Includes: AAV, AR, BXE, CLR, COG, CVX, EQT, FANG, GENGF, OAS,

Summary

I attempt to evaluate some of the ways an investor could play the potential rebound in oil and natural gas prices.

Sifting through the carnage requires hard work, but it could provide some of the most lucrative opportunities.

Buying the best risk/reward E&P companies that will survive is the key.

The oil price is in the dumps. It has declined 77% from the top in June 2014.

There isn't a single E&P company in North America that's making money if you include full cycle finding and development cost. So the question is, how can you make money from this selloff?

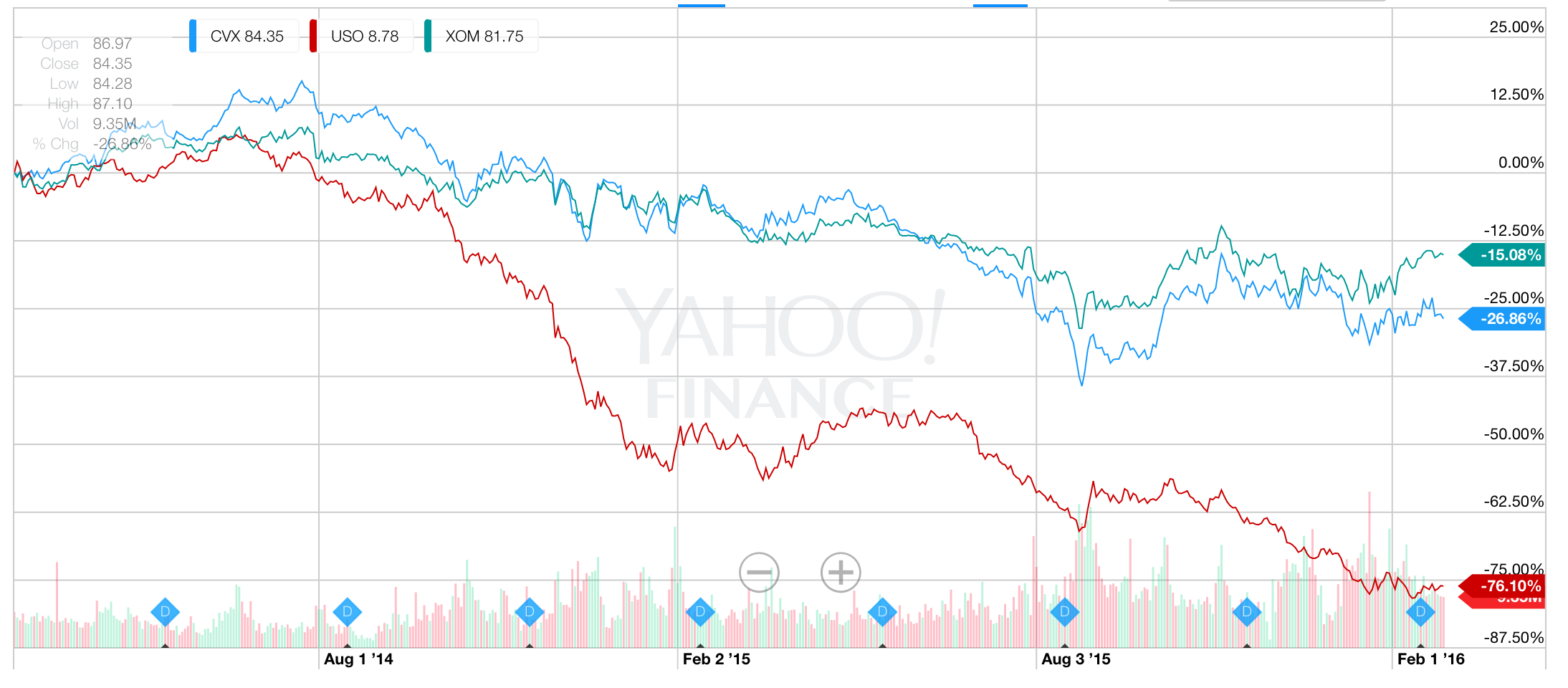

Option 1: Buying USO or OIL. The worst way to do it

If you considered buying an ETF like the the iPath S&P GSCI Crude Oil Total Return Index ETN (NYSEARCA:OIL) or the United States Oil ETF (NYSEARCA:USO), then I can say that that is the worst way to play the rebound. As many of you may know, WTI currently trades in contango, which means forward prices are much higher than current prices. This creates a negative carry which means that the longer it takes for prices to rebound, the higher the potential for permanent impairment of capital.

Option 2: Buying oil majors like Chevron and Exxon

This is the option many people have been choosing as it's probably the safest way to play the rebound. What's not talked about is how insulated the majors have been relative to the magnitude of the oil selloff.

Both Exxon (NYSE:XOM) and Chevron (NYSE:CVX) are pricing in a recovery of oil to the $55-$60 level, so if you expect WTI to rebound to that level, the likelihood of appreciable gains for the risks taken aren't very appealing.

The risk/reward isn't skewed to the investor's favorite.

Option 3: Buying Russia or countries correlated to the price of oil

One very attractive alternative is to buy non-oil related companies in countries that are tied to the price of oil. Russia (NYSEARCA:RSX) is a great example where price appreciation for the whole index would rise if the price of oil recovers as the Ruble would strengthen relative to the Dollar.

What's also intriguing about this play is it offers a sort of idiosyncratic risk as the potential of the sanctions being lifted could play a positive catalyst for both Russian equities and the Ruble.

