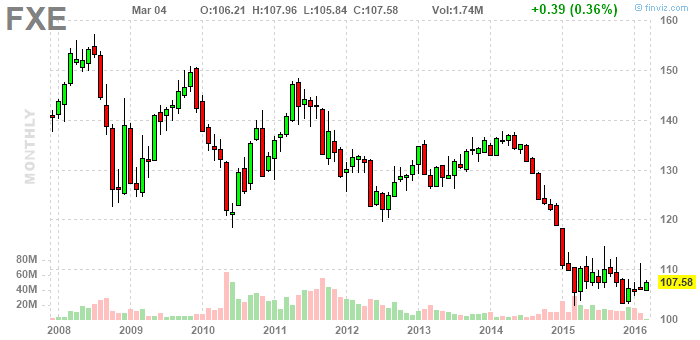

As you can see from the chart of the CurrencyShares Euro ETF (NYSEARCA:FXE) above, the Euro was still quite strong up until the end of 2014, and then it started to plunge, and now remains near the lows. Since this has only been a fairly recent development that has been around for just the past few quarters or so, the full impact has probably not yet been reached, especially since there is a potential lag due to any currency hedges. This kind of drop of roughly 40%, is a massive benefit for a company like Natuzzi and it is one of the reasons why the macro trends are now very positive for this company. But there are other macro trends that are hugely beneficial for Natuzzi that investors should consider now:

Aside from the major tailwind this company is getting from the weakening Euro, it is also benefiting from macro trends such as the continued strength in the U.S. for housing and furniture sales, and also from rising job growth. It is also likely to see even better financial results now that the economy in Europe has stabilized and even started to show some growth. In the past few weeks I have seen a number of data points and other signs that suggest the recent positive sales gains and profit margin improvement trends are likely accelerating for Natuzzi:

First of all, home furnishings have been on the rise in the U.S., due to a rebound in the housing market and also because of job growth. A number of furniture companies have been reporting solid revenue growth. For example, Berkshire Hathaway's (NYSE:BRK.A) (NYSE:BRK.B) furniture division recently reported a 24% jump in revenues. LaZBoy recently reported a 7% revenue increase. American Furniture recently reported a 37% increase in revenues. Furthermore, according to a Furniture Today article, this industry looks poised for solid growth as furniture sales are expected to rise nearly 4% this year and 19.6% by 2020. A February 29, 2016, article in Barron's discusses that the "home furnishings sector is seeing a resurgence", and mentioned that Ethan Allen (NYSE:ETH) recently announced better than expected earnings. This is another sign of a big macro trend that is likely to benefit Natuzzi, especially since the U.S. is one of its biggest sources of revenues.

All of these signs of a resurgence in home furnishings are great macro trends for Natuzzi, but it is even more significant when there are indications coming directly from this company that would appear to indicate it is also seeing growth and expansion potential in the U.S. On September 16th, 2015 it wasannounced that Natuzzi was opening a 9,000 square foot store in Palm Beach at CityPlace right next to a Restoration Hardware (NYSE:RH) furniture "mansion" store. The Natuzzi store is expected to open in the Spring of 2016. On February 1, 2016, Natuzzi opened its first store in Pennsylvania on South Street, which would also seem to indicate that the company is seeing strong results in the U.S. and potential for more growth.

Natuzzi Italia Storefront in Pennsylvania

Photo credit: Furniture Today

Europe is also a major market for Natuzzi and there are reasons for increased optimism in that region as well. In 2015, the European Central Bank or "ECB" started to reverse course and take actions that are similar to what the U.S. Federal Reserve did a few years ago, in order to boost the economy. It takes time for quantitative easing to trickle through the economy, but there are already some signs of improvement. It appears that the ECB wants to accelerate growth even more and it is expected to take additional action to stimulate growth and inflation when it meets on March 10, 2016. Low interest rates have started to create a rebound in Europe's housing market, particularly in Spain which was hit hard during the Financial Crisis. Just as we saw in the U.S., stimulus from the Federal Reserve and low interest rates led to a rebound in housing and jobs which led to a big rebound in home furnishings. With Europe now mimicking these actions, and with the Euro currency exchange rates far more favorable, these are big macro trends that will hugely benefit Natuzzi. The efforts by the ECB seem to be gaining some traction because retail sales numbers in the Euro Zone rose more than expected in January. Aside from the actions by the ECB, the big drop in oil prices is also likely to boost consumer spending in Europe. I am not the only one who thinks Natuzzi is going to benefit for the next few years from ECB policies, a Benzinga article states:

"Furniture maker Natuzzi, is an unlikely candidate for stock pickers, as the firm is priced at under $2 per share. However, many analysts believe that smaller firms will reap the largest benefits from further EU stimulus, and the company's low share price makes it a buying opportunity.Natuzzi recently opened a new store in Naples, Florida, and is set to continue expanding across the United States and Asia. That means that the company will benefit from growth in both economies, even if the eurozone continues to weaken."