Option 4: Buying the best risk/reward E&P companies that will survive the downturn (Most attractive)

Option 4, in my opinion, is the most attractive option as it offers investors the highest risk/reward. There are a lot of companies that can survive the downturn within a reasonable time estimate (3-5 years), and some that won't have any risk of insolvency.

I have highlighted a few investments that I thought were particularly attractive and written them up here.

Peyto (OTCPK:PEYUF), Advantage (NYSE:AAV), Bellatrix (NYSE:BXE), Painted Pony (OTCPK:PDPYF), Gear Energy (OTC:GENGF).

Notice how many of these are mostly Canadian natural gas producers? What I find is that during the commodity selloff, natural gas producers sold off along with oil producers thanks to record warm winter and storage levels that also caused natural gas prices to tank to historical lows.

The selloff in natural gas combined with oil depressed many of the E&Ps in my list, and I've set out to look for the most appealing ones out of the bunch.

Some of the U.S. names I particularly like include Cabot Oil (NYSE:COG), Antero (NYSE:AR), EQT (NYSE:EQT), and Range Resources (NYSE:RRC), which are all mostly natural gas as well.

On the oil side, I have found very few superior operators, and when I did, their share prices have detached from the selloff in oil as market participants went into these companies as safety nets. Raging River (OTC:RRENF) and Diamondback Energy (NASDAQ:FANG) are good examples of a high quality oil companies.

Some of the more distressed opportunities I have found to be appealing include Continental Resources (NYSE:CLR) and Oasis Petroleum (NYSE:OAS).

Concluding Thoughts

The best way to play the rebound in oil and natural gas prices is to find the companies with just bad enough balance sheets where the market rips them apart (falling share prices), but well capitalized and low cost enough to be able to live through the downturn.

For information or help with regards to E&P investing, please consider subscribing to Hedge Fund Insights Premium Research as we set out to help investors navigate through the carnage and to avoid some of the common pitfalls made by investors. We have also written how-to articles to help investors look at E&P companies. We hope you can join the community!

Disclosure: I am/we are long BXE, AAV, PEYUF, PDPYF, COG, AR, RRC, GENGF, EQT.

By Hedge Fund Insights

No comments:

Post a Comment