Natuzzi has been reporting financial results that clearly show major improvement. Many of the conditions that were in place in 2007, when this stock was trading for $9 are coming back now-that includes the weaker euro, increased consumer spending and a stronger housing market. With these very big and very positive macro trends going in its favor now, I think it is just a matter of time before Natuzzi reports it is profitable again. Once that happens, I believe this stock will appreciate significantly from the extremely low and undervalued levels it trades at now. A return to profitability could lead to increased analyst coverage, which may help broaden the very limited exposure this company has with U.S. investors. Right now, I can only find one analyst who covers Natuzzi and they have set a price target of $6.26 per share, which suggests very significant upside potential.

Based on the current level, a price target of $6.26 per share would represent a gain of about 350%. That might seem overly optimistic, but when you consider the fundamentals it appears realistic. For example, the book value is about $3.50 per share. This company has a market cap of just under $100 million and annual revenues of about $550 million, which is equivalent to $9.34, on a per share basis. That means the price to sales ratio is extremely low and this is often a major sign a stock could be undervalued. Hooker Furniture (NASDAQ:HOFT) trades for about $32 per share, its revenues are equivalent to about $23 per share, and the book value is about $14 per share. This shows it is trading for around 1.5 times book value and for about 1.5 times revenues, which is in the range of other publicly traded furniture companies. If Natuzzi were to be valued at 1.5 times revenues, it would be trading for about $14 per share. If it were valued at 1.5 times book value, it would be trading at $5.25 per share.

I believe potential downside risks are limited at these levels for a number of reasons. Natuzzi has a very strong balance sheet with nearly $45 million in cash and just around $35.7 million in debt. That is a very small amount of debt for a furniture company with well over half a billion dollars in annual sales. This also shows that Natuzzi is net debt positive, since it has more cash than debt. This company has been seeing revenues grow and losses narrow for the past few quarters. These improving financial results appear to be a trend that is likely to continue, all of which reduces the potential downside. Mr. Pasquale Natuzzi (the founder and CEO) owns nearly 31 million shares or about 56% of the entire company. This major ownership stake could also limit downside risks as it suggests that Mr. Natuzzi's interests are directly aligned with other shareholders and that he is probably highly motivated and working hard to get Natuzzi shares at much higher levels.

Based on the recent revenue growth, and a few big macro trends, I believe Natuzzi is poised to report a profit in the next quarter or two. However, the exact timing does not matter, the point is that many indicators and trends appear to indicate is just a matter of time before profits return. It could payoff big to be in this stock before that happens, as well as to hold these shares for the next couple of years as the Euro zone economy improves. The U.S. economy has steadily improved since the Federal Reserve started quantitative easing and Europe only started last year, so there could be years of solid improvements in the European economy as well.

In summary, Natuzzi shares are dirt cheap when you consider book value, the price to sales ratio, and industry valuations. This company is seeing very positive growth trends in revenues and in profit margins. Natuzzi came very close to reporting a profit last quarter and it did actually report positive EBITDA. Further bolstering the case for the investment opportunity and upside potential in this stock is the fact that big macro trends are extremely positive; this includes: a much weaker Euro currency, strong furniture sales and store expansion in the U.S, plus continued aggressive action by the ECB to improve the economy in Europe. In 2015, Natuzzi reported fourth quarter and full-year results on March 27th. Based on this, I expect Natuzzi to make an announcement about this soon and report fourth quarter and full-year results for 2015, on or around March 27, 2016. Based on all of the positive macro trends and the momentum in revenue growth Natuzzi has been generating, I expect more good news. My short term price target on this stock is $1.85 which is right around the 200-day moving average. However, I think the upside is far more significant in the long run and I see no reason why this stock can't trade back at around $6 per share, which is close to the price target set by one analyst. For my future updates on Natuzzi and other deep value stocks, please consider following me.

Data is sourced from Yahoo Finance. No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Disclosure: I am/we are long NTZ.

By Hawkinvest

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

No comments:

Post a Comment